Spain’s 83.7-year life expectancy in 2023 is more than a lifestyle statistic. It is an investment signal. Long-lived populations, strong healthcare access, and sustained international appeal tend to support steady housing demand, especially in retirement-led and expat-led markets. For UK buyers thinking about living in Spain rather than just owning a holiday flat, that distinction matters.

The market is also more segmented than many guides suggest. Madrid, Barcelona, Costa del Sol, and Valencia serve different investor profiles, while the Balearics and Canaries sit in a separate category altogether, driven more by scarcity, tourism patterns, and second-home demand. The right choice depends less on headline appeal and more on your intended use, tax position, tenancy model, and post-Brexit residency plan.

The Investment Case for Living in Spain in 2026

Spain remains one of the few European markets where lifestyle strength and property logic overlap cleanly. The country’s appeal isn’t just climate. It rests on health outcomes, affordability, and a broad tenant base that includes retirees, mobile professionals, lifestyle migrants, and domestic urban renters.

According to Our World in Data’s Spain demographic profile, Spain’s life expectancy reached 83.7 years in 2023, compared with 81.3 years in the UK. The same verified dataset notes that Spain has also been ranked the world’s top destination for expat quality of life for four consecutive years. For property investors, that combination points to durable end-user demand rather than purely speculative demand.

Why living demand matters more than holiday demand

A market built only on tourism can produce good income in strong seasons and weak resilience when conditions change. Spain is different because a meaningful share of demand comes from people who want to live in Spain full-time or for extended parts of the year.

That affects holding quality in three ways:

- Retiree demand supports longer stays. Older international residents tend to value healthcare access, climate, and daily convenience over short-term price speculation.

- Expat demand broadens the rental pool. Demand isn’t limited to summer visitors. It also includes tenants seeking medium and long stays.

- Lifestyle-led purchases can stabilise resale demand. Buyers often enter the market for personal use first, then convert to investment use later.

Practical rule: In Spain, the strongest long-term locations are usually the ones people choose for ordinary life, not just for a week in August.

Spain’s appeal is strongest when compared, not viewed in isolation

The clearest way to assess living in Spain is against competing European choices. Spain combines high perceived quality of life with a lower everyday cost base than many alternative destinations. That helps explain why it remains central in relocation planning for UK households seeking both usable property and portfolio diversification.

For investors comparing destinations, this guide to the best EU countries to live in is useful because it frames Spain within a wider relocation and investment context rather than treating it as a one-size-fits-all answer.

The real thesis for 2026

The core case for Spain is straightforward. It is not the cheapest market, not the fastest-moving market, and not the least regulated market. It is, however, one of the most investable markets for buyers who want a property to serve both income and life use.

That makes Spain particularly relevant for UK investors who want one asset to do multiple jobs. Residence option. Family base. Pension-stage home. Rental property. Currency diversification. Very few markets perform credibly across all five.

Navigating Spanish Residency and Tax for UK Investors

Post-Brexit, living in Spain requires more planning for UK nationals, but the main routes are clear. For most investors, the practical choice is between a Golden Visa strategy linked to property purchase and a Non-Lucrative Visa for passive-income households.

The decision is less about paperwork than about intent. If you want mobility, work rights, and a property-led route, the Golden Visa is the more direct investment structure. If you’re relocating on pensions, dividends, or other passive resources without local employment, the Non-Lucrative Visa often fits better.

Golden Visa for property-led residency

According to NIM Extranjeria’s guide to Spanish residency, UK investors seeking residency through the Golden Visa must invest €500,000 in unencumbered real estate. The same source states that this route grants immediate residency with Schengen mobility and work rights, while Spain’s double-tax treaty helps avoid dual Capital Gains Tax exposure, and the Beckham Law can cap Spanish income tax at a flat 24% for six years.

For many UK buyers, the main advantage is strategic rather than cosmetic. Property becomes both an asset and an immigration tool. That can be compelling if your purchase budget already sits at or above the qualifying threshold.

