You've found a property that looks strong on paper. The rent seems workable, the location has demand, and the asking price doesn't feel stretched. Then the total acquisition cost lands on your desk and the deal changes shape.

That's where many investors get caught. They focus on the headline purchase price and mortgage terms, but the transaction tax can materially alter cash needed on day one, the return on invested capital, and even whether the deal belongs in the portfolio at all. A stamp duty calculator on property isn't just for getting a tax number. Used properly, it's a decision tool.

For UK purchases, that matters even more because Stamp Duty Land Tax is tiered, affected by buyer status, and sensitive to property use. Add international buyers, additional property surcharges, and cross-border cash planning, and a basic estimate stops being good enough.

The investors who use calculators well don't treat them as a formality at the end of the process. They use them early, alongside yield, financing, and refurbishment assumptions, to decide whether to proceed, renegotiate, restructure, or walk away.

Practical rule: If stamp duty changes your required cash materially, it's not an admin cost. It's part of the investment thesis.

What Is Stamp Duty and Why Calculators Are Essential

Stamp Duty Land Tax (SDLT) is the tax paid on qualifying property purchases in England and Northern Ireland. What trips people up is that it isn't a flat percentage on the whole price in the current system. It applies across bands, and the result depends on who is buying and what they're buying.

That means a buyer of a main residence, a buy-to-let investor, and a non-UK resident can all face different outcomes on the same property. A spreadsheet can do the maths, but only if the setup is correct. In practice, that's where errors start.

The policy backdrop matters

SDLT has changed repeatedly over time, and investors need to respect that. A major shift came with the additional property surcharge introduced in April 2016, which raised average SDLT bills for investors by 40 to 50% and generated £7.2 billion by March 2023, according to GOV.UK residential property rate guidance.

That same GOV.UK guidance confirms how the surcharge altered the effective rate structure for additional properties. The former 0% band up to £125,000 became 3%, and the 12% band over £1.5 million became 15% for affected buyers. It also confirms that first-time buyer relief exempts 67% of first-time buyer purchases under £300,000.

Those changes tell you something important. SDLT is not static. A calculator is essential because the tax is both rule-based and policy-sensitive.

Why manual assumptions often fail

A reliable stamp duty calculator on property helps with three practical tasks:

- Correct banding: It applies marginal rates properly instead of using one flat rate assumption.

- Buyer classification: It distinguishes between a main residence, an additional property, and a non-resident purchase.

- Deal modelling: It lets you move from tax estimate to cash requirement, then into yield and return analysis.

Many investors only calculate SDLT after agreeing a price. That's late. The smarter approach is to test it at shortlist stage, then run it again before exchange if your structure, residency status, or use case changes.

For investors who also model rental performance, a tax number becomes more useful when placed next to income assumptions. A separate rental yield calculator for property analysis helps show whether the deal still works once SDLT is included in total capital outlay.

A good calculator doesn't replace judgement. It gives your judgement the right starting numbers.

What works and what doesn't

A few habits consistently help.

- Use official assumptions first: Start with the rules as they stand, not with what a broker, agent, or forum comment says.

- Check buyer status carefully: Investors often misclassify themselves when they already own property elsewhere.

- Treat reliefs cautiously: Relief can help, but it should be verified before you build it into your offer price.

What doesn't work is relying on a generic portal tool without checking whether it includes additional property treatment and residency effects. That's how buyers end up underfunded on completion or overconfident on projected returns.

