Property still attracts investors for the same reason it always has. It's tangible, understandable, and capable of producing income while holding long-term value. What's changed is the margin for error.

In 2026, you're not buying into a simple passive-income story. You're buying into financing costs, tax rules, tenant law, compliance, local supply pressure, and the quality of your underwriting. A deal that looks strong on a portal can turn weak once management costs, voids, legal risk, and debt pricing are added properly.

That's why rental investment properties need to be treated as an operating business, not a hobby. The best investors don't ask, “What's the yield?” They ask, “What survives after costs, tax, financing, and friction?”

The Foundations of Global Property Investment

Property remains one of the few asset classes where a private investor can influence the outcome directly. You can improve the asset, alter the tenancy mix, refinance, change the management model, and decide when to exit. That control is valuable, but it also creates responsibility. Weak analysis gets punished quickly.

The rental market is no longer a side segment in major economies. In England, the private rented sector grew from about 2.4 million households in 2008–09 to 4.6 million by 2022–23, and represented around 19% of households by 2022–23, according to this market overview of rental property KPIs. That matters because it confirms rental housing is a structural part of the market, not a temporary trade.

A larger rented sector changes how serious investors should think. You're not just buying bricks and mortar. You're entering a mature income market where vacancy, rent collection, operating costs, and regulation shape returns every month.

Why the old story is too simple

A lot of beginner content still frames buy-to-let as a straightforward path to passive income. That was never fully true, and it's less true now. Mortgage pricing moves. Tax policy changes. Cities introduce licensing rules. Tenant protection expands. Insurance and maintenance costs don't stay still.

Established markets tend to offer stronger legal predictability and deeper liquidity. Emerging markets may offer lower entry prices or higher headline income, but they often bring more operational friction, policy uncertainty, or currency exposure. Neither is automatically better. The right choice depends on what you're trying to optimise.

Practical rule: If a property only works under perfect conditions, it doesn't work.

A disciplined investor starts with market structure, then legal context, then finance, and only then the individual property. That order matters. Good stock in the wrong market still underperforms.

For broader context on country-level opportunities, it's worth reviewing these real estate investment guides for international buyers. The useful question isn't where property sounds exciting. It's where the numbers, rules, and demand line up.

What professional investors focus on first

Before looking at décor, refurbishment ideas, or listing photos, focus on the fundamentals:

- Demand durability: Are tenants likely to remain in the area because of jobs, education, transport, or affordability?

- Legal clarity: Can you understand the tenancy rules, landlord obligations, and enforcement process without guesswork?

- Exit liquidity: If you need to sell, is there a broad buyer pool?

- Financing fit: Does debt financing improve the deal, or merely make it more fragile?

That mindset is what separates investing from speculation.

Understanding Rental Property Types and Strategies

Not all rental investment properties behave the same way. Tenant profile, management load, financing options, and regulatory burden can vary sharply even within the same city. Investors often go wrong by choosing an asset type that doesn't match their capital, time, or tolerance for operational complexity.

The main property types

A standard buy-to-let house or flat is usually the cleanest starting point. It tends to attract singles, couples, small families, or long-term tenants who want stability. Management is often simpler than more intensive models, and financing is usually more straightforward.

A small multi-unit property gives you multiple income streams under one roof. That can reduce the pain of one vacancy, but it also increases maintenance coordination and tenant management. It suits investors who want scale without moving fully into commercial-style operations.

An HMO or co-living property can produce stronger income per square metre when executed well. It also comes with more moving parts. More tenants means more wear, more turnover, and more compliance pressure. In many locations, that model only works if you understand local licensing and can run the property tightly.

A short-term or holiday let is a different business entirely. It depends more on occupancy management, pricing, furnishing, guest communication, and local rules. Gross income can look attractive in peak periods, but the operating model is closer to hospitality than long-term residential letting.

For investors new to the terminology, this guide to the buy-to-let definition and model is a useful baseline.