A useful companion reading for tax planning is this Beckham Law advisory by renn, particularly for investors trying to understand when the regime is beneficial and when ordinary Spanish tax treatment may be more appropriate.

Non-Lucrative Visa for passive-income households

The Non-Lucrative Visa is often better suited to retirees and financially independent households. According to this Spain residency overview, the minimum financial requirement for 2026 is €28,800 annually for a single applicant, plus €7,200 per additional family member, with proof typically shown through bank statements and tax returns.

That route does not depend on a property purchase. It depends on demonstrating that you can support yourself without local employment. In practice, that makes it attractive for buyers who want to acquire property gradually, rent first, or preserve flexibility before committing larger capital.

Choosing between the two

A simple decision framework helps.

| Investor profile | More likely fit | Why |

|---|---|---|

| High-net-worth buyer already planning a substantial purchase | Golden Visa | Property spend and residency objective align |

| Retiree with pension or investment income | Non-Lucrative Visa | Passive income route may be simpler |

| Buyer wanting work rights in Spain | Golden Visa | Work rights are part of the route cited above |

| Household testing life in Spain before larger acquisition | Non-Lucrative Visa | Reduces pressure to buy immediately |

Residency should follow the asset strategy, not the other way round.

Tax isn’t national in the way many UK buyers expect

Spain’s tax environment requires regional awareness. The verified data shows that Madrid offers a 100% wealth tax exemption on assets over €700,000, versus 0.2% to 3.5% elsewhere, which can materially change the holding appeal for higher-value investors when choosing where to base themselves within Spain.

That means two buyers with similar budgets can end up with very different after-tax outcomes depending on region, income type, and residency status. It also means the “best” area to buy isn’t always the same as the best area to become tax resident.

Use this practical guide on how to emigrate from the UK as a planning checklist. It helps organise the relocation sequence properly, which matters because visa timing, tax residency, healthcare access, and property completion often interact.

The main mistake UK investors make

Many buyers look at residency as an administrative add-on. It isn’t. It affects acquisition structure, financing conversations, tax exposure, and even which region makes sense as a base.

If you’re planning on living in Spain, your property search should start with four questions:

- Will the property be part of the residency route, or separate from it?

- Will you become tax resident in Spain?

- Do you need work rights, or only residence rights?

- Is your preferred region still optimal once tax treatment is considered?

Those questions are more important than whether the flat has sea views.

