A familiar decision lands on many investors’ desks at the same point. You’ve found a UK property that fits the strategy, the legal system feels dependable, lenders understand the market, and the long-term case is easy to justify. Then the purchase structure becomes the primary question.

Buy in your own name, and the path is simpler. Buy through a limited company, and you may gain cleaner ring-fencing, a more professional portfolio structure, and better alignment with a long-term investment business. But the entry cost can rise sharply, and stamp duty is usually where that reality becomes impossible to ignore.

That’s why a stamp duty calculator for limited companies matters so much. It isn’t just a tax tool. It’s an underwriting tool. If the calculator is wrong, your projected return is wrong, your cash requirement is wrong, and your hold period assumptions may be wrong too.

International buyers often start with the company question before they even make an offer. If you’re still at that stage, a practical UK company formation guide can help you understand the setup side before you commit to the acquisition side. Market selection matters just as much, and broader comparisons in this global property investment outlook for 2025 can help you judge whether the UK still deserves capital ahead of other jurisdictions.

Investing in UK Property Through a Limited Company

A smart overseas investor usually isn’t asking whether a UK limited company is legally possible. It is. The key question is whether the structure improves the investment after tax, after financing costs, and after the administrative burden of running it properly.

For some portfolios, the answer is yes. A company can make the ownership structure easier to manage, especially where investors want a dedicated vehicle for one asset or one strategy. It can also make reporting and ownership boundaries cleaner when multiple shareholders or family offices are involved.

The problem is that many buyers treat the company itself as the strategy. It isn’t. It’s only a wrapper. If that wrapper adds a heavy acquisition tax cost, the property has to work harder from day one.

Where investors usually get caught out

The most common mistake is using a generic SDLT calculator aimed at owner-occupiers. That produces a figure that looks plausible but doesn’t reflect the corporate rules. The second mistake is focusing only on rental income and forgetting that SDLT is a front-loaded cost paid before the asset has produced any return.

That changes decision-making in practical ways:

- Offer discipline: A deal that works at one purchase price may stop working once company SDLT is added.

- Cash planning: The tax bill affects deposit allocation, legal budgets, and reserve capital.

- Market choice: The same capital may stretch further in one UK sub-market than another, or outside the UK entirely.

A corporate purchase can still be the right move. But if you don’t price SDLT correctly at the start, you’re not investing. You’re guessing.

Why the UK still attracts corporate buyers

The UK remains attractive because investors value the legal framework, established conveyancing process, lender familiarity, and the depth of the market. Those strengths are real. They also explain why many international investors still accept a higher upfront tax burden if the long-term business case is sound.

That said, the UK should be judged against alternatives. In markets such as the UAE, Portugal, or parts of the USA, the choice of holding vehicle may produce a different balance between tax, asset protection, financing, and exit flexibility. The UK remains viable, but it rewards investors who model every acquisition cost properly before exchange.

Corporate SDLT Fundamentals Why Companies Pay More

A company bidding £600,000 for a UK residential asset can be materially behind an individual investor before either has collected a month of rent. That is the first corporate SDLT reality to price in. The UK still offers legal certainty, lender familiarity, and a deep resale market, but the entry tax for companies is one of the clearest reasons some international investors end up preferring a different holding structure in the UAE, Portugal, or parts of the USA.

Stamp Duty Land Tax applies to property purchases in England and Northern Ireland. For residential acquisitions, a limited company is treated more harshly than many individual buyers because HMRC classifies companies as non-natural persons. In practice, that means no first-time buyer treatment and no assumption that the purchaser is acquiring a main home.

HMRC’s guidance on SDLT for corporate bodies sets out the corporate position. For limited companies buying residential property, the rate structure can reach 17% in the highest band, and a £600,000 purchase can produce roughly £50,000 of SDLT. For an investor, the point is simple. This is dead capital on day one.

If you are weighing company ownership against personal ownership, portfolio investors should also review the wider second home tax implications because the surcharge logic is part of the same acquisition-cost problem.

The practical reasons costs rise

For most residential purchases, companies pay the higher rates that apply to additional dwellings. HMRC assumes the buyer is not an owner-occupier, so the purchase starts from a more expensive tax position.

Overseas investors need to watch the residency point as well. A non-UK resident company buying residential property can face an additional 2% surcharge. On a larger acquisition, that changes more than the tax line. It affects cash left for refurbishment, debt service cover, and contingency.

This is one reason UK incorporation is not automatically the right answer for an international buyer. In some markets, corporate ownership is relatively neutral at acquisition and the planning focus sits more on financing, liability protection, or exit. In the UK, SDLT can be the factor that makes the structure uneconomic unless the asset has strong yield, strong appreciation prospects, or a longer hold period.

