You're probably looking at Greece for the same reasons most international buyers do. Lifestyle demand is obvious, the stock ranges from Athens apartments to island villas, and the rental story can look compelling at first pass. Then the tax questions start. Is the buyer treated as a resident or a non-resident? What happens once rent starts coming in? Does a simple holiday-let plan trigger VAT? How expensive is it to hold the asset year after year?

Those are the right questions. In Greek property, the difference between a good investment and a frustrating one often comes down to tax treatment, compliance discipline, and how early you model the actual holding costs rather than the brochure version.

An Investor's Introduction to Greek Property Taxes

A common investor profile in Greece looks like this. Someone has narrowed their options to an Athenian apartment, a coastal home, or a unit in a tourism-led location. They've already compared prices, likely looked at gross rent assumptions, and may have read a market guide such as this overview on buying a home in Greece. What usually remains fuzzy is the tax layer that sits across the whole lifecycle of the asset.

That layer matters more in Greece than many first-time overseas buyers expect. The purchase itself is only the start. Holding costs continue. Rental income needs to be classified correctly. A passive long-let and a serviced short-term rental don't sit in the same tax box. If you change your personal circumstances and become Greek tax resident, the analysis can shift materially.

I advise clients to treat taxation in Greece as an underwriting item, not a legal footnote. If tax only appears at the end of your spreadsheet, your spreadsheet is wrong.

What usually works

The cleanest Greek property investments tend to share a few features:

- Clear residency position: The buyer knows from day one whether Greece will tax only Greek-source income or their wider income base.

- Simple income model: Straightforward residential letting is easier to run than a property with layers of hospitality-style services.

- Early compliance setup: Tax number, accountant, filing process, and documentation are arranged before completion or first rent.

- Conservative yield modelling: Net returns are tested after property taxes, income tax, local charges, and admin friction.

What tends to go wrong

Problems usually come from avoidable assumptions:

- Gross yield obsession: Buyers focus on headline rent and ignore the tax drag.

- Service creep: A holiday let starts as “just accommodation” and ends up looking like a taxable service business.

- Residency confusion: Time spent in Greece or personal ties change the tax answer, but the buyer keeps using a non-resident mindset.

- No local execution: Cross-border investors try to manage Greek compliance from abroad without a capable local accountant.

Practical rule: In Greece, the tax answer depends as much on how you hold and operate the asset as on the asset itself.

The upside is that Greek taxation is manageable once you separate the lifecycle into stages: acquisition, holding, renting, and eventual sale. That's the right way to assess a deal, and it's how experienced investors avoid unpleasant surprises.