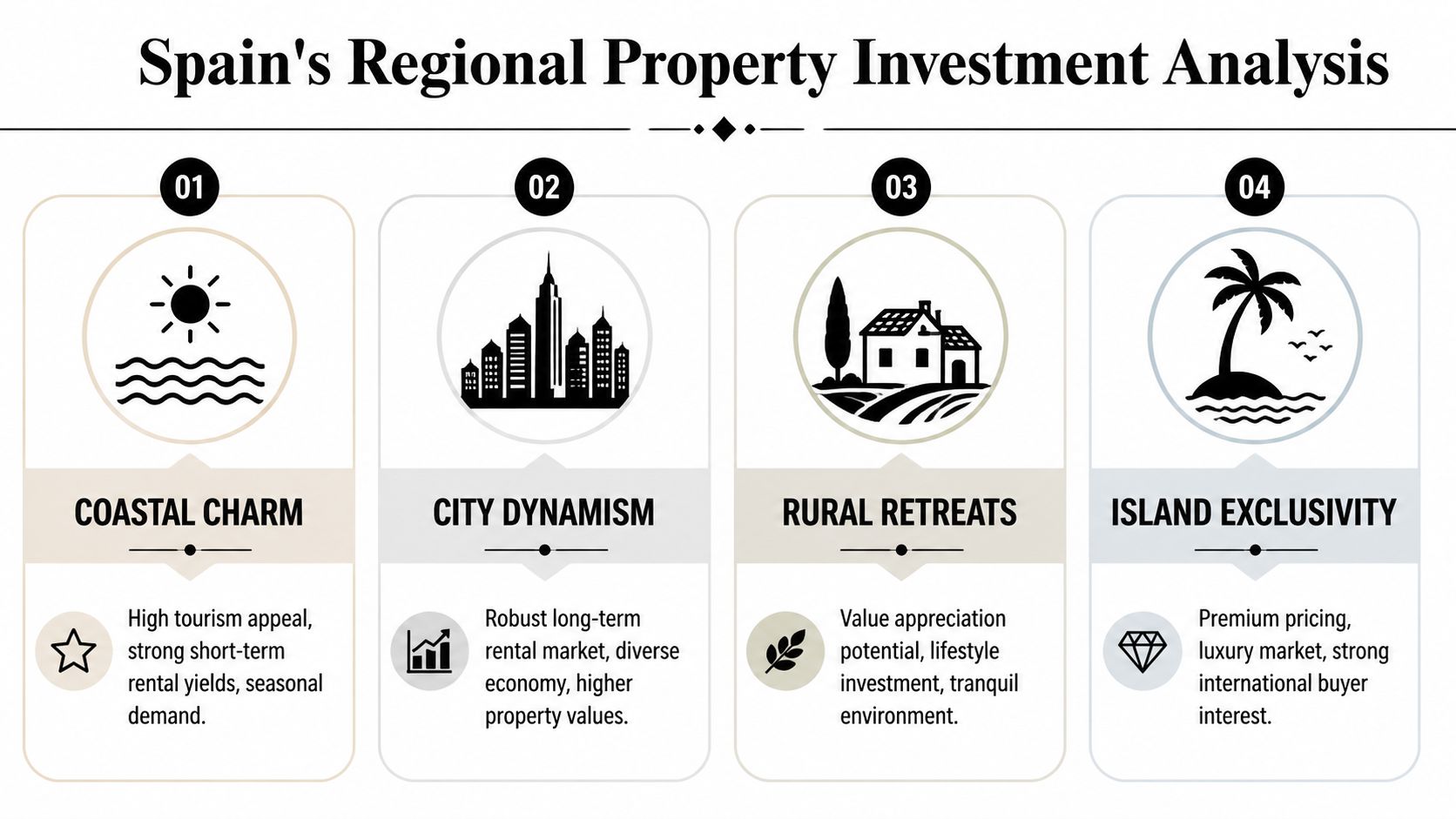

Spain's Property Market A Regional Investment Analysis

In Spain, regional selection does more to shape long-term returns than almost any other buying decision. A flat in Madrid, a villa on the Costa del Sol, and an apartment in Tenerife may sit under the same national legal system, but they behave like different assets, with different tenant demand, different exit routes, and different sensitivity to regulation and tourism cycles.

For UK investors, the most practical framework is to separate Spain into two groups. The first is the Big Four. Madrid, Barcelona, Costa del Sol, and Valencia. These markets offer the clearest comparables, the deepest buyer pools, and the strongest visibility on resale. The second is the island group. Balearics and Canaries. Those markets are narrower, more supply-constrained, and more dependent on international leisure demand. The right choice depends less on lifestyle preference than on three variables. Risk tolerance, yield target, and whether the purchase supports a wider post-Brexit residency plan.

Madrid and Barcelona for depth and liquidity

Madrid and Barcelona sit closest to core urban exposure. They suit investors who care more about liquidity, year-round tenant depth, and institutional-style resilience than holiday appeal.

Madrid stands out for scale and economic centrality. It has a broad occupier base, less reliance on seasonal flows, and a stronger fit for buyers building a long-term rental strategy around professionals, corporate tenants, and domestic demand. For investors who may want to refinance or exit into a larger resale pool, those characteristics matter.

