You bought the property as an investment. Then your plans changed.

That happens more often than many investors expect. A flat that looked ideal for tenants starts to look ideal for you. A relocation falls through. A short-term base becomes a long-term move. Or you decide that living in one of your own assets makes more sense than paying rent elsewhere.

The question sounds simple: can i live in my investment property? In practice, it sits at the intersection of mortgage terms, tax treatment, insurance cover, tenancy law, and local regulation.

Most costly mistakes happen because investors treat occupancy as a personal choice rather than a legal status. Lenders classify the property one way. Tax authorities classify it another way. Insurers use different assumptions again. If those don't match what you are doing, the risk compounds fast.

The right answer depends on three things. First, how the property is financed. Second, what country and local authority govern it. Third, whether your priority is flexibility, rental income, or long-term tax efficiency.

A move into your rental can be sensible. It can also be expensive, badly timed, or a direct breach of contract. The difference usually comes down to process. Investors who handle the transition properly preserve options. Investors who skip the paperwork often discover the problem only when they refinance, claim on insurance, or try to sell.

The Investor's Dilemma When You Want to Move In

The emotional logic is easy to understand. You sourced well, bought well, and now you know the property better than anyone. You trust the location, you like the layout, and you can see yourself living there. From a personal perspective, the decision feels rational.

From an investment perspective, it changes the whole file.

A rental property is underwritten on the assumption that it will function as an income-producing asset. The lender assesses a different risk profile. The insurer writes a different policy. Your tax position is built around a different use. If a tenant is in place, you also have contractual and statutory obligations that don't disappear because your plans changed.

Why investors get caught out

Problems arise when investors focus on the incorrect inquiry. They wonder if they can physically move in, when the significant question is whether they can do it without breaching finance terms, damaging tax efficiency, or creating legal exposure.

That distinction matters in every market.