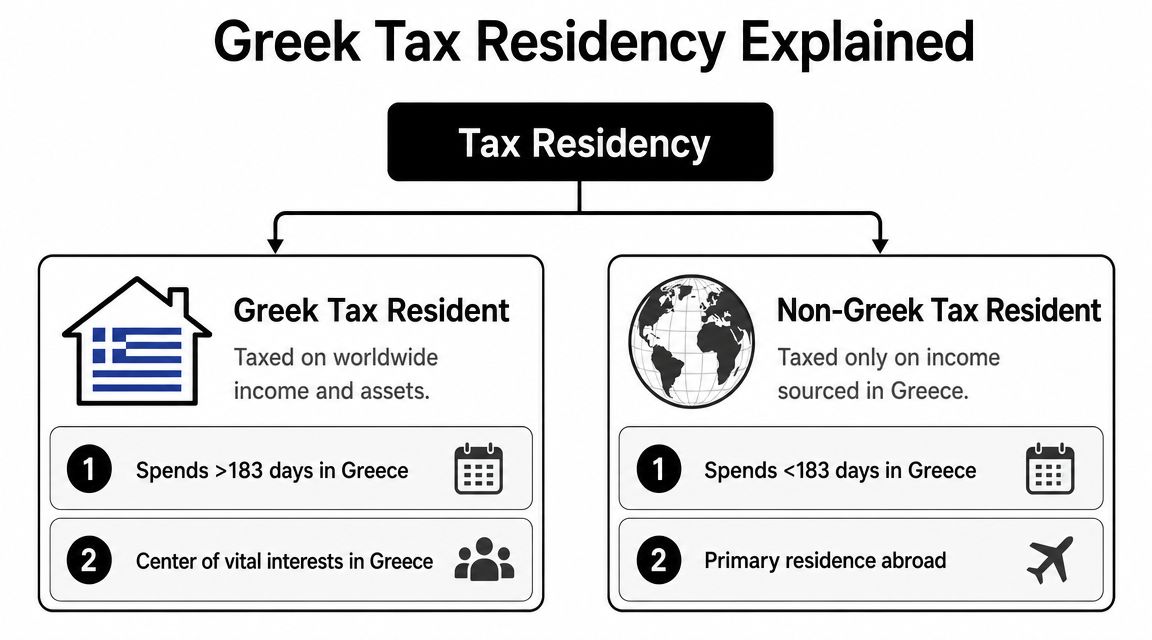

Understanding Your Greek Tax Residency Status

A common investor scenario goes like this. You buy an apartment in Athens as a non-resident, rent it out, then start spending longer periods in Greece each year. Later, a spouse joins you, local banking and day-to-day administration shift to Greece, and the tax position becomes less straightforward than it looked at purchase. At that point, the key issue is no longer just the property. It is whether Greece now treats you as tax resident.

That distinction changes the scope of Greek tax. A non-resident is generally taxed in Greece on Greek-source income. A Greek tax resident is generally taxed on worldwide income. The practical difference is significant for investors with foreign salary, dividends, pensions, or business income.

For income tax rates, use an official source rather than a general expat summary. The Independent Authority for Public Revenue (AADE) guidance on individual income tax is the right starting point for current personal tax treatment and filing obligations.

Resident or non-resident in practice

Day count matters, but it is not the whole analysis. In practice, the Greek position is tested by looking at where you spend your time and where your personal and economic ties are based. Family location, habitual living pattern, business activity, and the centre of your financial life can all matter.

Many investors encounter unexpected difficulties.

The buyer who sees the property as a passive overseas investment can move, gradually and without much planning, into a Greek resident profile. I see this most often with retirees, remote business owners, and families using the property more heavily than originally planned. The tax treatment can change before the investor has updated the holding model, the filing process, or the assumptions used in cash-flow forecasts.

Why this matters to your portfolio

Residency affects more than the annual tax return for the property. It changes how the portfolio should be modelled and monitored.

- Scope of taxation: Non-residents usually deal with Greek-source income. Residents may need to account for income arising outside Greece as well.

- Rate exposure: If you fall within Greek resident treatment, other income streams can affect your overall tax result.

- Compliance load: Resident treatment usually means a wider reporting position, more document gathering, and closer coordination with advisers in more than one country.

- Structure decisions: A holding approach that works well for a non-resident landlord may become inefficient once the investor is resident.

Residence permits and tax residence are also separate questions. Holding a visa, using a holiday home for part of the year, or planning a future move does not by itself settle the tax analysis. If relocation is part of the broader investment plan, this guide on moving abroad from the UK is a useful starting point for the non-tax side of that decision.

Here's a short visual explainer before the practical implications deepen:

The investor mistake to avoid

Do not treat residency as an admin detail to sort out after completion. For cross-border investors, it is one of the main variables that drives net return, reporting cost, and treaty planning.

Review residency before acquisition, then review it again whenever your travel pattern, family position, or business footprint changes.

The practical approach is disciplined. Set your expected status before buying. Stress-test the numbers if Greece later regards you as resident. Then make sure your Greek accountant and your home-country adviser are working from the same facts, because mismatched assumptions are where expensive mistakes usually start.

Taxes on Property Acquisition and Transfer

Buyers often underestimate acquisition costs because they focus on the agreed purchase price. In Greece, that's only one part of the entry cost. The practical question is your all-in cost to acquire legal title and get to first day of ownership.