Barcelona offers a different proposition. It has stronger international branding and sharper lifestyle appeal, but that usually comes with less margin for pricing mistakes. In practical terms, investors should be more selective on micro-location, building quality, and unit layout because a premium city punishes weak stock more quickly during slower market phases.

Which investor fits each city

- Madrid suits buyers seeking stable urban demand, broader tenant diversification, and a lower dependence on tourism.

- Barcelona suits buyers prepared to accept higher entry pricing in return for international visibility and stronger end-user appeal.

The best urban assets in Spain are usually the properties that can serve several exit routes at once. Long-term rental, refinance potential, and owner-occupier resale.

Costa del Sol for mixed-use ownership and tourism income

Costa del Sol should be treated as an international leisure market with residential depth, rather than as a standard regional market. Demand comes from retirees, second-home owners, seasonal tenants, and international buyers who may use the property themselves before shifting to partial rental use.

That mix creates flexibility. It also creates operational risk. Returns depend more heavily on management quality, local rental rules, and the ability to hold occupancy outside peak periods. Buyers who treat the area as passive income often underestimate how much performance depends on the exact asset and the exact sub-market.

Costa del Sol tends to fit three investor profiles:

- buyers who want personal use for part of the year,

- investors targeting seasonal or holiday-led income,

- and residency-focused purchasers who want a familiar international market with strong resale visibility.

For UK buyers comparing the Big Four, Costa del Sol usually sits between city stability and island specialisation. It offers stronger lifestyle utility than Madrid and Barcelona, but less pricing discipline than a pure urban market.

Valencia for better entry pricing and balanced demand

Valencia is the most interesting mainland market for investors who want a lower cost base without moving into a thin or speculative market. It offers a stronger balance between affordability, liveability, and tenant depth than many higher-profile Spanish locations.

That matters because lower entry pricing changes the return equation in several ways. It can improve gross yield potential, reduce financing pressure, and widen the margin for error if interest costs remain high. It also gives owner-investors a more credible route to combining personal use with long-term holding discipline.

Valencia benefits from demand that is broader than tourism alone. The market can attract local professionals, international residents, lifestyle migrants, and tenants who choose the city for everyday living rather than short stays. For UK investors who want to live in Spain while preserving sensible investment maths, that is a strong combination.

Valencia versus Barcelona

| Factor | Valencia | Barcelona |

|---|---|---|

| Entry pricing | Lower | Higher |

| Demand profile | Balanced local and international use | More globally branded, higher-end demand |

| Investor fit | Yield-conscious, long-term hold | Premium city exposure, lower tolerance for poor asset selection |

A useful discipline here is to run the same property through multiple scenarios before buying. Personal use, long-term tenancy, and resale. This property ROI calculation guide is a practical way to compare those outcomes consistently across regions.

Balearics and Canaries for specialist island exposure

The islands sit outside the standard mainland framework. They are not entry-level markets for most overseas buyers, and they should not be assessed using the same assumptions as Madrid, Valencia, or even Costa del Sol.

The Balearics appeal primarily through scarcity, prestige, and second-home demand. That can support values for prime stock, particularly where planning constraints and limited supply restrict future competition. The trade-off is a narrower occupier pool and a purchase case that often depends more on wealth preservation than on straightforward rental yield.

The Canaries are different. Their investment case is more income-led, with year-round tourism appeal and a seasonal profile that differs from many mainland coastal markets. For investors comfortable with tourism exposure, that can be attractive. For investors seeking predictable, city-style tenancy patterns, it is a weaker fit.

In portfolio terms, island property usually makes more sense for buyers who already understand Spain, or who are making a deliberate choice to accept higher volatility in exchange for stronger lifestyle use, scarcity value, or tourism-led upside.

Established markets versus specialist markets

The central comparison is not city versus coast. It is depth versus concentration.

The Big Four usually offer:

- broader resale demand,

- easier price benchmarking,

- more financing visibility,

- and tenant bases that are less dependent on one demand source.