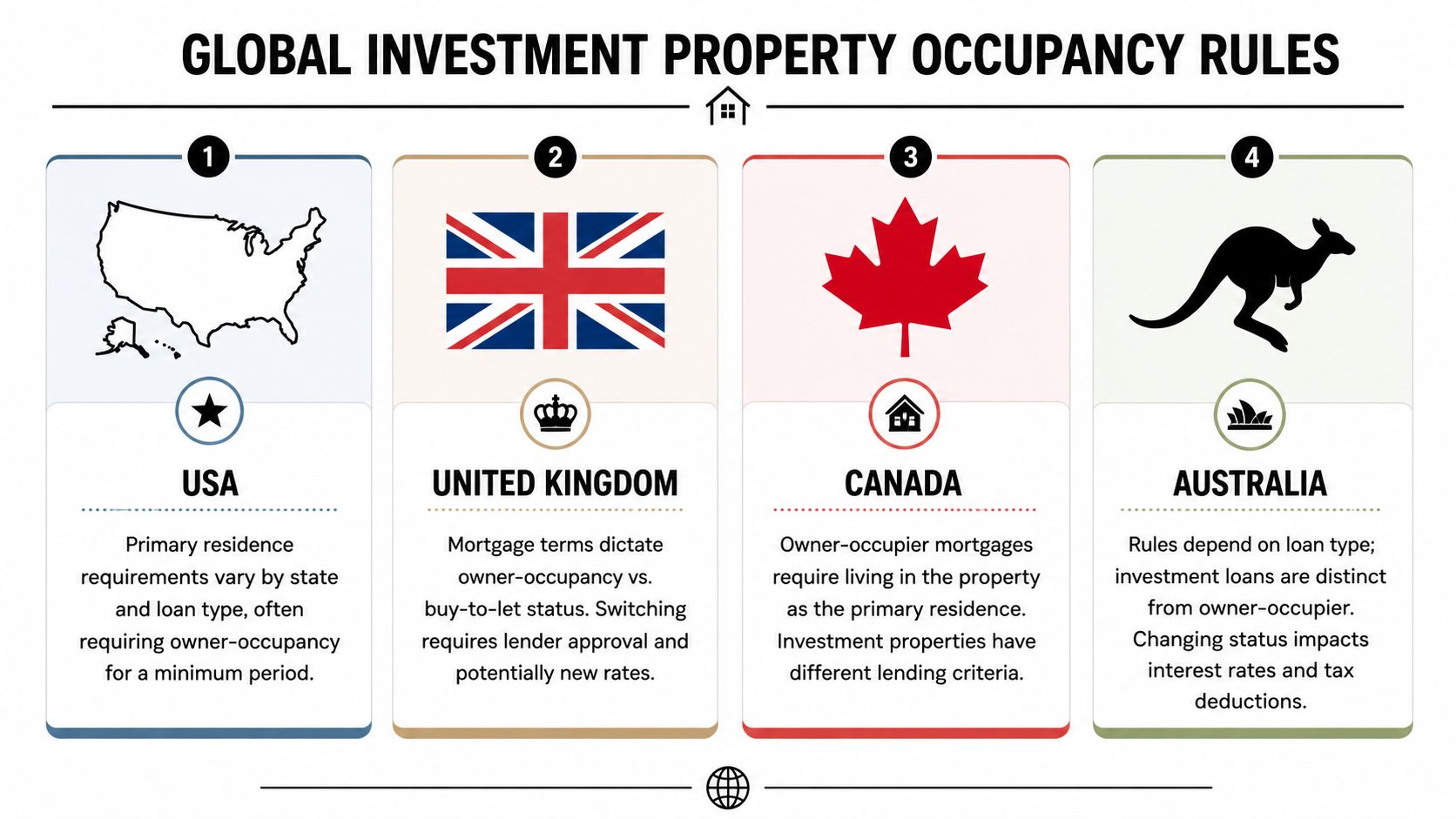

In established markets, the rules are usually clearer but less forgiving. In the UK, mortgage classification is strict. In the USA, there may be more room for owner-occupancy in certain structures, but financing and homestead rules still matter. In Spain, Portugal, and Dubai, ownership rights, residency status, and financing norms can interact in ways overseas buyers underestimate.

Practical rule: If the property was bought, financed, or insured as an investment, assume you need formal approval before you sleep there even one night as your home.

The four tests that matter

Before making any move, check the property against these four tests:

- Finance test: Does your mortgage allow owner-occupancy, or does moving in trigger a breach?

- Tax test: Will the property stay an investment for tax purposes, or does occupation change future capital gains treatment?

- Insurance test: Does your current policy still cover the building once you become the occupant?

- Legal test: Do you need vacant possession, licence changes, council tax updates, or local authority notifications?

When investors work through those four areas in order, the answer becomes clearer. Sometimes the right move is to remortgage and move in. Sometimes the right move is to keep the property as a pure rental and buy separately. Sometimes a hybrid model, such as a holiday-let structure where permitted, gives better flexibility.

Your Mortgage The First and Biggest Hurdle

A common investor scenario looks like this. The tenant leaves, the property is in a city you now want to live in, and moving into your own flat seems like the obvious next step. The problem is that your lender may still treat that address as an income-producing asset, not a home, and that difference can trigger a breach before you even change the utility bills.

Your mortgage contract usually decides the issue first. Tax planning, insurance changes, and local registration all matter, but the lender has the earliest and most immediate enforcement power.

Lenders do not treat all property borrowing the same way. A residential mortgage is priced and underwritten for owner-occupation. A buy-to-let or investment loan is assessed on rental income, tenant risk, vacancy assumptions, and a different enforcement model. If you change the occupancy without approval, you are not making a casual lifestyle change. You are changing the basis on which the loan was granted.

That applies well beyond the UK. In the USA, occupancy declarations on loan documents can affect underwriting, pricing, and, in serious cases, whether the lender alleges misrepresentation. In Spain and Portugal, the issue often appears during refinancing because banks separate owner-occupier products from non-resident and investment borrowing. In Dubai, investors also need to check whether the original finance offer, developer terms, and building rules all align before treating a unit as a primary residence.

Why lenders react so strongly

From a lender's perspective, owner-occupiers, second-home borrowers, and landlords present different risks. Affordability tests differ. Interest rates and deposit expectations differ. Arrears patterns differ. Even the valuation logic can differ if the original case relied on rental yield.

That is why informal assumptions cause problems. Owning the property does not give you the right to ignore the mortgage conditions attached to it.

If you move into a buy-to-let property without written approval, the consequences can include:

- A formal breach of mortgage conditions

- A demand to switch products or refinance

- Early repayment charges if you have to exit the current loan

- A call for full repayment in more serious cases

- Problems with linked insurance because the occupancy status no longer matches the file

Consent to let does not solve the reverse problem

I see this misunderstanding often. Borrowers hear the phrase consent to let and assume there must be an equivalent informal permission to move into a rental property they already own.