Matching the asset to the investor

The right property type depends less on fashion and more on fit.

| Property type | Best suited to | Main strength | Main weakness |

|---|---|---|---|

| Standard buy-to-let | Newer investors, long-term holders | Simpler management | Lower income intensity |

| Small multi-unit | Investors seeking spread of income | Multiple rent streams | More operational oversight |

| HMO or co-living | Hands-on operators | Stronger room-by-room income potential | Compliance and management complexity |

| Short-term let | Hospitality-minded investors | Flexible pricing and usage | Volatile occupancy and regulation |

The strategy matters as much as the asset

A buy-and-hold strategy suits investors who want steady occupancy, manageable turnover, and long-term wealth accumulation. It often works best in locations with durable tenant demand and clear resale appeal.

A BRRRR approach means buying a property with problems you can fix, improving it, renting it out, refinancing, and repeating the cycle. This can accelerate portfolio growth, but it requires strong execution. Refurbishment overruns, delayed letting, and weaker-than-expected refinance terms can break the model.

A yield-maximising urban strategy often leans toward co-living or room-based rental structures. That can work well in major employment centres, but only if your management systems are strong and the legal framework supports the format.

Some investors need simplicity more than they need maximum yield. A calm property that lets easily and runs predictably often outperforms a “high-yield” asset that creates constant friction.

What usually works and what usually doesn't

What works:

- Simple stock in proven areas: Easy-to-let homes near transport, jobs, and everyday amenities.

- Clear tenant targeting: Properties designed around a specific renter profile.

- Conservative strategy choice: Picking a model you can manage.

What doesn't:

- Chasing complexity too early: HMOs and short lets before you understand compliance and operations.

- Buying for theoretical upside: Assuming refurbishments, rents, or refinance terms will all go perfectly.

- Ignoring local rules: The same property can be viable in one council area and awkward in another.

The best rental investment properties aren't always the most exciting. They're the ones where income, management, and regulation stay aligned over time.

The Key Metrics Every Investor Must Master

A listing shows a 7 percent gross yield, the photos look clean, and the rent seems strong for the area. A new investor often stops there. An experienced buyer keeps going, because the gap between headline yield and net return is where good deals survive or fail.

Gross yield has one job. It helps you screen quickly. It does not tell you what lands in your account after management, repairs, insurance, tax friction, local compliance costs, and debt.

Professional analysis starts with income, strips out operating costs, and then tests the cash left after finance. That is why investors spend more time on net operating income and cash-on-cash return than on portal yield calculators, as explained in this property analysis reference on NOI and underwriting.

Start with gross yield, then move to net return

Gross yield is annual rent divided by purchase price. It is useful because it is fast.

Its weakness is obvious in cross-border investing. Two flats can show the same gross yield, while one carries service charges, licensing fees, higher insurance premiums, and frequent maintenance that cut the return sharply. The other may operate smoothly for years.

Use a simple order of analysis:

- Gross income

- Less vacancy allowance

- Less operating costs

- Net operating income

- Less finance costs

- Pre-tax cash flow

- Return on cash invested

That sequence forces you to examine what the property earns, what the structure of the deal does to those earnings, and how much cash you had to commit.

The metrics that matter in practice

Net yield improves on gross yield because it includes recurring ownership costs. It is still a shortcut, but it is a better one.

Net operating income, or NOI, measures the property before debt. That makes it useful when comparing one asset bought in cash with another bought using a mortgage. If the NOI is weak, cheap debt does not fix the asset.

Cash-on-cash return measures the annual pre-tax cash flow against the cash you invested up front. For buyers who use financing, this is often the clearest test of whether a deal is working.

Debt service coverage also deserves attention. A property may look acceptable on a spreadsheet and still become fragile if interest costs rise or rent slips for a few months.

If you want a plain-English breakdown of how operators frame this, Clouddle's NOI strategies are a useful supplementary read.

A simple underwriting example

Assume a property is advertised at a rent that supports a strong gross yield. That tells you very little on its own.

The underwriting questions are practical:

- How many weeks of vacancy should be assumed, based on local letting speed rather than optimism?

- What will routine repairs cost for a building of this age and condition?

- Will the asset need full management, part management, or active owner oversight?

- Are there recurring building costs such as service charges, sinking fund contributions, or compliance checks?