The island markets can offer:

- stronger scarcity,

- more emotional buyer demand,

- and better performance for exceptional stock.

But they also require tighter underwriting. A buyer can recover from an average purchase more easily in Madrid than in a specialist island sub-market with a smaller pool of future buyers.

A note on inland bargains

Low headline prices in inland Spain can look attractive to first-time overseas buyers. In many cases, they reflect weak local demand rather than hidden value.

For investment purposes, cheap property is only useful if there is durable occupier demand behind it. Areas with shrinking populations, limited employment, and thin resale markets may work as personal lifestyle purchases, but they are rarely dependable income assets. UK investors focused on long-term returns should be careful not to confuse low entry cost with low risk.

A practical market framework for UK investors

The regional map is clearer when framed by objective rather than by marketing appeal:

- Madrid for liquidity, urban depth, and lower dependence on seasonal demand.

- Barcelona for prime-city exposure and international resale appeal, with less room for pricing mistakes.

- Costa del Sol for personal use, tourism-linked income, and residency-aligned buying.

- Valencia for lower entry pricing, broader day-to-day liveability, and stronger yield logic.

- Balearics for scarcity, prestige, and long-hold wealth preservation.

- Canaries for specialist, tourism-facing income with a different risk profile.

For most UK buyers, the decision is not about finding the single best place to live in Spain. It is about matching the region to the return model. The Big Four usually suit investors who want clarity, scale, and easier exits. The islands suit investors who are willing to accept narrower demand in exchange for scarcity or higher-yield tourism exposure.

The Financials Understanding Costs Yields and ROI

A small difference in annual yield matters less than a large difference in costs, vacancy risk, and exit liquidity. That is why UK investors comparing Spain’s Big Four with the Balearics and Canaries should treat headline rent as only one part of the return equation.

Spain works best as an investment market when the property, the tenant base, and the ownership structure fit the same objective. A Madrid apartment aimed at long-term professionals should be underwritten differently from a Costa del Sol unit relying on seasonal bookings. The same applies to the islands. Scarcity can support pricing in the Balearics, but that does not automatically produce stronger cash flow. The Canaries can offer higher income potential in tourism-led stock, but with a narrower operating margin for mistakes.

Cost of living matters because it affects occupier demand

As noted earlier, Spain’s lower living costs are part of the investment case. They help support demand from local households, international workers, retirees, and post-Brexit lifestyle movers who want a predictable monthly budget. For investors, that matters most in markets where rental demand is linked to year-round employment and day-to-day liveability rather than peak-season tourism.

This is one reason Valencia often stands out on a risk-adjusted basis. It tends to offer a more manageable entry point than the prime districts of Madrid or Barcelona, while still benefiting from a real local economy and broad occupier demand. By contrast, parts of the Balearics can preserve capital well because supply is constrained, but the income case is often weaker once purchase costs, management, and seasonality are included.

Gross yield is only a screening tool

Quoted yields are useful for filtering markets. They are not enough to price risk.

A reliable appraisal separates gross yield from net yield and then tests whether the income stream is durable. Investors who skip that step often overpay for tourist-facing property and understate how much return depends on occupancy, licence position, and ongoing management.

Use a simple sequence:

- Start with annual rent based on realistic occupancy

- Divide by total capital committed, not just the agreed purchase price

- Deduct recurring ownership and operating costs

- Test the numbers against weaker occupancy, higher financing costs, and slower resale conditions

This guide on how to calculate return on investment property is a useful framework because it focuses on return after costs, not the headline figure used in sales material.

High gross yield can still produce mediocre returns if the asset is management-heavy, highly seasonal, or difficult to resell. Lower gross yield can be acceptable if occupancy is stable and the exit market is deep.

The cost stack is where many overseas buyers misprice Spain

Purchase price is only the start of the underwriting. UK investors should model the full capital stack before deciding whether a region fits an income strategy, a capital preservation strategy, or a residency-led purchase.

