The UK average house price reached £268,000 in April 2025, up 3.4% year on year, with England at £290,000, Wales £210,000, Scotland £191,000, and Northern Ireland £185,000, according to the housing figures cited in this market reference. That matters because it changes the starting point for many investors. For a growing share of UK buyers, the international real estate market is no longer a niche search for a holiday flat. It's a practical response to domestic pricing, portfolio concentration, and the need to compare income, growth, and risk across borders.

Buying abroad can improve diversification. It can also create new forms of exposure that many investors underestimate, especially legal complexity, tax friction, financing constraints, and currency translation. A property that looks attractive in local terms can deliver a much weaker result once income is converted back into sterling, taxes are paid, and resale liquidity is tested.

Serious international investing starts with a different question. Not “Which country is hot?” but “What is this property supposed to do for my portfolio?” Income, capital appreciation, diversification, personal use, and residency planning all lead to different market choices. Investors who ignore that usually end up comparing unlike assets and taking avoidable risk.

An Introduction to the Global Property Market

The international real estate market is best understood as a set of local markets connected by global capital, migration, tourism, regulation, and financing conditions. That's why broad headlines rarely tell you enough. A city can benefit from strong tenant demand while the wider country struggles. Another market can look cheap on price alone but remain difficult to exit because foreign buyer demand is thin or financing is restrictive.

For UK-based investors, the case for looking abroad is increasingly grounded in portfolio construction rather than speculation. When the domestic market is already expensive, overseas property can offer access to different tenant bases, different economic cycles, and a wider range of property strategies. Some investors want stable long-term lettings in mature cities. Others want exposure to tourism-driven assets, student housing, logistics, or second-home markets.

Why investor goals matter first

An investor seeking cash flow will assess a market differently from one seeking capital appreciation. Income-focused buyers care about tenant demand, occupancy resilience, operating costs, and the reliability of rent collection. Growth-focused buyers care more about supply constraints, infrastructure quality, population trends, and whether the city can attract long-term demand from employers and residents.

A third group wants diversification. For them, the right overseas property may not be the one with the highest apparent yield. It may be the one that behaves differently from assets already held in the UK.

Practical rule: Don't compare countries before you've defined the role the property will play in your portfolio.

What separates disciplined buyers from casual buyers

Experienced investors rarely start with listings. They start with filters:

- Target outcome: Income, growth, diversification, lifestyle use, or a blend.

- Asset type: Residential, commercial, hospitality, land, or specialised real estate.

- Risk tolerance: Legal complexity, political uncertainty, financing exposure, and currency sensitivity.

- Exit path: Who is likely to buy the asset from you later, and under what conditions?

The international real estate market rewards investors who treat each purchase as an operating business with local rules, not a generic asset class with interchangeable returns.