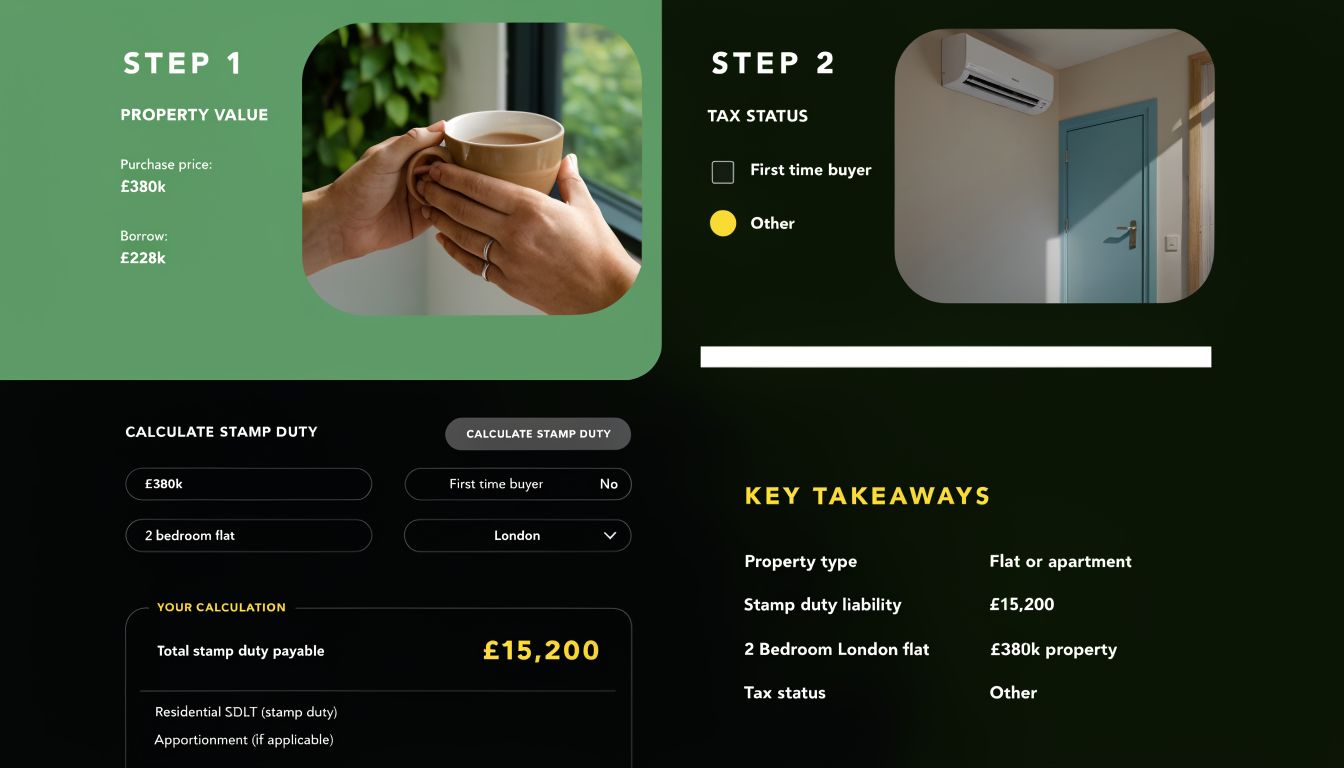

Using a Stamp Duty Calculator A Step-By-Step Example

A calculator is only as good as the inputs. If you enter the wrong property type or buyer status, the number will look precise and still be wrong.

Start with a straightforward investment case. A £600,000 buy-to-let property in England for a UK resident investor. This is a clean example because it shows how the marginal bands work once the additional property surcharge applies.

The right input sequence

When using a stamp duty calculator on property, I'd keep the process in this order:

Enter the purchase price

Use the agreed or target acquisition price. In this example, that's £600,000.Select the property as an additional property

This is the key step for buy-to-let and second home purchases. If you miss it, the output is unusable.Confirm jurisdiction

SDLT applies in England and Northern Ireland. Don't mix systems across the UK.Check residency status

A UK resident investor and a non-UK resident investor can face different outcomes.Review relief fields carefully

If the calculator includes relief options, don't tick them unless they clearly apply and can be evidenced.

For investors comparing tools, a dedicated buy-to-let SDLT calculator is usually more useful than a generic homebuyer version because it frames the transaction correctly from the start.

The worked calculation

For this example, the applicable method is set out by HomeOwners Alliance stamp duty guidance. With the 5% surcharge effective from 31 October 2024, the SDLT is calculated as follows:

- £0 to £250,000 at 5% = £12,500

- £250,001 to £600,000 at 10% = £35,000

That produces a total SDLT bill of £47,500.

If the buyer is a non-UK resident, there is an additional 2% surcharge on top. That's exactly the kind of input many buyers overlook when they use a basic tool.