What this means for returns

SDLT does not improve the building or increase rent. It raises your all-in basis.

That matters most in four situations:

- Short hold periods. You have less time to recover the upfront tax.

- Lower-yielding assets. More of the return is consumed by acquisition friction.

- Refinance-led strategies. Front-loaded tax reduces flexibility and weakens early cash efficiency.

- Strategic assets. The company route can still work if control, asset protection, or portfolio planning justify the higher entry cost.

A good investor does not ask only, "What is the SDLT bill?" The better question is, "What return does this structure leave me after SDLT, financing, and exit costs?" That is the comparison that matters if you are deciding whether UK corporate ownership beats a direct purchase, or whether your capital works harder in another jurisdiction.

Practical rule: Add SDLT to your true acquisition cost at the underwriting stage. If that combined basis pushes the deal below target return, either the price is too high or the company structure is the wrong vehicle.

For many international buyers, this is the point where the UK stops being a generic property market and becomes a structuring decision.

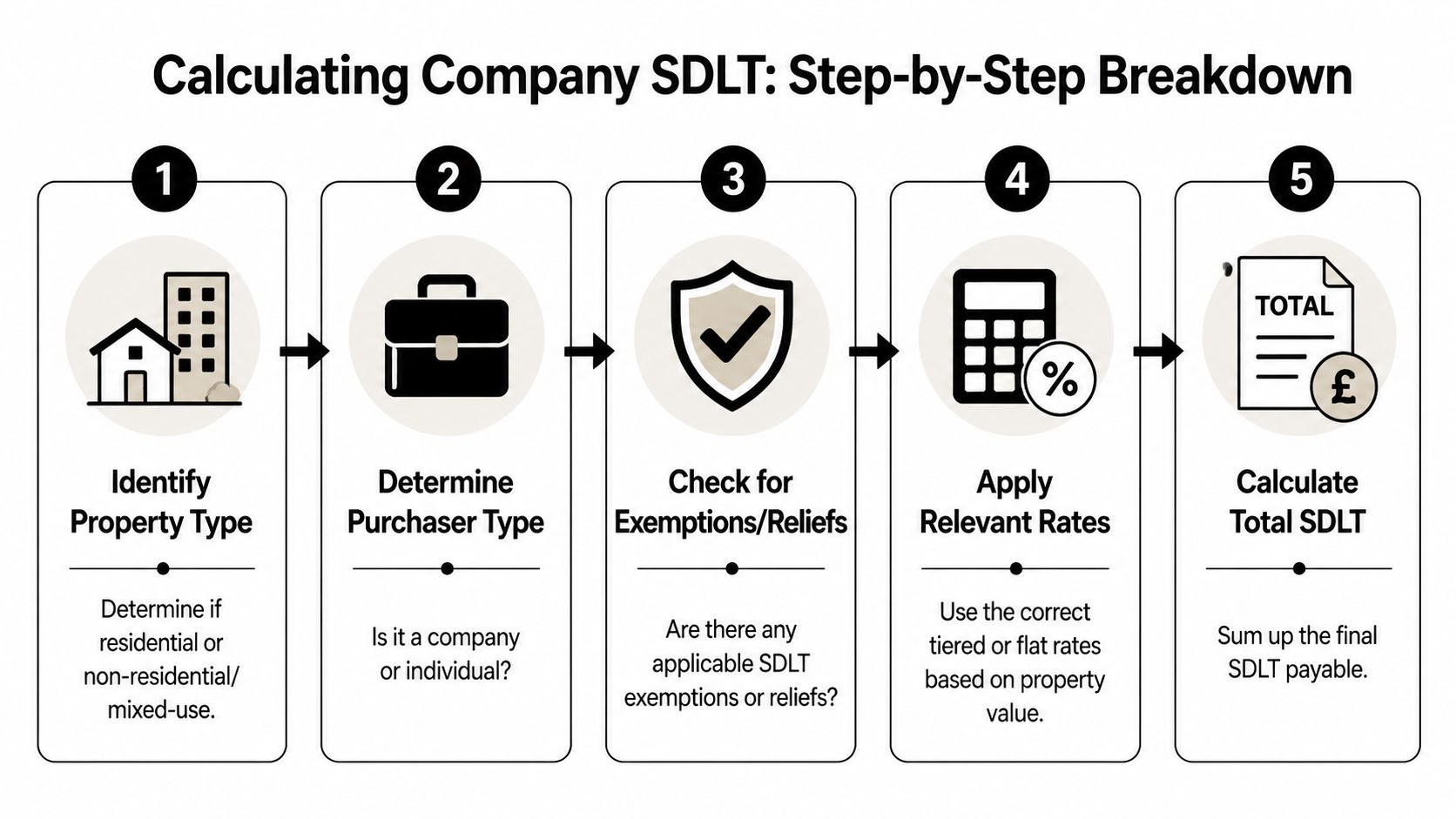

Calculating Stamp Duty A Step-by-Step Breakdown

A Dubai investor agrees terms on a £600,000 buy-to-let in Manchester through a UK company. The headline yield looks acceptable. Then the SDLT goes in, and the entry cost shifts enough to change the return case against buying through an SPV in the USA or holding property more lightly in markets such as the UAE. That is why the calculation needs to be exact before exchange, not corrected afterwards.

For a company buying residential property in England and Wales, SDLT is usually calculated on a slice basis using the higher rates that apply to corporate buyers. As noted earlier, a £600,000 purchase can produce a £50,000 SDLT bill under the standard company rate structure. The point is not the arithmetic alone. The point is what that tax does to your cash deployment on day one.

Use the calculator in the right order

A reliable stamp duty calculator for limited companies should help you test four points in sequence.

- Classify the asset correctly. Residential, mixed-use, and non-residential deals do not use the same SDLT treatment.

- Set the buyer status correctly. The calculator must treat the purchaser as a company from the start.

- Check for any override to the standard banded calculation. This matters on higher-value residential acquisitions and on deals where reliefs may apply.

- Apply the rates to each slice of value. SDLT is marginal, so each band is taxed at its own rate, not by applying one percentage to the whole price.

For a quick sense check, this BTL stamp duty calculator for investors is useful, but company purchases still need a manual review of the assumptions behind the result.

Company rates against an individual additional-property buyer