- If finance is used, what happens to cash flow under a higher interest-rate scenario?

That is why serious buyers calculate their return on investment for rental property using a full-cost method rather than relying on a portal headline.

A property can be cheap to buy and expensive to hold.

A market example that sharpens the picture

The UK illustrates why yield alone is a weak guide. Analysts at the UK Office for National Statistics have shown that house prices and rents do not move in lockstep across regions, and the relationship between the two can leave investors with modest income yields even in desirable markets, according to the ONS private rental market summary. In practice, many UK buyers rely on a mix of income, amortisation, and long-term price appreciation rather than rent alone.

That does not make the market good or bad by itself. It means the final decision depends on financing terms, tax treatment, expected hold period, and whether the property still performs under a lower-rent or higher-cost case.

Why global yield tables often mislead

Headline comparisons between cities can hide the factors that drive net return.

A higher-yield market may come with weaker lease enforcement, more volatile occupancy, thin resale demand, or currency risk. A lower-yield market may offer steadier tenants, clearer landlord rights, and more predictable exits. Investors who buy abroad need to compare the full operating model, not just the rent-to-price ratio.

The table below is illustrative. Its purpose is to show why local context matters more than a generic city ranking.

| City | Country | Average Gross Yield |

|---|---|---|

| London | UK | Varies by borough and asset type |

| Berlin | Germany | Often moderate, shaped by regulation and entry pricing |

| Lisbon | Portugal | Depends on central versus suburban stock and local rules |

| Dubai | UAE | Can screen well on headline yield, but fee structure and vacancy assumptions matter |

| Istanbul | Turkey | Income can look attractive, but currency and policy risk need careful modelling |

What to track after purchase

Acquisition is only the start. Returns drift after completion if you do not measure performance against the original underwriting.

Track these items consistently:

- Collected rent, not just contracted rent

- Vacancy by days and by cause

- Operating costs against budget

- Capital expenditure timing

- Debt costs if the loan is variable or due for refinance

- Net cash flow after every recurring expense

Investors who master these numbers stop chasing properties that look good on listing portals. They buy assets that hold up after tax, after finance, and after the practical costs of ownership.

How to Select Your Target Investment Market

Market selection comes before deal selection. A well-bought property in a weak location can tie up capital for years while delivering mediocre income and limited exit options. Investors who buy internationally need a repeatable way to compare places without relying on broad national headlines.

Build a market scorecard

A simple scorecard keeps you focused on variables that affect rent stability and resale depth.

Look at these factors first:

- Employment base: Diverse local employers are usually more durable than one-industry towns.

- Population direction: You want places that attract residents, students, professionals, or retirees for clear reasons.

- Transport and infrastructure: Rail upgrades, airport access, and business districts matter when they change tenant convenience.

- Landlord operating conditions: Local licensing, planning treatment, and tenancy enforcement can alter returns more than a headline yield ever will.

- Comparable rent evidence: Asking rents alone aren't enough.

Accurate rent estimates should be built from neighbourhood-level evidence, not broad regional averages. Professional investors cross-check asking rents, achieved rents, and transaction data, then stress-test the deal under lower-rent and higher-vacancy scenarios before buying, as discussed in this practical underwriting reference on rental comparables.

Established markets versus emerging markets

Established markets tend to offer legal clarity, mature lending systems, and more liquid resale conditions. Cities such as London, Berlin, or Paris usually attract investors who prioritise stability, transparency, and a broad tenant base.

Emerging or less mature markets often appeal because entry prices can feel more accessible and gross income may appear stronger. The trade-off is that investors may face more uncertainty around local enforcement, currency exposure, planning shifts, or transaction friction.

That creates a real strategic split.

| Factor | Established market | Emerging market |

|---|---|---|

| Legal predictability | Usually stronger | Can be uneven |

| Liquidity on exit | Broader buyer pool | More cyclical |

| Entry pricing | Often higher | Often lower |

| Income appeal | Sometimes tighter | Can look stronger at headline level |

| Operational risk | More standardised | More variable |

A practical way to compare two target cities

Suppose you're choosing between a large, proven European capital and a smaller fast-growing market. Don't begin with asking price. Begin with tenant durability.