The Greek system also uses the concept of objective value in parts of the tax framework. That matters because tax calculations don't always track the commercial price in the way foreign buyers expect. Even where the headline deal looks attractive, the tax base and official valuation mechanics can affect total cost.

Your acquisition budget needs a full checklist

A serious acquisition model should include more than tax alone. In practice, buyers should budget for:

- Transfer-related tax exposure: This depends on how the transaction is classified and what tax base applies.

- Notary costs: These are part of closing mechanics, not an optional extra.

- Legal fees: Essential for title review, due diligence, and execution.

- Registry and filing costs: Ownership has to be properly recorded.

- Agent commissions: Commercially obvious, but still missed in early modelling.

This is one reason broad international comparisons can be misleading. In some markets, acquisition costs are more transparent because the tax and fee structure is standardised and widely understood. In Greece, the investor needs to be more careful about document review, valuation assumptions, and the precise tax treatment of the transfer.

Why objective value matters

For property taxes in Greece, the official value framework can influence both one-off and annual costs. That means a deal that looks sensible on market pricing can still carry a heavier tax profile than expected if the objective value sits at a less favourable level.

This issue is familiar to investors who've bought in other Southern European markets. The lesson is the same. Don't underwrite to the listing price alone. Underwrite to the tax base that the authorities may use.

A Greek acquisition should be priced twice. First by the seller. Then by the tax system.

A practical buying discipline

I usually suggest buyers run a pre-close checklist in this order:

- Confirm buyer status: Individual, couple, company, and resident position all matter.

- Confirm transaction classification: Don't assume every purchase is taxed in the same way.

- Review objective value implications: This affects more than one stage of ownership.

- Get written estimates from local professionals: Notary, lawyer, registry, and accounting support need to be costed.

- Stress-test the exit: Some structures feel efficient on purchase but are awkward later.

If you want a frame of reference for transfer-related deal costs in general, a broader property stamp duty calculator guide helps illustrate why transaction taxes should be built into return assumptions from the start.

The investor who keeps acquisition tax simple usually wins. The investor who tries to improvise at closing usually overpays in money, time, or both.

Annual Property Taxes and Rental Income

A purchase can underwrite well on day one and still disappoint by year two. I see this often with Greece. Buyers focus on transfer costs, then discover that the annual holding burden and the tax treatment of rent do most of the work in shaping actual yield.

For property investors, the practical question shifts after completion. The issue is no longer how to acquire the asset. It is how expensive the asset is to hold, whether occupied or vacant, and how rental income will sit inside the owner's wider tax position.

Holding costs start from ownership, not income

Greek property ownership usually brings two recurring local charges into the model. The first is ENFIA, the annual property tax charged by reference to the property's taxable characteristics. The second is the municipal property charge that is commonly collected through the electricity bill. The AADE guidance on property tax administration and the Athens municipality information on municipal fees and taxes are the right places to verify how these charges are assessed and collected in practice.

That has a simple implication. A Greek property creates annual drag even before it produces a euro of rent.

ENFIA is easy to underestimate because it is not linked to cash flow. The bill arrives because the asset is held. The municipal charge is often missed for a different reason. It can look like a utility item rather than an investor cost, so buyers fail to include it in their recurring expense line.

For a non-resident with one apartment, this is mostly a yield discipline issue. For a Greek resident with several properties or wider local income, it becomes part of a broader tax and cash management exercise.

Rental income is where the divergence truly appears

The tax position begins to separate more clearly once the property is let. Greek-source rental income is relevant for both residents and non-residents. The difference is context.

A non-resident is usually dealing with a narrower Greek tax footprint. In many cases, the analysis can stay focused on the Greek property itself, local costs, filing obligations, and treaty relief in the home country if available.

A Greek tax resident has a wider exposure. Rental income does not sit in isolation. It forms part of a broader personal tax profile, which means the marginal cost of extra rent can feel quite different from what a non-resident landlord experiences.

The Greek Ministry of Finance income taxation guide is a useful reference point for the personal tax framework and rate structure.