Usually there is not.

Consent to let normally means a lender with a residential mortgage allows temporary letting. It does not usually mean a lender with a buy-to-let mortgage allows owner-occupation on the same terms. If you want to live there, the practical route is often a product transfer or a full remortgage onto residential or second-home terms. For a useful benchmark on how lenders assess those cases, review these second home mortgage requirements.

The process that keeps you compliant

The legal route is rarely complicated in theory. It is just easy to mishandle in practice.

| Step | What usually happens |

|---|---|

| Read the mortgage offer and conditions | Check occupancy clauses, borrower declarations, notification duties, and early repayment charges |

| Contact the lender before moving in | Ask whether owner-occupation is permitted and what approval process applies |

| Prepare for a new underwriting decision | Expect income checks, credit review, property valuation, and updated affordability testing |

| Price the switch properly | Factor in product fees, legal fees, valuation costs, broker fees, and any exit penalties |

| Wait until the paperwork matches reality | Do not move in while the mortgage, insurance, and property records still describe the home as a rental |

Global investors can often get caught out by these differences. In the UK and USA, the paperwork is often stricter and the categories are more clearly defined. In Spain, Portugal, and Dubai, overseas owners sometimes assume a bank will treat owner-use as a harmless internal change. Many banks will not. They may require a fresh application, especially if your residency, income source, or currency profile has changed since the original purchase.

There is also a tax-linked mortgage issue in the United States. If a borrower starts claiming homeowner treatment, local benefits may depend on the property being their principal residence. The rules vary by state, but this example of Texas principal residence tax rules shows how occupancy status can carry legal and financial consequences outside the loan itself.

A short explainer on owner-occupancy mortgage issues can help frame the lender's perspective:

Moving into a financed rental without lender approval is a mortgage event, with legal and financial consequences that can be expensive to reverse.

Understanding the Tax and Capital Gains Transformation

You buy a flat as a rental, hold it for several years, then decide to move in yourself. From that date, the property is no longer just an income-producing asset. It starts building a different tax history, and that change affects far more than the final sale.

For many investors, the main issue is capital gains treatment. A property held as an investment is usually taxed differently from a property that qualifies as your main home. Living there may improve the outcome for part of your ownership period, but it can also end or reduce deductions, allowances, or reliefs linked to letting activity.

The first tax question to answer

Start with one clear question. Will this become your main home, or are you only planning occasional personal use?

Tax authorities often treat those two facts very differently. In the UK, owner-occupiers may qualify for Principal Private Residence relief for eligible periods, while pure rental periods are usually assessed under investment rules. If you want a practical refresher on how disposal is taxed, this guide on capital gains tax on property is a useful starting point.

Mixed-use history needs careful records. Keep purchase documents, tenancy agreements, move-in dates, council tax or utility evidence, and any residence declarations filed in that jurisdiction. If the property was rented first and occupied later, the gain is commonly apportioned by period of use, so weak records often turn into expensive arguments.

The real trade-off after you move in

Investors often assume owner-occupation automatically improves the tax position. Sometimes it does. Sometimes it changes which tax advantages you give up.

A former rental that becomes your home may stop generating deductible letting expenses from the date you occupy it. If you were relying on rental losses, local depreciation rules, or interest treatment linked to an investment loan, that benefit can shrink or disappear. At the same time, you may begin building a period of owner-occupation that improves the capital gains position later. The right answer depends on holding period, expected appreciation, rental yield, and your personal tax residence.

That trade-off looks different across markets. In the UK and USA, the distinction between investment use and principal residence use is usually formal and heavily documented. In Spain and Portugal, the local tax result can also turn on whether the property is your habitual residence and whether you have completed the right registrations. In Dubai, the capital gains question is less central than in many Western markets, but occupancy status can still affect financing, service charge assumptions, and how the asset fits your wider residency and portfolio plan.

Hybrid use needs more caution than investors expect

Some owners want a middle path. They plan to live in the property part of the year and rent it for the rest.

That can work, but only if the local rules allow a tax classification that matches the facts. In the UK, for example, some investors look at Furnished Holiday Let treatment because it may offer different tax outcomes from standard residential letting. The risk is practical, not theoretical. If your occupancy pattern, availability, or records do not meet the tests, the authority can treat the property under ordinary letting rules instead.