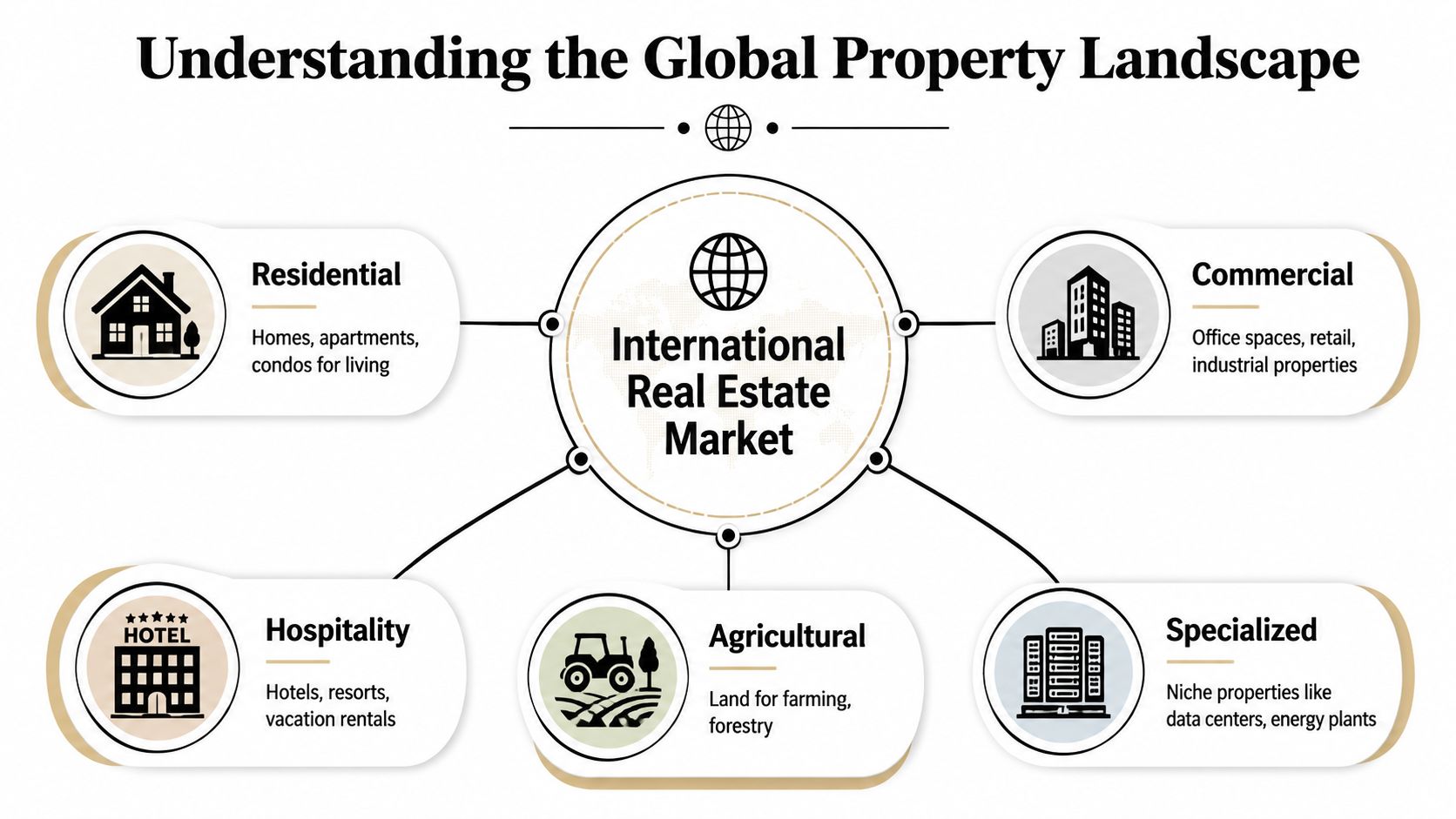

Understanding the Global Property Landscape

The global property market resembles a multi-asset portfolio more than a single market. Residential flats, office buildings, hotels, farmland, and data centres may all sit under the same real estate umbrella, but they respond to different demand drivers. A family renting a city apartment isn't behaving like a logistics operator taking warehouse space, and neither is comparable to a tourist booking a short-stay unit.

The main sectors investors actually choose between

Residential property is usually the starting point for individual investors. It tends to be easier to understand because demand is linked to household formation, affordability, transport links, and local employment. The key question isn't just whether people want to live there. It's whether the rent level is sustainable relative to local incomes and whether supply can expand quickly.

Commercial property includes offices, retail, and industrial space. These assets depend more heavily on business activity, lease structures, and tenant covenant quality. They can offer stronger contractual income visibility, but they also require a deeper understanding of vacancy risk, fit-out costs, and local leasing norms.

Hospitality assets such as hotels, serviced apartments, and holiday rentals can produce strong income in the right market, but they're more operationally intensive. Revenue depends on travel demand, regulation, seasonality, and management execution.

The less obvious categories

Alternative and specialised property deserves more attention than it often gets. Data centres, student accommodation, healthcare property, energy-linked sites, and agricultural land all serve specific forms of demand. These sectors can behave differently from mainstream housing cycles, which can help diversification.

For investors comparing countries and structures, practical operational support matters too. Platforms and workflows built for cross-border teams, such as international real estate solutions, can help standardise lead management, documentation, and communication when multiple jurisdictions are involved.

A good international property strategy often starts by narrowing the asset type, not the country.

Matching sectors to investor objectives

A simple way to think about the international real estate market is by function:

- For steady occupancy: Standard residential property in liquid urban markets.

- For business-linked income: Commercial assets where lease quality is strong.

- For tourism exposure: Hospitality in markets with resilient visitor demand.

- For niche diversification: Specialised sectors with structural rather than cyclical demand.