The same HomeOwners Alliance guidance notes that 68% of first-time buy-to-let investors miscalculate this, which is why calculator choice and input discipline matter.

How to read the result properly

Once the calculator returns £47,500, don't stop there. Ask three follow-up questions.

Is the result based on the correct ownership profile?

If the property is being bought through a different structure, revisit the assumptions.Does the number fit your liquidity plan?

SDLT is cash out on acquisition. It affects deposit planning and reserves immediately.Have you tested the non-resident scenario if relevant?

Cross-border buyers often analyse in one currency and complete in another. That creates a second layer of cost pressure.

Use the calculator twice. First to screen the deal. Then again before commitment, using final facts rather than provisional assumptions.

Common user errors

The recurring mistakes are simple, but expensive:

- Choosing main residence instead of additional property

- Ignoring residency status

- Assuming one flat percentage on the full price

- Forgetting that tax paid on completion still reduces effective starting yield

None of those errors come from difficult mathematics. They come from incomplete setup.

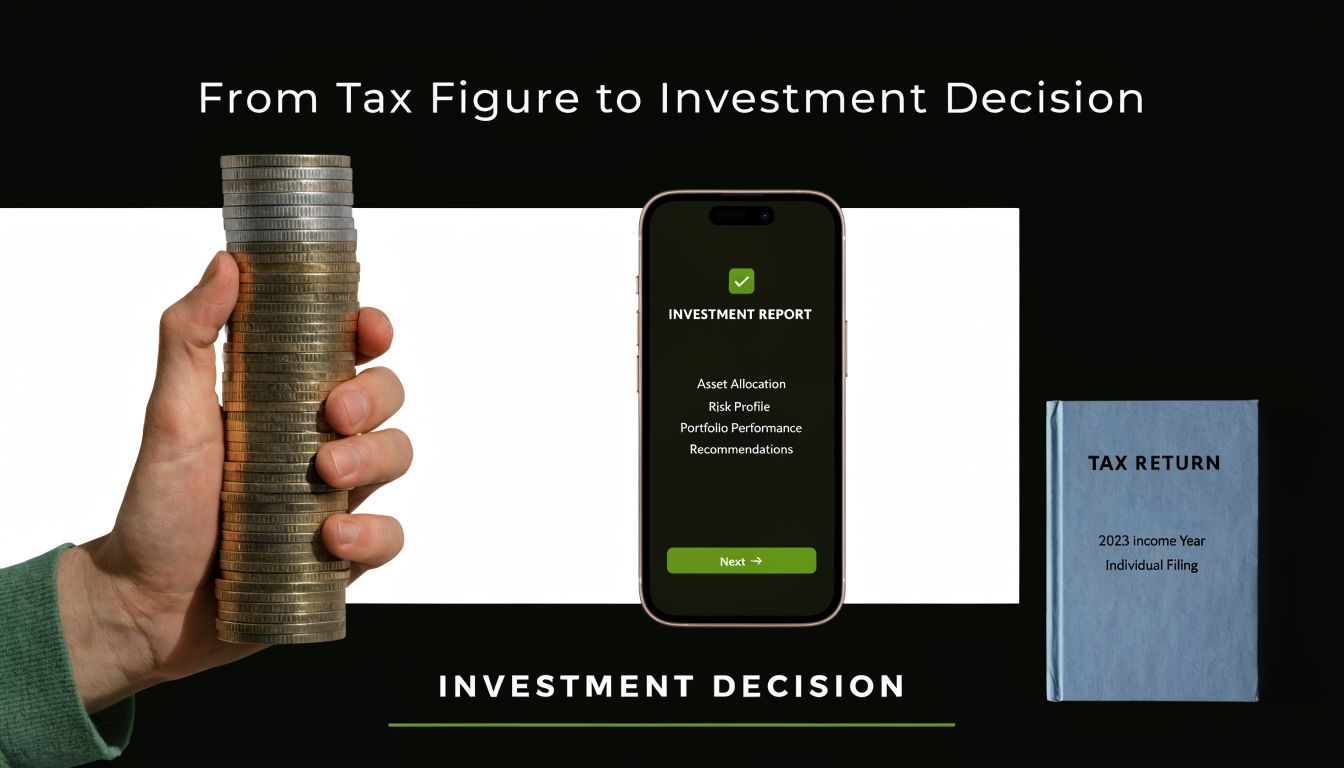

From Tax Figure to Investment Decision

The SDLT output becomes useful when you stop seeing it as a tax figure and start treating it as part of capital deployed. For investment analysis, that's the right lens.