Ask:

- Who rents there consistently?

- Why do they stay?

- What would stop them renewing?

- If rents soften, does the deal still hold?

- If you had to sell in a weak market, who would buy?

A lot of investors skip the last question. That's a mistake. The exit is part of the underwriting from day one.

For investors comparing locations globally, this guide on where to buy investment property internationally can help structure the shortlist.

Good markets usually reveal themselves through boring strengths. Jobs, transport, affordability, schools, and repeatable rental demand.

What not to rely on

Avoid making a market decision based on one attractive feature. A shiny waterfront district, a new airport route, or an influencer-led “hotspot” narrative isn't enough.

Be wary of:

- Broad national averages: They hide weak neighbourhoods and overstate local viability.

- Listing rents without verification: Asking rent is an ambition, not evidence.

- One-theme markets: Heavy dependence on tourism, one employer, or one policy incentive can create fragility.

Strong market selection isn't glamorous. It's a process of eliminating places where the numbers depend on hope.

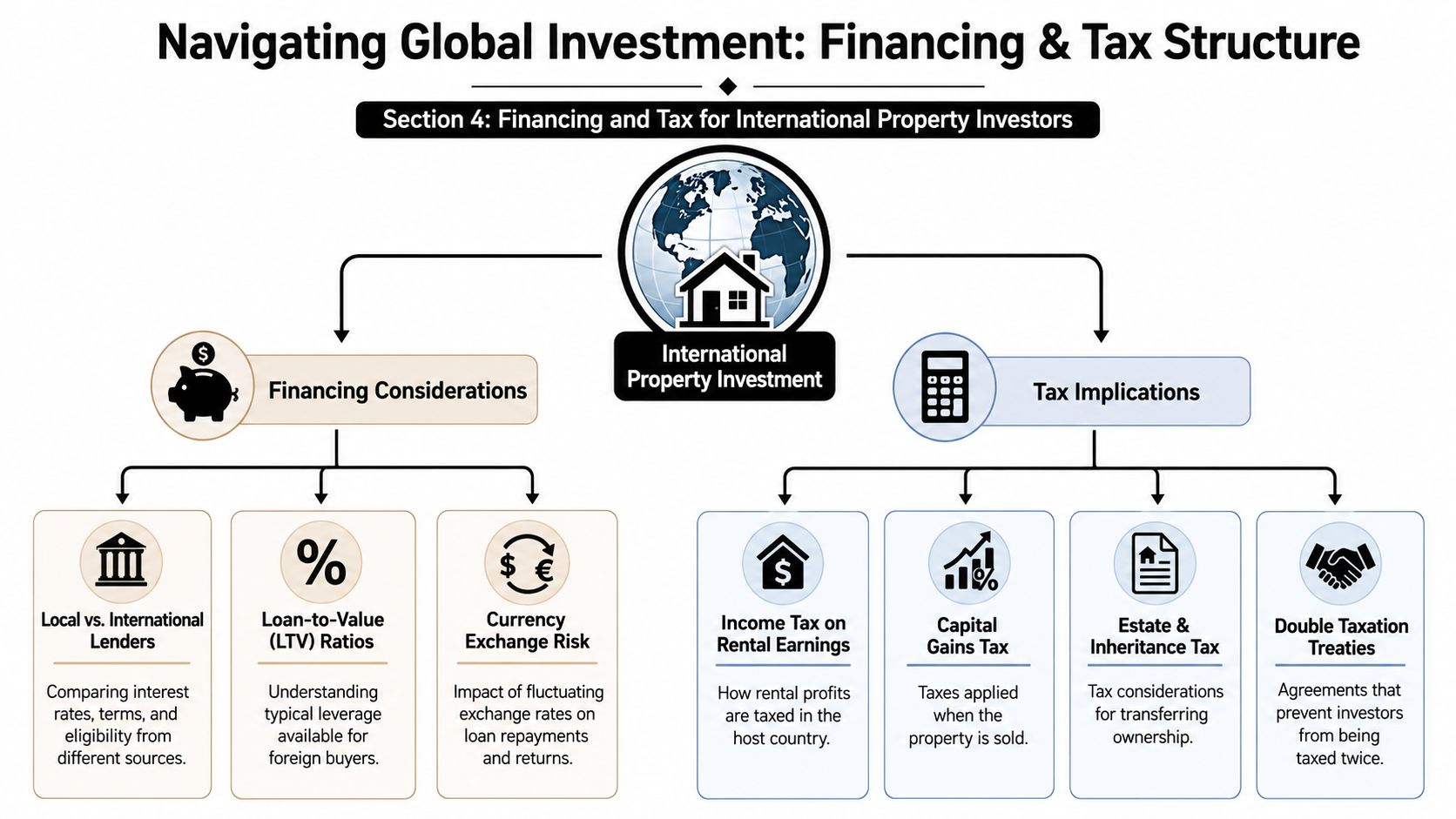

Financing and Tax for International Property Investors

Financing and tax aren't admin issues to solve after you've agreed a purchase. They determine whether the deal works in the first place. Two investors can buy the same property and achieve very different outcomes purely because their debt terms, tax position, and acquisition costs are different.

Financing shapes the whole risk profile

Debt can improve returns when income is resilient and pricing is sensible. It can also magnify errors. That's especially true for overseas buyers, who often face extra documentation, narrower lender choice, and more scrutiny around income sources and residency status.

The key question isn't whether you can borrow. It's whether the debt structure leaves enough room for voids, repairs, and rate changes.

For buyers exploring cross-border lending routes, this guide to a mortgage for buying property abroad is a practical starting point.