Your assumptions should include:

- Acquisition costs, including transfer taxes or VAT where relevant, legal fees, notary charges, and registration

- Finance costs, including arrangement fees, interest, and the effect of currency movements on sterling-funded buyers

- Holding costs, such as insurance, local taxes, maintenance, utilities during void periods, and community fees for apartment stock

- Operating costs, especially cleaning, key handling, platform fees, and local compliance if the property depends on short-term lets

- Vacancy and arrears risk, based on the tenant profile of that specific micro-market

The comparison between the Big Four and the islands sharpens. Madrid and much of Valencia usually offer simpler income models because the demand base is wider and less seasonal. Barcelona can still work well, but mistakes are expensive because entry pricing leaves less room for weak underwriting. Costa del Sol returns can look attractive on paper, yet they depend more heavily on occupancy patterns and professional management. The Balearics suit investors who prioritise scarcity and wealth preservation. The Canaries suit buyers willing to accept a more operational model in exchange for stronger tourism-linked income potential.

Match the region to the return model

| Return model | Best suited locations | Main risk |

|---|---|---|

| Long-term urban rental | Madrid, Valencia, parts of Barcelona | Regulation, affordability pressure, slower rental growth if supply expands |

| Short-term or seasonal income | Costa del Sol, Canaries, selected Balearic submarkets | Occupancy swings, licensing constraints, higher operating intensity |

| Hybrid personal use plus rental | Costa del Sol, Valencia, selected islands | Calendar friction, inconsistent occupancy, management complexity |

| Lifestyle-led capital preservation | Prime Madrid, prime Barcelona, premium Balearic stock | Lower income yield and high entry costs |

For UK investors, the non-obvious point is that the highest-yielding market is not always the best long-term investment. If post-Brexit residency, occasional personal use, and a future resale to another international buyer all matter, a slightly lower-yield but more liquid market can produce the better overall outcome. If the target is income first, the right comparison is not Barcelona versus Valencia on price alone. It is whether the property can deliver dependable net income after costs, with a tenant or guest profile that still holds up in a softer market.

A Step-by-Step Guide to Buying Property in Spain

Buying in Spain is procedurally straightforward once the sequence is right. Problems usually start when overseas buyers treat reservation paperwork as informal, rely on the selling side for legal guidance, or mistake a cheap listing for a low-risk purchase.

Start with independence. Your lawyer should represent you, not the agent, developer, or seller.

The buying sequence that keeps risk under control

Appoint an independent abogado

This is the first decision, not an administrative detail. Your lawyer checks ownership, charges over the property, planning issues, and whether the seller can legally transfer title.Obtain your NIE and prepare funds

You will need the tax identification number used by foreign buyers. In parallel, organise proof of funds, banking arrangements, and mortgage discussions if financing is part of the plan.Run due diligence before committing fully

Don’t rely on brochure language or verbal assurances. Confirm the legal status of the property, any attached debts or obligations, and whether the intended use is compatible with local rules.

Treat the deposit stage seriously

The private deposit contract is where many buyers become exposed. Once signed, it has legal and financial consequences. Review the draft carefully, including completion timing, penalties, inventory if relevant, and what happens if defects emerge before closing.

For financing research, this guide to mortgage rates in Spain is a useful early-stage reference. It helps buyers decide whether financing should shape the search from day one or be treated as secondary.

A property is only a bargain if you can rent it, hold it, and exit it on sensible terms.

Completion happens at the notary, but risk is managed earlier

The notary formalises the transaction. It doesn’t replace your own legal due diligence. By the time you reach completion, the heavy lifting should already be done.

A sensible buyer will usually verify:

- Title position and the seller’s right to dispose of the asset

- Outstanding debts or charges attached to the property

- Building and community issues where relevant

- Use case compatibility, especially if rental income is part of the plan

This walkthrough gives a good visual overview of the process:

Be careful with inland “value” listings

The sharpest warning in the current market concerns depopulating rural areas. According to the verified data tied to the cited reference, Spain has 3,000+ ghost villages, and property values in some inland zones are falling by 15% annually because local demand is disappearing.