If the tax on a £600,000 buy-to-let is £47,500, your entry cost is no longer just the purchase price. Your acquisition budget has moved materially before legal fees, finance costs, furnishing, or any refurbishment. That changes the return profile from day one.

Fold SDLT into total cost, not overhead

Many investors mentally place stamp duty in an admin bucket. That's a mistake. The tax is part of the capital you must commit to control the asset, so it belongs in the denominator of your return calculation.

A practical review usually starts with:

- Purchase price

- Stamp duty

- Legal and financing costs

- Any immediate works needed to reach lettable standard

- Cash reserves for early voids or operating friction

Once those are assembled, you can calculate whether projected rent still produces an acceptable return on actual capital employed. A focused guide on how to calculate return on investment for property is useful here because ROI becomes distorted quickly when buyers exclude upfront tax.

The decision impact is strategic

The output of a stamp duty calculator on property helps answer better questions than “How much tax will I pay?”

Ask these instead:

| Decision question | Why it matters |

|---|---|

| Does the tax push total cash required above my limit? | Liquidity strain can kill an otherwise good deal |

| Does the asset still meet my return hurdle after SDLT? | Headline yield can look acceptable while cash-on-cash return weakens |

| Should I renegotiate on price? | A thin deal often gets thinner once acquisition costs are fully loaded |

| Is this the right asset class for the tax treatment? | Short-term, mixed-use, and commercial-adjacent assets need closer review |

That's where good investors separate tax calculation from tax strategy. The calculation gives the number. The strategy decides whether the deal structure, asset type, and holding plan still make sense.

For buyers reviewing broader acquisition structuring, especially where asset classification affects treatment, it's worth understanding how experienced operators think about commercial real estate tax strategies. The principles are not identical to residential SDLT, but the mindset is relevant. Tax should be modelled as part of investment design, not patched in after the offer is accepted.

Investment lens: If the tax bill changes your acceptable offer price, the calculator belongs at the start of underwriting, not at the end of conveyancing.

What works in practice

In established markets, where pricing is tighter and yields are often compressed, transaction costs can make mediocre deals look worse very quickly. In emerging or higher-yield locations, investors sometimes tolerate higher friction if net income remains strong, but they still need a disciplined entry-cost model.

The key is consistency. Run the same acquisition-cost framework across every candidate property. That makes comparisons cleaner and prevents one market from looking better because costs were modelled more loosely.