The UK example shows why modelling matters

In England, the Renters' Rights Bill aims to remove Section 21 evictions. The Bank of England's Bank Rate was 4.25% in June 2026, and buyers of additional homes in England and Northern Ireland still face a 3% stamp duty surcharge, according to this discussion of UK landlord pressures and market shifts.

Those three items change the economics of buy-to-let directly.

- Tenancy reform: Affects possession risk and operational flexibility.

- Rate environment: Changes mortgage affordability and refinance assumptions.

- Stamp duty surcharge: Raises upfront capital committed and extends break-even timing.

An investor who ignores that stack is underwriting fiction, not property.

The tax stack is broader than many buyers expect

International investors should model tax in three layers:

- Acquisition taxes and fees

- Income tax on rental profits

- Tax at disposal or succession

The exact treatment depends on the jurisdiction, ownership structure, and treaty position. That's why cross-border tax advice matters early. Not because tax should drive the whole strategy, but because tax can erode a decent operating margin.

If you invest in markets where depreciation is part of the tax conversation, it can help to learn MACRS and cost segregation so you understand how some investors model after-tax returns in systems outside the UK.

The best deal on paper often becomes average once tax, debt, and purchase costs are included properly.

What experienced investors do before making an offer

They prepare a full acquisition model that includes:

- All upfront costs: Not just the price, but tax surcharges, legal fees, and financing fees.

- Debt assumptions under stress: What happens if the loan is priced less favourably than expected?

- Post-tax cash flow: Can the property still justify the capital tied up?

- Refinance and exit assumptions: How sensitive is the strategy to future market conditions?

Many attractive listings fall short when assessed thoroughly. The gross income may be fine. The after-finance, after-tax return often isn't.