- For land-based value: Agricultural assets where the investment thesis is distinct from urban housing.

The mistake many first-time buyers make is treating every overseas asset like a residential buy-to-let. That misses both risk and opportunity.

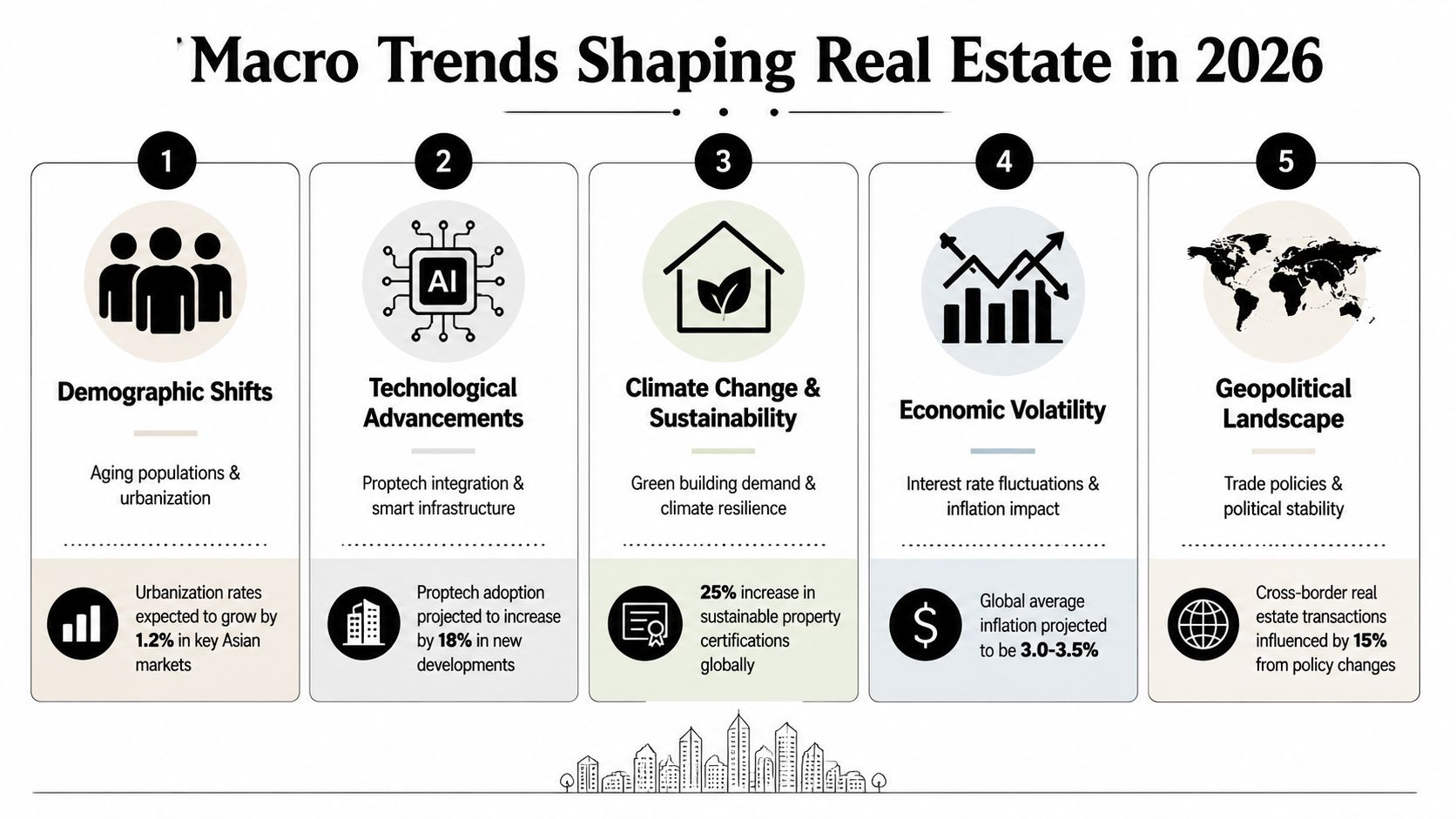

Macro Trends Shaping Real Estate in 2026

Property values don't move in isolation. They sit at the intersection of work patterns, financing conditions, demographics, regulation, and physical resilience. In 2026, the most important trends aren't just affecting prices. They're changing what counts as a “good” asset.