Many investors assume a company pays the same surcharge as an individual buying an extra property. That is only partly true. The practical risk is using the wrong setting on a generic calculator and underwriting the wrong acquisition cost.

| Property Value Band | Standard Additional Property Rate (Individual) | Corporate Rate (with 3% surcharge) |

|---|---|---|

| £0 to £125,000 | 5% | 5% |

| £125,001 to £250,000 | 5% | 7% |

| £250,001 to £925,000 | 10% | 10% |

| £925,001 to £1.5m | 15% | 15% |

| Above £1.5m | 17% | 17% |

That difference in the £125,001 to £250,000 band is not huge in isolation, but it is enough to distort your model if you are comparing several deals across jurisdictions and assuming the UK company route is broadly similar to other holding structures.

Worked example on a £600,000 purchase

Take a residential purchase at £600,000 by a limited company.

The SDLT is charged in slices:

- First £125,000 at 5%

- Next £125,000 at 7%

- Remaining £350,000 at 10%

That produces total SDLT of £50,000.

This is the part many calculators hide. If the tool shows only one headline percentage and no band-by-band breakdown, it is not good enough for an acquisition decision. A professional buyer needs to see how the figure was built, because the next question is always whether a different structure, a different asset class, or a different market leaves more capital working for the portfolio.

What a useful calculator should tell you

A serious investor needs more than a tax total. You need enough detail to decide whether the UK company purchase still clears your return hurdle after SDLT, finance costs, and expected hold period.

Look for these outputs:

- Band-by-band calculation. You should be able to audit the number quickly.

- Property type prompt. The tool should ask whether the asset is residential, mixed-use, or non-residential.

- Buyer status prompt. Company and individual transactions should not be merged into one default result.

- Warning flags for exceptions. Higher-value corporate residential purchases need extra care.

- Clear assumptions. If the calculator does not show what it assumed, treat the answer as provisional only.

For international buyers, that last point matters more than it first appears. In some markets, transfer taxes are lower, flatter, or easier to model. In the UK, SDLT is front-loaded and structure-sensitive. If you are using a company, the calculation is part of the investment thesis, not an admin step.

The High-Value Property Trap The 15% Flat Rate

Many investors encounter an unpleasant surprise when they use a standard company calculator, see a progressive banded result, and assume the SDLT is settled. On certain residential purchases, it isn’t.

A known weakness in many calculators is that they do not properly account for the 15% flat SDLT rate for non-natural persons buying a single residential property over £500,000. The MFBrokers calculator guidance notes that this flat rate overrides the progressive bands and is frequently missed, even though exemptions may apply for genuine property letting businesses. The same source states that for a £600,000 property, the SDLT can jump from about £32,500 under standard corporate bands to a flat £90,000.