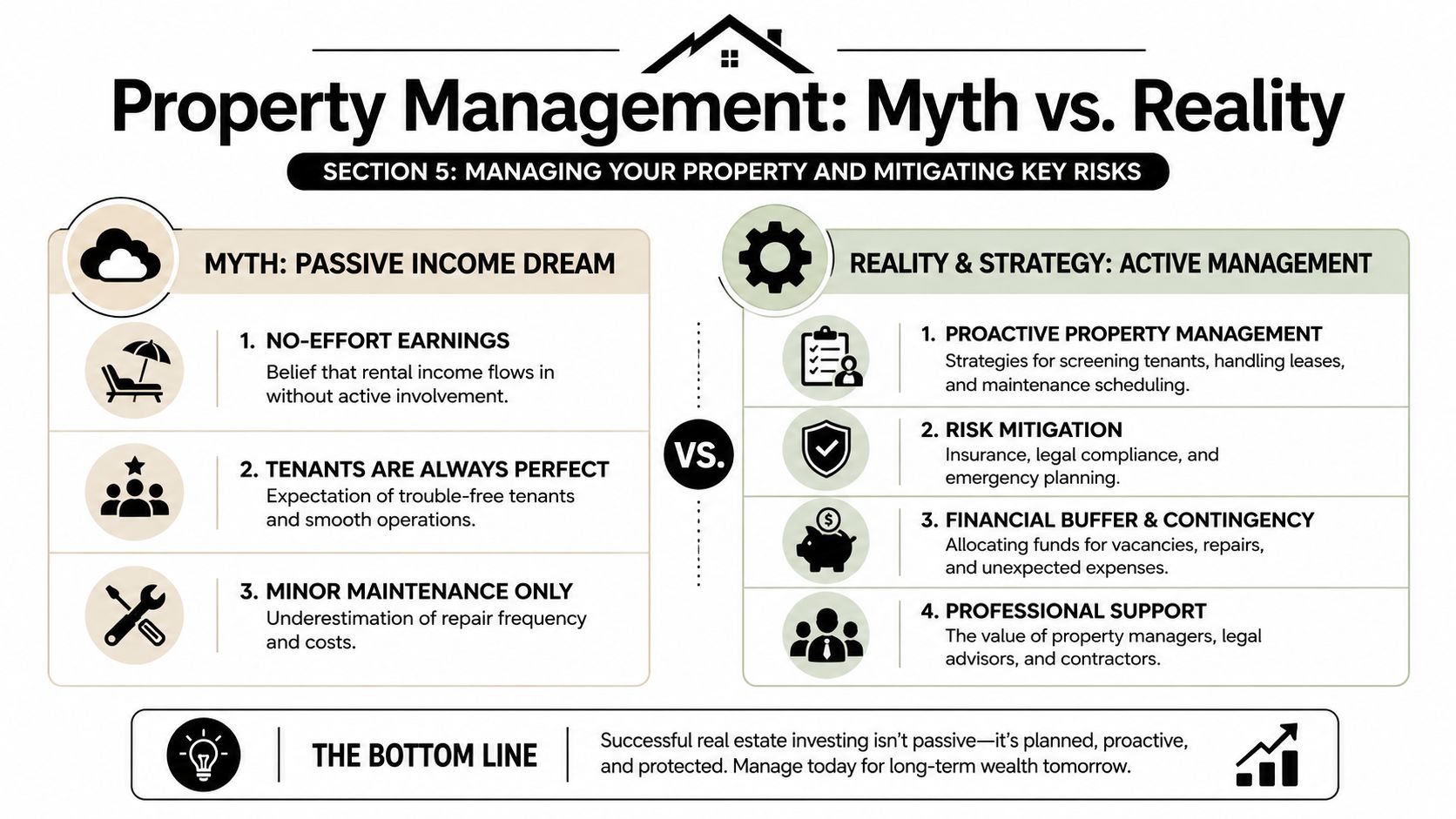

Managing Your Property and Mitigating Key Risks

The phrase “passive income” has done more damage to new landlords than almost any bad yield formula. Rental investment properties can become relatively low-touch once systems are in place, but they are never self-managing.

A property is an operating asset. Tenants leave. Boilers fail. compliance deadlines arrive. Insurance renewals need reviewing. Repairs don't happen on your preferred schedule.

Self-manage or appoint an agent

Self-management gives you control. You choose the tenants, oversee contractors, monitor arrears directly, and stay close to the asset. For local investors with time, experience, and reliable trades, that can work well.

Professional management costs money, but it can reduce friction. A competent agent handles viewings, referencing, paperwork, maintenance coordination, inspections, and tenant communication. That matters more as distance increases or portfolios become more complex.