Greek rental income tax brackets

| Annual Rental Income Bracket | Tax Rate |

|---|---|

| Up to €10,000 | 9% |

| €10,001 to €20,000 | 22% |

| €20,001 to €30,000 | 28% |

| €30,001 to €40,000 | 36% |

| Above €40,000 | 44% |

These figures matter, but the investor mistake is usually elsewhere. It is relying on the average rate instead of testing the marginal effect on the next euro of rent.

Resident versus non-resident through the holding period

The lifecycle view matters. During acquisition, residence status may not be the dominant issue. During the holding and rental phase, it often is.

- Non-resident landlord: usually models Greek rent, ENFIA, municipal charges, filing costs, and any home-country relief position.

- Greek tax resident landlord: needs to test rental income against total taxable income, not just property-level profit.

- Investor running a more active rental model: should check whether the activity remains passive letting or starts to look more like a business for tax purposes.

I do not tell clients that non-resident ownership is automatically preferable. Some are relocating, some are building a long-term base in Greece, and some need a structure that fits family or succession planning. But if the brief is strict portfolio efficiency, resident status can reduce net yield faster than expected once rent is added to other taxable income.

A practical example

Take two investors with similar apartments in the same district and similar gross rent. One remains non-resident and has no other Greek income. The other becomes Greek tax resident and already has taxable earnings in Greece.

Both investors bear ENFIA and the municipal charge. Both need local compliance. The difference appears in how rental income interacts with the rest of the tax profile. The resident investor is more exposed to rate pressure from the wider income base, so post-tax cash flow is often thinner even when the property itself performs similarly.

That is why I prefer to review Greek rentals in two layers. First, the asset. Second, the owner.

What usually works better for long-let investors

For many overseas buyers, ordinary residential letting remains the cleaner route. It is easier to cost, easier to administer, and less likely to drift into a more complicated operating profile.

A sensible underwriting model should include:

- ENFIA and municipal charges as recurring holding costs

- vacancy periods and collection risk

- accounting and filing costs

- the owner's residency position

- realistic assumptions on personal use, if any

Investors who need a broader operating context can review the practical side of renting out residential property in Greece.

One further point. If the property activity involves invoicing or VAT-sensitive services, check registration details carefully. For counterparties and compliance reviews, reliable tax ID checks can help confirm Greek VAT numbers before transactions are booked.

The strongest Greek property returns are rarely the ones with the highest headline gross yield. They are the ones that still work after annual taxes, admin costs, and residency-based tax friction are priced in.

Capital Gains VAT and Other Important Taxes

Selling, developing, or operating a serviced rental introduces a different set of tax triggers. These situations often lead many investors from ordinary landlord issues into more technical territory.

The biggest practical split is between passive property ownership and property activity that starts to look like a taxable supply of services.