A useful background read on broader context is this review of global real estate market value, but the investment implications only become clear when trends are translated into asset selection.

Work patterns and the location reset

Remote and hybrid work have changed demand in uneven ways. Prime city centres haven't disappeared, but investors now need more precision. In residential markets, people still pay for access to jobs, transport, schools, and services. Yet some demand has shifted toward locations that offer more space, better liveability, or lower total housing cost.

In commercial markets, weak offices and strong offices are no longer the same category. Buildings with outdated layouts, poor energy performance, or weak transport access face different leasing risk from well-specified assets in proven business districts.

So what for investors? Don't buy “city centre” or “suburban” as a theme. Buy specific micro-locations that fit how occupiers now use space.

Financing conditions and the affordability test

Interest rate conditions continue to affect borrower affordability, lender appetite, and exit demand. Even when a property's rental profile looks solid, financing can make the investment unattractive if debt costs compress cash flow or limit refinance options.

This matters most in markets where foreign buyers depend on local borrowing or where domestic buyers set resale prices. A market can look appealing at entry, then feel less attractive when the eventual buyer base faces tighter mortgage conditions.

Investor lens: Underwrite the asset on what it can support through a full financing cycle, not only under today's borrowing terms.

Demographics and durable demand

Demographic change is slower than sentiment, but far more powerful. Ageing populations often support healthcare, assisted living, and downsizer housing. Younger populations can support rental demand, student housing, and entry-level ownership markets if jobs and incomes are expanding alongside population growth.

The important distinction is this: population growth alone isn't enough. Investors should ask whether the relevant population segment can afford the asset type being developed.

Sustainability and physical risk

Sustainability is no longer a branding feature. It affects running costs, tenant appeal, compliance risk, and obsolescence. In some markets, inefficient buildings face steeper refurbishment needs, weaker tenant demand, or poorer financing terms. Climate exposure matters too. Flood risk, heat stress, water availability, and insurance conditions can all change the economics of ownership.

A property investor doesn't need to become an environmental specialist. But every acquisition should include practical questions:

- Building efficiency: What will it cost to keep the asset lettable and compliant?

- Insurance resilience: Is cover straightforward, restricted, or expensive?

- Operational durability: Can the asset perform in harsher weather conditions?

- Exit quality: Will future buyers see this as modern stock or stranded stock?

Markets still matter. Yet within most markets, asset quality now matters more.

Analysing Market Types Established vs Emerging

Cross-border property returns can diverge sharply from headline market performance once currency moves are included. For UK-based investors, that changes the established versus emerging question from a simple risk trade-off into a portfolio design decision.

A more useful framework starts with objective. Investors buying for cash flow usually benefit from markets with clearer rent histories, deeper tenant demand, and lower operating uncertainty. Investors seeking capital appreciation can accept more pricing volatility if there is a credible path to income growth, infrastructure improvement, or institutional re-rating. Investors focused on diversification should ask a different question again: whether the market is driven by economic forces that differ from the UK, and whether the currency exposure improves or weakens that benefit.

Established markets typically offer better transparency, stronger financing channels, and more reliable exit liquidity. That matters because a good investment is not just an asset you can buy at the right price. It is also one you can refinance, manage, and sell without relying on ideal conditions.

Emerging markets can produce stronger upside, but only where the growth story is matched by execution capacity. A city can attract foreign interest, tourism, or new infrastructure and still disappoint investors if planning rules shift quickly, title checks are inconsistent, or local wage growth fails to support rents. For investors screening higher-growth regions, this review of emerging property markets is most useful when treated as a starting point for local due diligence, not a shortlist of automatic winners.

How to assess Berlin and Lisbon

Berlin illustrates why many investors accept lower headline yield in an established market. The city benefits from scale, a large employment base, and broad investor coverage. Those features usually mean fewer pricing anomalies, but they also reduce the odds of overpaying based on optimistic sales narratives. In practical terms, underwriting is easier because comparable evidence tends to be stronger and the buyer pool at exit is usually wider.

Lisbon fits a different profile. International demand, urban renewal, and lifestyle-driven buying have all supported interest in the city. That can create faster repricing than in a mature market, but it also makes returns more sensitive to political decisions, tax treatment, and shifts in foreign buyer demand. A UK investor also has to account for euro exposure. A property that performs well in local terms can still produce weaker sterling returns if exchange rates move unfavourably over the holding period.