Intent is not enough. Your filings must match your actual use.

Cross-border owners need a country-by-country review

This point matters most for international investors. One country may decide whether the property is an investment or a main residence. Another may decide whether you, personally, are tax resident there. Those two decisions do not always line up cleanly.

For US property, state-level benefits can be tied tightly to genuine principal residence use. This overview of Texas principal residence tax rules is a good example of how local tax relief can depend on actual occupancy, not just ownership.

Use a simple decision frame before you change status:

- Keep it as an investment if rental income and investment deductions still produce the stronger long-term result.

- Convert it to your home if you expect to live there in a real, provable way and the future tax outcome justifies giving up landlord treatment.

- Consider hybrid use only after local advice confirms that the tax category, reporting obligations, and personal-use pattern all fit together legally.

Managing Tenancies Insurance and Local Regulations

Even if the mortgage and tax position can be fixed, you still have the operational work. Many investors make preventable errors during this stage because the tasks feel administrative rather than strategic.

They aren't administrative. They are legal.

If a tenant is in place, vacant possession comes first

You can't decide to move in because you own the asset. If a tenant occupies the property under a valid agreement, you need lawful vacant possession before you do anything else.

That means reading the tenancy agreement, understanding the local eviction and notice framework, and avoiding informal arrangements that look convenient but create later disputes. Don't book removals on the assumption that the tenant will “probably leave on time”. Until the property is lawfully vacant, your move-in date is provisional.

For investors with US property, state-level rules vary sharply. A practical example is this guide to essential laws for California property owners, which shows how local landlord-tenant rules can shape what is possible and how long it may take.

Insurance must match occupancy

A landlord policy is written on the basis that the property is let. Once you become the occupant, that assumption changes.

If you move in without updating the insurer, you risk discovering the problem only when there is a claim. Buildings insurance may still exist in some form, but disclosures matter. Contents cover, liability assumptions, unoccupancy wording, and use-class details can all be affected.

Use this quick checklist before you sleep in the property as an owner-occupier:

- Call the insurer before the move: Tell them the exact date occupation changes.

- Ask for written confirmation: Verbal reassurance from a call centre isn't enough.

- Replace landlord cover where needed: You may need standard owner-occupier buildings and contents insurance.

- Check any overlap period: If the property is empty between tenant exit and your move-in, the vacant period may have its own conditions.

Local authority and licence issues

The next layer is local administration. This changes by jurisdiction, but the issues are broadly consistent.

If the property was previously run as a rental business, holiday let, or licensed shared house, your local authority records may need updating. Council tax status, local registration, waste arrangements, and licence conditions can all be occupancy-sensitive.

A practical review should include:

| Area | What to check |

|---|---|

| Council tax or local charges | Whether the property needs to move from a rental or business-related basis to owner-occupier treatment |

| Landlord registration | Whether you must update or cancel existing registrations |

| HMO or similar licence | Whether your new use breaches licence conditions or occupancy assumptions |

| Utility accounts | Whether accounts need transferring from landlord or managing agent setup into personal use |

| Management agreements | Whether a letting agent must be formally instructed to stop marketing or management |

For investors using technology to manage the handover, even a simple workflow tool can help avoid missed steps. If you're moving from active rental management to self-occupation, a review of landlord systems in this guide to the best rental property app can help you close out the operational side cleanly.

If your file still says “tenanted investment” while you are living in the property, you haven't finished the transition.

A Global Snapshot Rules in Key Investor Markets

The best way to think about this internationally is simple. The question isn't “Can owners live in their own property?” Of course they can in a broad sense. The main issue is whether the property was acquired, financed, licensed, and taxed on terms that still allow that use.

UK

The UK is one of the clearest examples of strict mortgage separation between owner-occupier and investment use. If the property sits on a buy-to-let mortgage, the financing terms usually control what happens next. That makes the UK relatively predictable, but not especially flexible.

Tax treatment can also improve for periods when the property becomes your main home, yet the route there still needs careful handling. This is a market where investors should assume documentation comes before occupation.

USA

The USA often feels more flexible because owner-occupancy can sit inside certain investment-style strategies. Multi-unit ownership, room letting, and “house hacking” are all more culturally familiar there than in the UK. But flexibility in the market doesn't mean one rule nationwide.