The right choice depends on your bottleneck.

| Management model | Best for | Main advantage | Main drawback |

|---|---|---|---|

| Self-management | Local, hands-on owners | Maximum control | Time-intensive |

| Professional agency | Distant or time-poor owners | Operational support | Reduced margin if the service is weak |

The core risks to price in from the start

Most risks in rental property aren't surprises. They're neglected line items.

- Void periods: Rent stops, but most costs don't.

- Maintenance spikes: A year of calm can be followed by one expensive quarter.

- Tenant quality issues: Weak referencing often creates expensive downstream problems.

- Compliance failure: Safety, licensing, and tenancy breaches can trigger costs and legal exposure.

- Manager underperformance: A poor agent can increase arrears, delays, and repair spend.

Strong property management doesn't eliminate risk. It makes risk visible early enough to manage.

What good operators do routinely

They create process, not reliance on memory.

A sound operating approach usually includes:

- Tenant screening standards: Consistent checks, documented criteria, and clear affordability review.

- Maintenance triage: A contractor list, repair thresholds, and approval rules.

- Cash reserves: A dedicated buffer for voids and non-routine repairs.

- Compliance diary: Gas, electrical, licensing, insurance, and inspection dates tracked in one place.

- Performance review: Rent level, arrears, repair frequency, and tenant retention reviewed periodically.

The practical edge is boring discipline

Investors often look for an exotic strategy to improve returns. In practice, better results usually come from ordinary discipline done consistently.

That means keeping the property lettable, answering issues promptly, documenting expenditure properly, and reviewing whether the current tenancy model is still the best use of the asset. It also means accepting that lower drama often beats higher theoretical yield.

Well-run rental investment properties rarely feel exciting. They feel organised.