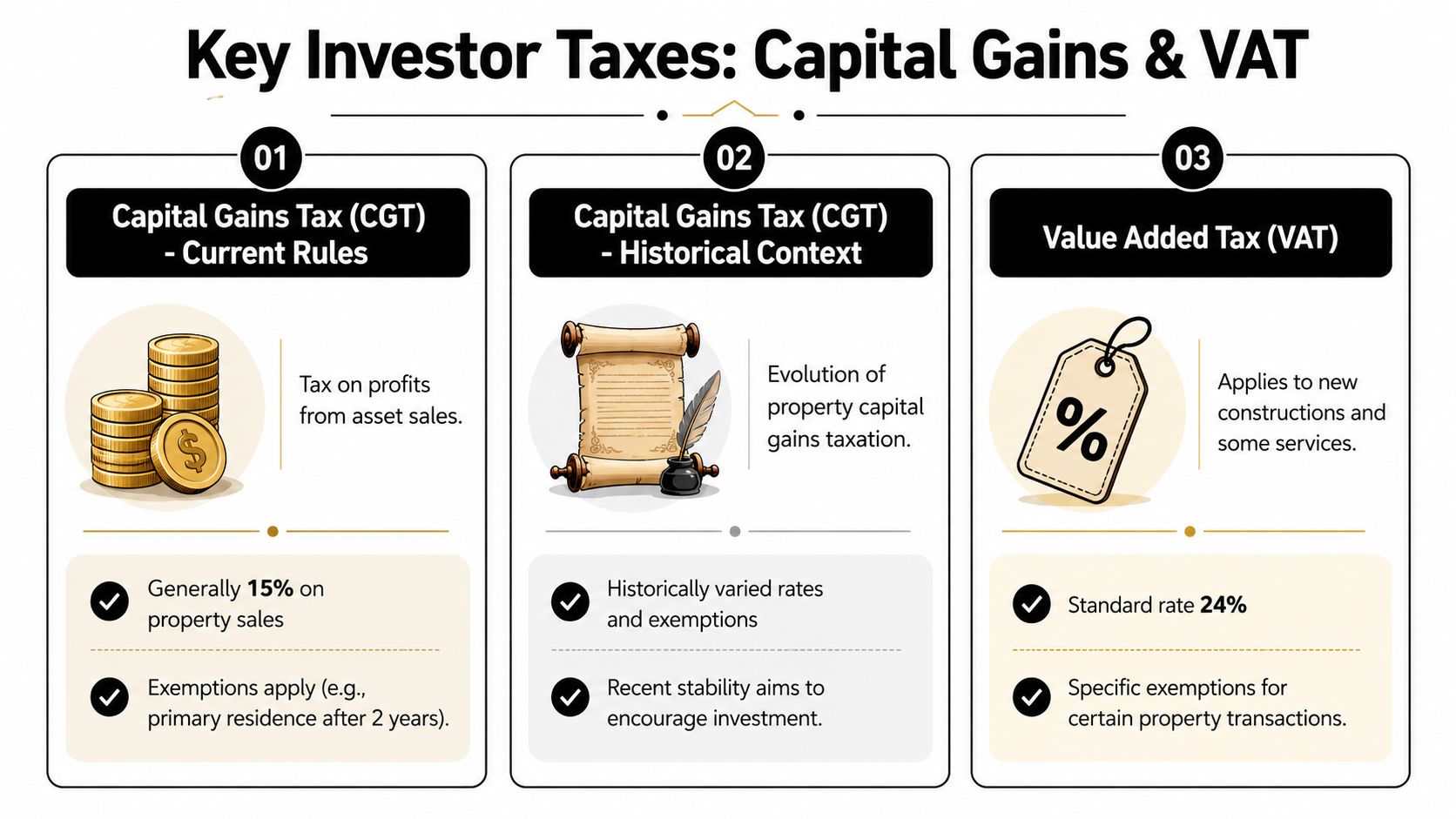

Capital gains and sale planning

Investors regularly ask whether a Greek sale is straightforward from a tax perspective. The honest answer is that sale treatment needs transaction-specific review. You need to consider the seller's status, the holding history, the property type, and whether any special rules or suspensions apply at the time of disposal.

That's why I don't like generic “exit tax” summaries for Greece. They tend to oversimplify a point that is legal, fact-sensitive, and often date-sensitive. Before selling, get the answer fresh. Don't rely on what applied when you bought.

For a broader primer on the mechanics of disposal taxation in property, this guide on capital gains tax on property helps frame the issue.

VAT is the point many investors miss

VAT is often where a Greek property strategy stops being simple. According to Avalara's Greece VAT guide, Greece's standard VAT rate is 24%, with reduced rates of 13% and 6% for specified goods and services. The same source notes that passive long-term lets are exempt, while short-term holiday lets that include services can be treated as a VATable supply.

That distinction changes the economics.

A plain residential lease is one thing. A short-stay operation with cleaning, concierge-style elements, booking support, or other add-ons may fall into a different compliance category. Once VAT enters the model, the investor has to think about registration, invoicing, cash-flow timing, and whether quoted prices are being viewed gross or net of VAT.

Where service wrappers create friction

Three investors can own similar units and face very different tax outcomes:

- The passive landlord signs a standard long-term lease. VAT is generally not the core issue.

- The holiday-let operator offers short stays plus services. VAT risk becomes central.

- The platform-style operator adds digital or concierge elements. Compliance becomes more technical.