For investors targeting prime and upper-mid-market areas, that difference can change the viability of the deal immediately. It can also reshape your view of London pricing if you’re already comparing stock in the capital through this guide to the average price of a flat in London.

When the trap matters most

This issue tends to arise when buyers assume every company purchase follows the same marginal band structure. It doesn’t. On certain high-value residential acquisitions, the flat rate can override the usual calculation.

That is especially dangerous in the following situations:

- Single-asset corporate purchases in higher-value postcodes

- Cross-border buyers relying on generic portal calculators

- Investors buying for occupation by connected persons

- Deals reviewed late in the process, after price and funding assumptions are already fixed

The commercial test matters

The critical distinction is whether the purchase falls within a genuine business exemption. The MFBrokers guidance makes the point that genuine property letting businesses may avoid the flat-rate treatment where an exemption applies. That means the question is not just “what is the price?” but also “what is the company doing with the property?”

Many tax mistakes happen because investors ask only for a number. They should ask for a classification, an exemption review, and then the number.

Adviser quality is paramount. A conveyancer may process the completion efficiently, but if nobody has tested whether the flat rate could apply, the SDLT estimate may be incomplete. On premium purchases, that is not a minor error. It is a structural underwriting error.

Strategic Reliefs to Reduce Your Company's SDLT Bill

A company agrees terms on a UK property, runs a quick SDLT estimate, and assumes the tax cost is fixed. Then legal review shows the asset is mixed-use, or the intended business activity supports a relief that was never priced into the deal. I see this change returns more often than investors expect.

The best SDLT savings usually come from getting the facts right before exchange. Once a company is committed to a straightforward residential purchase, options narrow fast. Good planning here is rarely about aggressive tax engineering. It is about classification, evidence, and choosing a structure that matches the actual commercial use of the property.

Some investors also read Top Wealth Guide's tax insights as general background on lawful tax planning. That is useful up to a point. For UK property, the return on advice comes from deal-specific analysis, not generic ideas.

Mixed-use often changes the conversation

Mixed-use treatment can reduce SDLT sharply, but only when the asset includes a commercial element. A shop with a flat above it, a parade unit, or a building with credible non-residential use can fall into a different charging regime from an ordinary company purchase of a residential dwelling.

The practical point is simple. A correct mixed-use classification can matter more than negotiating a small price reduction.

Investors buying converted buildings or split-use stock should also look closely at tenure and operational control. A property that is awkward to manage or legally fragmented can weaken the business case even if the SDLT result is better on paper. This guide to leasehold versus freehold ownership structures is useful background if you are comparing assets with different rights and restrictions.

Key point: Mixed-use treatment depends on facts you can defend. Floor area, access arrangements, leases, planning position, and actual use all matter.

Reliefs work when the business activity is real

Reliefs do not rescue a weak file. They work when the company is carrying on a genuine business activity and the documents support that position.

In practice, that usually means four things:

- The business purpose is clear: The company's intended use of the property must fit the relief being claimed.

- The evidence is specific: Tenancy terms, plans, board minutes, marketing material, and funding papers should point in the same direction.

- The structure is chosen early: Relief analysis done after exchange is less persuasive and often less useful.

- The file is well-documented: If HMRC reviews the transaction later, the paperwork should show why the treatment was adopted.

A short explainer helps here:

What tends to hold up under scrutiny

The strongest SDLT positions are commercially ordinary. A genuine mixed-use building is taxed as mixed-use. A real property rental business with the right facts may qualify for a better result than a generic online calculator suggests. The legal analysis follows the asset and the business model.

Weak positions usually fail for predictable reasons. The company buys a standard residential property, someone adds a tax label late in the process, and the facts never support that label. HMRC will usually look past the wording and focus on the substance of the deal.

For international investors, this is one of the UK's defining trade-offs. The UK gives you a clear legal framework, reliable title, and an institutional lending market, but entry tax is technical and front-loaded. In the UAE, Portugal, or parts of the USA, acquisition taxes may appear simpler or lower at the outset, yet the wider ownership, financing, reporting, or exit picture can be less predictable. The right question is not whether the UK has reliefs. It is whether the UK company structure still produces the best after-tax return for your portfolio once SDLT, financing, compliance, and exit are all priced in.

Alternative Structures Share Transfers and SPVs

Once you move from one purchase to portfolio building, direct acquisition is not the only route worth examining. Structure starts to matter as much as asset selection.

Why investors use SPVs

A special purpose vehicle, or SPV, is a limited company set up to hold a property or a defined group of properties. Investors use SPVs to isolate liabilities, separate strategies, and make ownership cleaner for lenders, partners, and future buyers.