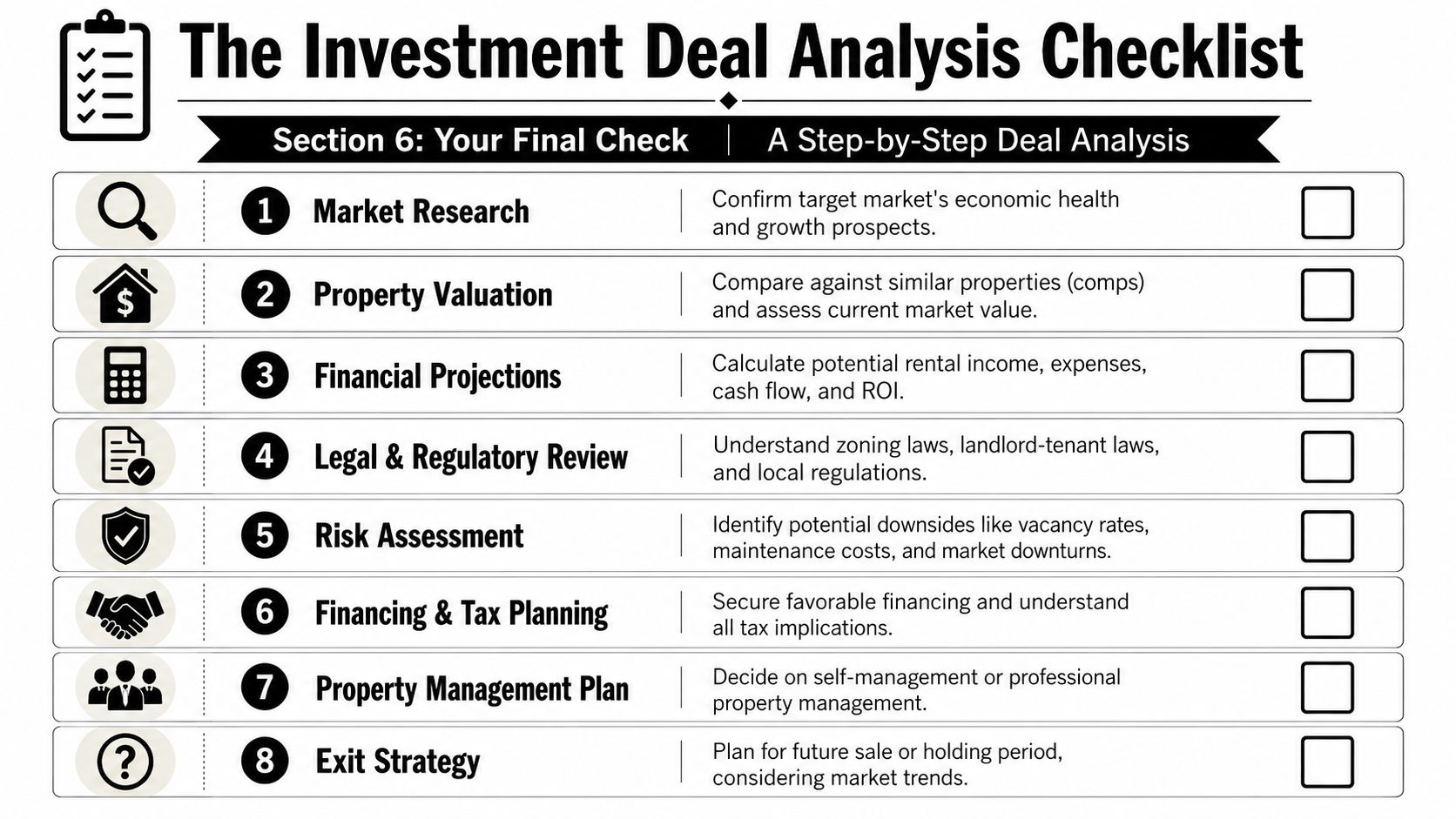

Your Final Check A Step-by-Step Deal Analysis

You are three days from exchange. The agent says there is another buyer circling. The spreadsheet shows a decent yield. Then one rate change, one licensing requirement, or one month of vacancy turns a tidy projection into a weak investment. This final review is where disciplined investors slow down and test whether the deal still works after finance, tax, regulation, and operating friction are stripped of optimism.

The eight checks that matter

Market demand check

Confirm that tenant demand is tied to durable drivers such as jobs, transport, universities, or supply constraints. Avoid markets where demand depends on a short-lived story or a single employer.Comparable evidence check

Verify sale prices and achievable rents against recent local comparables. If your rent assumption sits above what similar units are letting for, your return model is already overstated.Income quality check

Judge the rent by how repeatable and collectible it is, not by the headline figure. A lower rent from a stable tenant base often produces a better net result than a higher rent with frequent turnover.Full-cost underwriting check

Underwrite the property with the costs you will pay. Include vacancy, repairs, management, insurance, taxes, service charges where relevant, and compliance costs. Gross yield is a screening metric. It is not an investment decision.Debt and cash exposure check

Measure total cash in, monthly debt service, refinancing risk, and your sensitivity to higher rates. International buyers should also test currency exposure if income and borrowing sit in different currencies.

A simple acquisition worksheet helps here. An essential guide for rental property budgeting can keep every cost line visible before exchange, especially the ones brokers tend to leave out.

Here's a brief walk-through that complements the checklist:

Legal and regulatory check

Review title, planning use, tenancy rules, licensing exposure, building restrictions, and any local tax changes that affect landlords. In many cities, regulation now changes returns faster than rent growth does.Management reality check

Decide who will manage lettings, maintenance, renewals, arrears, and compliance. Self-management may improve cash flow on paper, but remote ownership often makes professional management the cheaper option over time.Exit check

Identify the likely next buyer and the resale conditions they will care about. Owner-occupier appeal, lending eligibility, building condition, and local supply all affect exit liquidity.

One final valuation lens

A useful final test is to ask what is carrying the investment case. In some markets, rental income does most of the work. In others, the purchase only makes sense if you also expect long-term price growth. If the numbers only hold together with an aggressive growth assumption, price the risk realistically and decide whether that fits your strategy.

The final decision

If the deal works only under favourable assumptions, pass.

If it still holds up with conservative rent, realistic costs, sensible debt, and a workable management plan, it is worth serious consideration. That is how experienced investors get past headline yields and focus on what survives in practice.

World property investment becomes much easier when you can compare markets, rules, yields, and strategies in one place. If you want country guides, city analysis, and practical buying advice for international investors, explore World Property Investor.