If you're dealing with counterparties, service providers, or cross-border platform arrangements, accurate VAT data matters. A practical tool for due diligence is reliable tax ID checks, which can help verify Greek VAT numbers before you rely on invoicing or supplier treatment.

Short-term rental income may look stronger on paper, but once services trigger VAT and added compliance, the margin can narrow quickly.

Other taxes investors shouldn't ignore

Inheritance and gift issues are often neglected because they don't affect year-one cashflow. That's a mistake. Family ownership plans, joint purchases, and succession intentions should be considered before acquisition, not after a death or transfer event.

The practical test is simple. Ask whether the property is meant to be:

- a personal income asset,

- a family legacy asset, or

- inventory in a wider operating business.

The tax treatment won't be identical across those three cases, and the wrong assumption can create avoidable friction later.

Navigating Tax Compliance and Double Taxation Treaties

A well-structured investment can still become messy if compliance is weak. Greece has become less forgiving of casual administration, and foreign buyers should assume that records, filings, and identifiers need to be in order from the outset.

The first operational step is obtaining a Greek Tax Identification Number, commonly referred to as an AFM. Without it, you won't get far with acquisition, ownership administration, or annual filings. In practice, most foreign investors also need a local accountant early, not later.

Why enforcement matters more than many buyers expect

Greece's tax administration sits against a long history of compliance challenges. A Dianeosis study estimated total tax evasion at between 6% and 9% of GDP, or roughly €11 billion to €16 billion annually, according to Dianeosis on tax evasion in Greece. That history helps explain why the authorities have put such weight on tighter reporting and collection.

For investors, the lesson isn't political. It's practical. Assume that documentation quality matters, electronic records matter, and inconsistent reporting will draw attention faster than it once did.

The compliance stack that actually works

The smoothest setups usually include:

- AFM obtained early: Don't leave this until you're about to close.

- Local accountant appointed: Cross-border owners need someone who understands filings, rental treatment, and communication with the authorities.

- Consistent income records: Lease terms, receipts, utility allocation, and service descriptions should all line up.

- Documented home-country advice: Greek tax doesn't replace home-country tax analysis.

Double taxation treaties are the bridge

Most serious investors aren't worried only about Greece. They're worried about being taxed in Greece and again at home on the same income.

That's where double taxation treaties matter. Their purpose is to allocate taxing rights and provide mechanisms such as credits or relief so that the same income isn't taxed twice in full. The exact effect depends on the treaty and your home-country rules, which is why generic internet summaries aren't enough for actual planning.

A useful example for readers with an Australia connection is this note on tax implications for Greek and Australian residents, which shows how treaty analysis becomes practical once residency and income type are clear.

What investors should do each year

I usually tell clients to approach Greek compliance like a recurring asset-management task, not a once-a-year scramble.

- Confirm tax status for the year. Travel patterns and personal ties can change the analysis.

- Reconcile income classification. Passive rent and service income shouldn't be blurred.

- Review treaty position at home. Relief often depends on proper reporting in both places.

- Keep source documents organised. Contracts, invoices, utility bills, and tax payments should be easy to retrieve.

The investors who struggle most in Greece are rarely the ones facing the highest tax rate. They're the ones with inconsistent paperwork, unclear residency facts, and no coordinated advice across jurisdictions.