That currency point is often underestimated. In an established eurozone market, exchange-rate risk may be acceptable if the goal is diversification away from sterling assets. In a faster-moving market, currency volatility can either amplify gains or erase part of the market's underlying performance. The right choice depends less on whether a market is labelled established or emerging, and more on whether its return drivers match the investor's base currency and time horizon.

Market profile comparison

| Metric | Established Market (e.g. Berlin, Germany) | Emerging Market (e.g. Lisbon, Portugal) |

|---|---|---|

| Pricing efficiency | Usually higher, with clearer comparables and tighter bid-ask spreads | More uneven, with district-level pricing gaps and greater scope for mispricing |

| Liquidity | Typically deeper across buyer types and financing sources | More dependent on sentiment, overseas demand, or a narrower buyer base |

| Income profile | Easier to underwrite using longer rent histories and standard leasing evidence | Can appear stronger initially, but income may be less stable through policy or demand shifts |

| Capital growth potential | More often linked to steady income growth and supply constraints | More often linked to re-rating, infrastructure change, or rising international visibility |

| Currency effect for UK investors | Often easier to model where volatility is lower and holding periods are longer | Can have an outsized effect on realised sterling returns |

| Legal and regulatory clarity | Usually more predictable for first-time overseas buyers | Often requires stronger local legal and tax advice |

| Best fit | Cash flow, lower-friction ownership, and core portfolio holdings | Capital growth, selective diversification, and investors able to handle more local complexity |

Which type of market suits which goal

Established markets tend to suit investors who want:

- Cash flow that is easier to forecast: Better rent evidence, clearer operating costs, and more stable resale conditions.

- Lower execution risk: Fewer surprises in financing, management, and disposal.

- Core portfolio exposure: Assets that anchor an international allocation rather than drive all of its growth.

Emerging markets tend to suit investors who want:

- Capital appreciation with a clear catalyst: Infrastructure delivery, business relocation, urban regeneration, or rising institutional interest.

- Diversification from UK pricing cycles: Exposure to demand drivers that do not closely track the domestic market.

- Selective higher-return opportunities: Provided currency risk, legal process, and exit depth have been tested in advance.

The strongest international portfolios often use both. Established markets can provide stability and financing flexibility. Emerging markets can add growth. The mistake is treating either category as automatically superior, instead of matching market type to the return objective that matters most.

Essential Metrics for International Investors

Numbers don't eliminate risk, but they do stop investors from relying on sales language. In the international real estate market, a small group of metrics can turn a broad market search into a disciplined screening process.

Gross and net rental yield

Gross rental yield is the simplest measure.

Formula: Annual rent ÷ purchase price × 100

It tells you how much income the property generates before costs. That makes it useful for quickly comparing markets, but weak for final decisions. Gross yield ignores letting fees, maintenance, insurance, taxes, service charges, vacancy, and local compliance costs.

Net rental yield adjusts for those costs.

Formula: Annual rent minus annual operating costs, divided by total acquisition cost × 100

Net yield is closer to economic reality. In cross-border investing, it's usually the more useful figure because operating expenses vary widely by country and building type.

Cap rate and price-to-rent ratio

Capitalisation rate, or cap rate, is closely related to net yield but is usually discussed in relation to the property's operating income and current market value rather than the investor's purchase costs. This guide to the rate of capitalisation is a helpful reference if you want to compare how income-producing property is commonly assessed across markets.

Formula: Net operating income ÷ property value × 100

Cap rate is especially useful when comparing income assets in different cities because it focuses on what the asset itself produces.

The price-to-rent ratio works differently.

Formula: Property price ÷ annual rent

A high ratio can indicate that pricing has run ahead of income. That doesn't always mean the market is unattractive. Prime locations often trade on scarcity and expected capital preservation. But it should make you ask whether you're paying for future appreciation that may or may not arrive.

Why metrics must be read together

A property can show a strong gross yield and still be weak once costs are included. Another can have a modest yield but sit in a highly liquid market with stronger long-term pricing support. No single metric can answer every investment question.

Use the metrics as a sequence:

- Screen with gross yield to eliminate obviously weak income deals.

- Refine with net yield and cap rate to understand true operating performance.