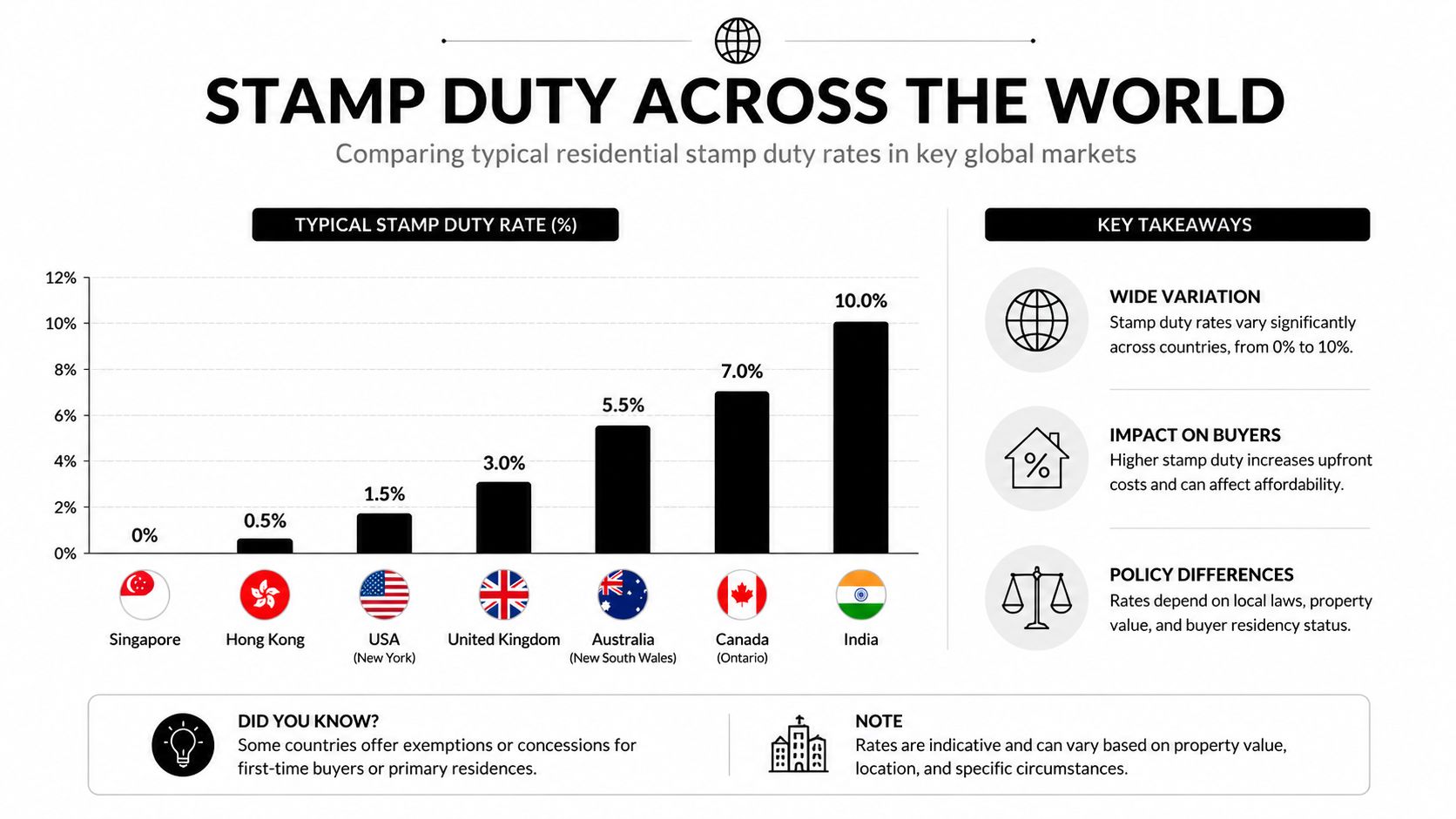

How Stamp Duty Compares in Key Global Markets

International investors rarely assess the UK in isolation. They compare it with Spain, Portugal, France, Dubai, and other markets where entry costs, income profiles, and ownership rules differ. That's exactly why a UK stamp duty calculator on property should sit inside a broader acquisition-cost framework rather than stand alone.

The UK's system is notable for its layered structure. Buyer status and intended use matter. In some other markets, the acquisition tax is simpler to estimate at first glance, but the wider transaction package may still be complex once local fees, notary costs, or municipal charges are included.

A comparison framework that investors can actually use

When comparing markets, I'd focus on four variables:

- Tax structure: Is it banded, flat, or dependent on buyer profile?

- Foreign buyer treatment: Are overseas investors taxed differently?

- Asset classification risk: Do residential, mixed-use, and commercial uses change the result?

- Transaction friction: How much cash is tied up before the asset produces income?

That framework is more useful than chasing one headline tax rate.

Property Transaction Tax Comparison for International Investors 2026

| Country | Tax Name | Indicative Rate | Key Considerations |

|---|---|---|---|

| UK | Stamp Duty Land Tax | Banded and status-dependent | Additional property and non-resident treatment can materially change entry cost |

| Spain | ITP | Varies by region and property profile | Regional rules matter, so investors need local verification before underwriting |

| Portugal | IMT | Tiered by property value and use | Residence status and use can affect the practical cost calculation |

| Dubai | DLD Fee | Usually presented as a transfer fee model | Simpler to model upfront, but investors still need to account for total buying costs |

| France | Droits de Mutation | Typically part of a broader acquisition-cost package | Notary and related purchase costs often shape the real entry-cost picture more than buyers first expect |

The purpose of this table isn't to reduce every country to one number. It's to remind investors that tax comparison only works when you compare like with like.