That doesn’t make an SPV a tax shortcut. It is an organisational tool first. The tax outcome still depends on what the vehicle buys and how the acquisition is structured.

SPVs tend to work well when an investor wants:

- Ring-fenced risk: One project doesn’t contaminate another.

- Clear reporting: Accounts and financing are easier to track.

- Transaction flexibility: It may be easier to sell the company than the asset in some circumstances.

- Defined ownership: Shareholdings can reflect partnership terms more neatly than direct title.

Share purchase versus property purchase

The more strategic question is whether you are buying the property itself or buying the company that already owns it.

According to Quality Company Formations on stamp duty for limited companies, share transfers are subject to Stamp Duty at 0.5% on transactions over £1,000, rounded up to the nearest £5. The same guidance explains that this is separate from SDLT on direct property purchases.

That difference is why knowledgeable buyers sometimes consider a share acquisition. Instead of buying the building and paying property SDLT, the buyer acquires the shares in the property-holding company and pays stamp duty on the shares.

The trade-off that matters

The tax on the shares may be lower, but you inherit the company. That means you may inherit its history, contracts, accounting issues, compliance gaps, and legal risks along with the property.

So the decision becomes commercial, not just tax-driven.

| Route | Main tax point | Main risk point |

|---|---|---|

| Direct property purchase | Property SDLT applies | Cleaner title path, higher transaction tax |

| Share acquisition | Share stamp duty may apply instead | You acquire company-level liabilities with the asset |

Lower transaction tax is attractive. Inherited corporate risk is real. The buyer has to decide which problem is easier to manage.

Proper due diligence transforms the situation. On a share deal, tax, legal, accounting, and property diligence all need to work together. If they don’t, a saving at entry can be replaced by a problem you didn’t price in.

Filing Your Return Payment Deadlines and Compliance

Once completion happens, the technical debate ends and the administrative deadline starts. This part is not optional and it is not forgiving.

According to the Tax Wise guidance on limited company SDLT, a UK limited company must file an SDLT return and pay the tax due within 14 days of completion. The same source warns that late compliance can trigger HMRC penalties and daily interest.

What needs to happen after completion

The filing process is usually handled with support from the conveyancer or tax adviser, but the company remains responsible for getting it right. In practical terms, that means the final purchase details, buyer identity, property classification, and tax treatment all need to be settled immediately after completion.

The compliance sequence is straightforward:

- Confirm the final tax position

- Submit the SDLT return

- Pay the SDLT due

- Keep evidence of the filing and payment

- Ensure registration can proceed without delay

Why timing matters so much

Late filing does more than create nuisance. It damages returns. If capital is already tight because of deposit, legal fees, and refurbishment costs, an avoidable penalty is one of the least productive uses of cash in the whole transaction.

For non-resident companies, there is an additional practical issue. The acquisition analysis must already have considered whether the non-resident surcharge applies before completion funds are finalised. If the wrong amount has been budgeted, the payment deadline becomes even more dangerous because the company may be scrambling for extra liquidity after the deal has already closed.

SDLT compliance should be prepared before completion, not delegated after it. The return is an execution task, but the tax position needs to be settled earlier.

What works in practice

The smoothest transactions tend to share the same habits:

- The calculator result is checked manually before exchange

- The buyer’s residency status is confirmed early

- The company details are finalised before completion day

- Funding for SDLT is ring-fenced, not treated as spare cash

- One adviser owns the timetable, even if several advisers are involved

What doesn’t work is leaving the SDLT calculation to the end because the number “won’t change much”. On corporate purchases, it can.

Conclusion Is a UK Corporate Structure Right for Your Portfolio

A UK limited company can be the right vehicle for a serious property portfolio. It offers a formal ownership structure, cleaner risk separation, and a framework that many lenders, solicitors, and professional investors understand well.

But the SDLT cost is not a side issue. It is one of the main investment variables. If you buy through a company without testing the acquisition tax properly, you can damage returns before the asset has a chance to perform. That is why the right stamp duty calculator for limited companies is only the starting point. The actual job is interpreting the result in the context of yield, hold period, funding, and exit.

International investors should compare the UK objectively with alternatives such as the UAE, Portugal, and the USA. The UK often looks heavier on transaction tax, but stronger on legal certainty and market depth. Whether that trade-off works depends on your time horizon and your operating model.

If you want a broader view of how the company itself fits into the tax picture, this overview of navigating UK limited company taxes is a useful next read.

If you’re comparing UK deals with opportunities in other markets, World Property Investor gives you practical, research-driven guides on taxes, yields, buying structures, and market fundamentals across major global property destinations.