- Sense-check with price-to-rent ratio to see whether capital values are stretched.

- Overlay market factors such as legal ease, financing, tenant demand, and exit liquidity.

This video gives a useful visual introduction to assessing property performance:

If an agent only gives you gross figures, you're looking at marketing. If you can rebuild the net numbers yourself, you're doing analysis.

Navigating Foreign Ownership Rules Risks and Taxes

A sound property can become a poor investment if the ownership structure is weak, the tax treatment is misunderstood, or the currency moves against you. These risks don't sit on the edge of the investment case. They sit at the centre of it.

Legal risk starts with title and ownership rights

Foreign ownership rules vary widely. Some countries permit straightforward freehold ownership. Others limit foreigners to leasehold structures, require local approvals, restrict land categories, or apply different rules by region. The critical question isn't whether foreigners can buy. It's what exactly they are buying, and how enforceable those rights remain over time.

A buyer should verify:

- Title quality: Is ownership clean, registered, and transferable?

- Use restrictions: Can the asset legally be rented, renovated, or redeveloped?

- Entity rules: Is personal ownership allowed, or is a company structure common?

- Approval risk: Does the purchase depend on government or municipal consent?

These issues often matter more than the headline location.

Tax risk is rarely confined to purchase day

Most overseas investors think first about transfer taxes or stamp duty equivalents. That's only one layer. You may also face annual property taxes, rental income tax, withholding arrangements, reporting obligations in your home country, and capital gains tax at sale.

If you're modelling an eventual disposal, this overview of capital gains tax on foreign property is a useful starting point. The key discipline is to model the entire holding period, not just the purchase cost.

Key judgement: A property isn't “high yielding” if taxes and compliance costs absorb the margin after conversion into your home currency.

Currency risk is not a side issue for UK investors

For UK-based investors, one of the least appreciated risks in the international real estate market is sterling translation. Aberdeen's UK-focused investor research notes that currency risk and sterling translation effects can shape realised returns as much as local rent or capital growth, because a UK buyer's result is exposed both to the local market cycle abroad and to the pound's effect on repatriated income and sale proceeds, as discussed in Aberdeen's global real estate market outlook Q2 2025.

That creates a double layer of exposure. The property may perform well in local terms while the sterling value of those gains weakens on conversion. The reverse can also happen, but investors shouldn't treat favourable currency moves as part of the core thesis.

A practical way to group and manage risk

Legal risks are best managed through local counsel, document review, title verification, and a conservative reading of what the ownership structure grants.

Financial risks include tax leakage, financing mismatch, and foreign exchange exposure. Investors can reduce them by matching debt and income currency where appropriate, stress-testing costs, and planning repatriation rather than treating it as an afterthought.

Political and regulatory risks are harder to predict but easier to identify than many buyers assume. If a market has become heavily dependent on foreign capital, ask how popular that trend is domestically. Policy can change faster than property can be sold.

The disciplined buyer doesn't try to eliminate uncertainty. They price it correctly before completion.

Your Due Diligence Checklist for Buying Abroad

Cross-border property investing gets safer when the process is orderly. Most mistakes happen when buyers skip ahead from market interest to reservation deposit without testing the asset, the structure, and the exit.

A disciplined sequence that works

Research the market first. Check the city economy, local demand drivers, rental depth, and likely resale audience before looking at individual units.

Build the local team early. Use an independent lawyer, tax adviser, and broker or agent with direct experience of foreign buyers. If your purchase may involve a corporate holding structure, jurisdiction-specific reading such as this UAE offshore company formation guide can help you frame the right questions before taking formal advice.

Test the numbers yourself. Rebuild yield, operating costs, taxes, financing, and currency scenarios from scratch.

Inspect or verify properly. Visit in person where possible. If not, use trusted third parties for condition reports, document checks, and neighbourhood verification.

Review legal ownership and exit mechanics. A specialist international real estate lawyer should confirm title, restrictions, contracts, and transferability.

Define the exit before you buy. Decide whether the most likely buyer later is a local owner-occupier, an investor, another foreign buyer, or a developer.

A property abroad should feel clearer, not murkier, as due diligence progresses. If each answer creates two new uncertainties, step back.

World Property Investor publishes country guides, city comparisons, tax explainers, and strategy-led research for investors comparing property markets across borders. If you want practical, neutral analysis before committing capital, explore World Property Investor.