That does not mean rural Spain should be ignored. It means a low purchase price is not enough. A house in a depopulating village may be enjoyable for personal use, but it can be a poor investment if occupancy is weak and resale demand is thin.

A practical filter helps:

| If the property is cheap because… | Investor response |

|---|---|

| It needs cosmetic work | Assess renovation rationally |

| It is outside the main demand zone | Check rental and resale evidence |

| The local population is shrinking sharply | Treat as high-risk unless there is a very specific strategy |

For UK investors living in Spain part-time, the best acquisitions are usually the most legible ones. Good title, clear demand, manageable running complexity, and an obvious resale audience.

Integrating into Spanish Life Healthcare Schooling and Daily Practicalities

For UK buyers, the difference between a property that works as a long-term base and one that becomes a recurring administrative burden often comes down to factors outside the title deed. Healthcare access, school availability, banking setup, transport, and day-to-day service reliability all shape retention, tenant quality, and the practicality of post-Brexit relocation.

Healthcare is the first filter. For many UK pensioners and some other eligible residents, access can be arranged through the S1 form, which materially reduces out-of-pocket medical risk and makes Spain more workable for retirement-led moves. For investors comparing regions, that matters most in areas with an older buyer profile, especially parts of the Costa del Sol, the Balearics, and selected coastal zones in Valencia. Madrid and Barcelona offer deeper private healthcare networks, but they also tend to suit working-age households and internationally mobile professionals rather than purely retirement-driven relocators.

Schooling creates a second layer of regional divergence. Madrid and Barcelona generally offer the widest choice of international schools and bilingual options, which supports executive relocations and longer corporate tenancies. Valencia can be a stronger fit for buyers seeking a lower-cost family base without giving up urban infrastructure. The islands present a different trade-off. They can work well for lifestyle-led moves, but school choice is narrower and logistics become more important if a household expects curriculum continuity through secondary education.

Daily practicalities have direct investment implications. A delayed bank account, an unreliable utility transfer, or weak public transport can turn a theoretically attractive purchase into a difficult asset to occupy or let. That is one reason the Big Four zones, Madrid, Barcelona, Costa del Sol, and Valencia, usually look more resilient for lower-risk investors. Their appeal is not only demand depth. It is operational simplicity. The Balearics and Canaries can produce stronger seasonal income and a clearer lifestyle proposition, but the margin for administrative friction is higher, especially for part-time owners managing the property from the UK.

Household budgeting also needs to be location-specific rather than based on a generic “Spain is cheap” assumption. Running costs, transport habits, schooling choices, and private healthcare use vary sharply by region, so this guide to the cost of living in Spain is useful for testing whether a target location fits your income plan and residency goals.

Rental affordability is another point investors often underestimate. In stronger urban markets, local wage pressure can limit what tenants can sustain even where demand remains high. For landlords, the practical conclusion is straightforward. Underwrite conservatively, screen tenants carefully, and avoid assuming that headline demand automatically translates into stable occupancy. That issue is most relevant in Madrid and Barcelona, where liquidity is strong but affordability pressure can be higher. In Valencia and parts of the Canaries, lower entry prices can improve yield maths, but tenant quality still depends on microlocation and employment mix.

Pets add one more operational layer. For households relocating with animals, understanding pet travel compliance for Spain helps reduce avoidable delays and paperwork errors.

The broader investment point is clear. Spain works best for UK buyers who match region to objective. Madrid and Barcelona suit capital preservation, liquidity, and professional tenant demand. Costa del Sol and Valencia often offer a better balance between usability and income. The Balearics and Canaries can justify higher risk for buyers targeting lifestyle value, seasonal rents, or island residency outcomes, but only if they are prepared for tighter supply, more operational detail, and less margin for mistakes in everyday setup.