State law, loan type, insurer requirements, and local tax status all matter. A borrower who bought on owner-occupier terms may have one set of obligations. A borrower who bought on investment terms may have another. The idea is broader than the rule, which means due diligence has to be more local.

Spain

Spain is often attractive to global investors who may want part personal use, part rental income. The key practical issue is usually not whether ownership allows occupancy, but whether your financing, community rules, and tax reporting support the way you plan to use the property.

If you're non-resident, the distinction between private use and income-producing use can affect tax filings and compliance expectations. In some buildings or municipalities, short-term rental restrictions can also shape whether the property works better as a home, a holiday asset, or a conventional let.

Portugal

Portugal has historically appealed to buyers who want lifestyle and investment in one asset. That can work, but the investor should still separate three questions: can you own it, can you reside in it, and can you monetise it on the basis you expected?

For some buyers, especially internationally mobile ones, visa and residency planning also sit alongside the property decision. If residency options are part of your wider plan, this guide to an investor visa gives a broader framework for how property can fit into cross-border mobility decisions.

Dubai

Dubai usually offers a different dynamic again. Foreign ownership in designated areas, developer rules, service charges, and bank underwriting can create more room for direct personal use than in classic UK buy-to-let structures. But the commercial logic still matters.

A property bought for yield may stop performing as a yield asset the moment you occupy it. In Dubai, that decision can be entirely lawful and still be financially weak if your acquisition assumptions were built around leasing demand rather than personal lifestyle value.

A practical comparison

| Market | Main friction point when moving in | Investor mindset that works |

|---|---|---|

| UK | Mortgage classification and occupancy clauses | Treat occupancy as a refinance and compliance exercise |

| USA | State-level variation and loan-specific rules | Verify local financing and residence definitions |

| Spain | Tax reporting, local rules, and community restrictions | Separate personal use from rental strategy clearly |

| Portugal | Residency planning and use classification | Align property use with visa, tax, and exit goals |

| Dubai | Commercial trade-off more than classic buy-to-let rigidity | Test whether lifestyle use still supports portfolio logic |

Established markets usually have clearer legal frameworks. Emerging or internationally popular expat markets often offer more practical flexibility, but less forgiveness for sloppy compliance. In both cases, the disciplined investor wins.

Your Action Plan Before You Move Your Boxes

The right move is rarely the fastest one. It's the one that survives lender review, tax scrutiny, and an insurance claim.

Before you move in, run through a proper decision sheet. If any answer is uncertain, pause until it is resolved in writing.

Ask these questions in order

What does my current mortgage allow?

Read the offer, not your memory of the offer. If the property is financed as an investment, speak to the lender before changing use.Can I qualify for the replacement finance if needed?

Don't assume income, stress testing, or product availability will work in your favour.Is the property vacant, and can I obtain lawful possession?

If a tenant is in place, your personal timetable doesn't override their legal rights.What happens to my tax position if I move in?

Model future capital gains treatment, loss of rental deductions, and any hybrid structure you may be relying on.Will my insurance still respond after the move?

Occupancy type, vacant periods, and contents assumptions all need updating.Which authorities or administrators need to be told?

Think local authority, licence register, utility providers, freeholder or block manager, and any managing agent.

The simplest way to make the decision

Investors usually fall into one of three camps:

- Move in and formalise it fully: Best when the property becomes your home and the financial trade-off still works.

- Keep it as a pure investment: Best when yield, financing, and tax treatment are stronger than the lifestyle benefit.

- Use a compliant hybrid model: Best only where the local rules clearly permit it and you can meet them consistently.

If you're unsure which path fits, go back to fundamentals. What is the asset for now? Income, flexibility, or residence? A property can do more than one job over its lifetime, but not all at the same time under the same paperwork.

For investors refining portfolio strategy more broadly, these investment property tips can help you assess whether a personal-use switch supports or weakens your long-term plan.

A good property decision is one you can still defend two years later to a lender, an insurer, a buyer, and a tax adviser.

The short answer to can i live in my investment property is this: sometimes, yes. Casually, no. If you treat the move as a formal change of use and document it properly, you protect both the asset and your options.

If you're comparing countries, tax treatment, rental models, and investor rules before making your next move, World Property Investor publishes detailed global guides to help you research markets, structure purchases, and invest with more confidence.