Strategic Tax Planning for Greek Property Investors

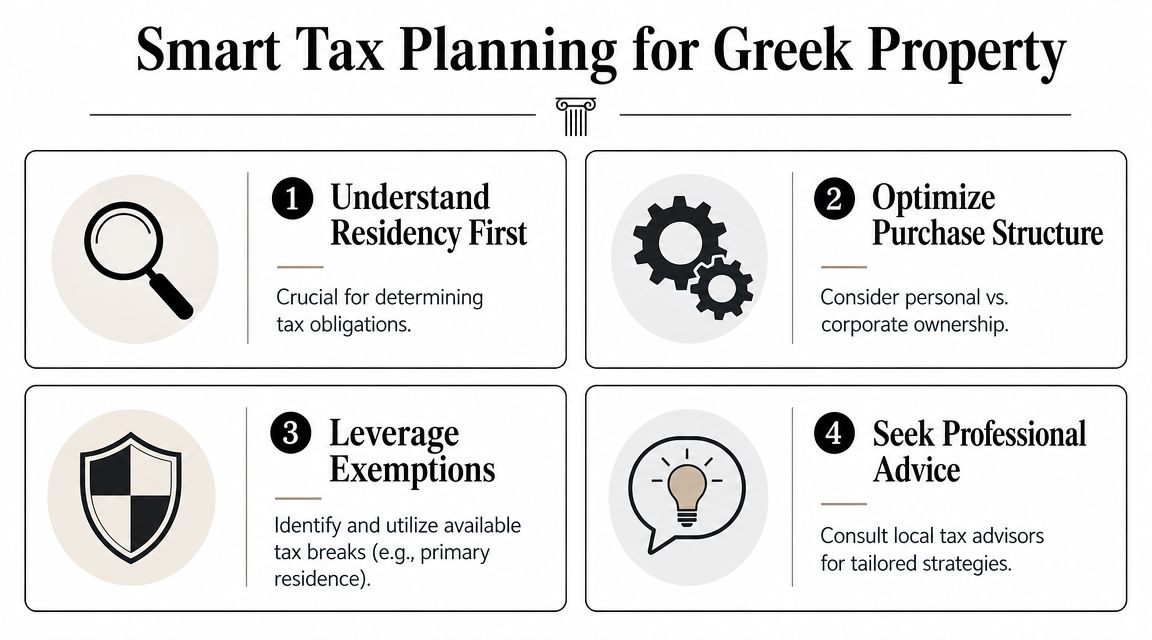

The strongest Greek property plans are built before the purchase, not repaired afterwards. Tax planning here isn't about chasing clever tricks. It's about choosing a structure that matches the asset, your residency position, and the way you'll use the property.

A buyer who wants a long-term residential income asset should usually optimise for simplicity. A buyer who wants serviced accommodation, future relocation, or family succession needs a broader plan from day one.

Start with the ownership question

Most investors begin by asking whether to buy personally or through a company. That's the right question, but the wrong investors often ask it for the wrong reason.

Personal ownership is usually easier to understand and run. Company ownership may help in some cases, especially where the activity is more business-like, but it also adds administration, governance, and potentially a different tax profile. The Greek Ministry of Finance summary referenced earlier notes a 22% standard corporate or business profits rate for the period from 2021 onward, which is relevant when comparing individual and business routes, but a lower company rate on paper doesn't automatically mean a better after-tax outcome once extraction, compliance, and operating realities are considered.

Don't overcomplicate a simple asset

If the property is a plain buy-to-let and you're a non-resident with a narrow Greek tax footprint, complexity often destroys value rather than creating it. Extra entities, nominee arrangements, and improvised service contracts can make a straightforward investment harder to finance, report, and exit.

By contrast, more complex use cases may justify more planning:

- A relocation-driven purchase: Residency needs to be mapped before completion.

- A family holding: Succession and transfer intentions should be reflected in ownership from the start.

- A serviced rental model: VAT and operating classification need upfront analysis.

Incentives and special regimes

Some investors will also review whether any residency, pensioner, or high-net-worth regimes are relevant to their broader move to Greece. Those can be attractive in the right circumstances, but they're personal tax planning questions first and property questions second. Don't buy a property assuming a regime will fit later. Confirm eligibility first.

The best Greek tax strategy is usually the one you can still explain clearly five years later, during a filing review or an exit.

In established markets, investors often accept lower yields in exchange for legal clarity and administrative ease. In emerging or transitioning markets, they demand a premium for complexity. Greece sits somewhere in between. It offers mature legal infrastructure in many respects, but investors still need to price in operational tax friction more carefully than they might in a simpler market.

If you're comparing Greece with other property markets or want practical country-by-country guidance before you buy, World Property Investor publishes detailed research on taxes, yields, buying costs, and investor risks to help you make better international property decisions.