Established markets versus emerging opportunities

In established markets, tax friction often matters more because yields may be tighter and the margin for underwriting error is smaller. If entry costs are high, the property needs stronger durability. That usually means better location quality, deeper tenant demand, and less operational uncertainty.

In emerging markets or faster-moving secondary cities, investors may accept more risk because income can compensate for acquisition drag. But that only works if legal structure, local compliance, and exit routes are clear. A lower transaction tax doesn't rescue a poor asset or a weak market.

Don't compare countries by tax alone. Compare what the full acquisition cost buys you in terms of income resilience, financing options, and exit flexibility.

Why localisation beats generic calculators

A generic global tool won't capture market-specific rules properly. That's why serious investors localise the model. They use one method for comparing total entry cost across countries, but they use local calculators and local legal guidance to populate each market.

France is a good example of why local tax understanding matters. Rules, fees, and acquisition structure need to be reviewed in-country rather than estimated from a generic international template. For investors weighing Europe side by side, a market-specific guide to property taxes in France helps keep comparisons grounded.

The practical takeaway is simple. Use the UK calculator to understand the UK accurately, then compare that result against equally localised assumptions in other markets. Anything less creates false precision.

Common Exemptions and Costly Mistakes to Avoid

Reliefs matter, but overconfidence is more expensive than missed optimisation. Buyers often hear that exemptions exist and then start underwriting as if relief is guaranteed. That's backwards.

The safe approach is to treat reliefs as provisional until your solicitor or tax adviser confirms they apply to your exact transaction. Some calculators allow relief settings, but the output is only useful if the legal basis is solid.

Reliefs worth checking carefully

There are legitimate situations where tax treatment improves, but they need case-by-case review.

- First-time buyer relief: This can materially change the number for qualifying owner-occupiers, but it doesn't transfer neatly into investment use cases.

- Multiple dwelling scenarios: Buyers acquiring more than one unit in a single transaction should check whether any relief or alternative treatment applies.

- Classification questions: Mixed-use or commercial treatment can produce a very different result from standard residential assumptions.

For company buyers assessing structure early, a more specific stamp duty calculator for limited companies can help frame the right questions before formal advice is taken.

The international investor trap

Cross-border buyers routinely underestimate acquisition cost because many basic calculators miss the full effect of buyer profile and currency exposure. According to HMRC tax and NIC receipts data, international investors often underestimate total UK acquisition costs by 10 to 15%.

That's not a minor variance. On a £500,000 flat, a basic tool might show £15,000, while an overseas investor with an existing property could face £29,500 once the relevant surcharges are included. The same HMRC-based data notes that this gap can erode projected net returns by 2 to 3% annually in high-yield markets like Manchester.

The stamp duty calculator on property is strategic. International investors shouldn't just ask, “What is my SDLT?” They should ask, “What is my all-in acquisition cost in both sterling and home currency, and how does that affect my expected return?”

A tax estimate that ignores buyer status and currency reality is not conservative. It's incomplete.

The short-term let classification problem

Another area where buyers make expensive mistakes is short-term rental property. Post-2025, treatment around holiday lets and property classification has become more sensitive, and investors who use broad residential assumptions can get caught out.

The HMRC-based data provided for this topic notes a 15% audit uptick on misclassified holiday lets. That should be enough to slow any investor down before relying on a simple portal estimate.

A few warning signs deserve attention:

- Residential by default: Many online tools assume standard residential treatment even when the asset has mixed-use or commercial-style characteristics.

- Operational model mismatch: A property intended for short-term letting may not fit the tax assumptions of a conventional buy-to-let.

- False savings expectations: Investors sometimes assume a more favourable classification without verifying the actual criteria.

The practical answer is discipline. Use calculators for screening, then verify classification and buyer status before commitment. If the asset sits near a rule boundary, don't rely on the tool alone.

The best investors don't avoid calculators. They use them properly, then challenge the result before capital is committed.

World Property Investor helps international buyers compare markets, analyse rental yields, understand taxes, and assess real acquisition costs before they commit capital. If you're researching where to buy next, visit World Property Investor for market guides, investment analysis, and practical tools built for cross-border property decisions.