Malaysia isn't a fringe property story. It's a USD 42.43 billion market in 2026, with projected growth at a 5.64% CAGR to USD 55.82 billion by 2031 according to Mordor Intelligence's Malaysia real estate market analysis. That immediately changes the frame. Property investment in Malaysia isn't about chasing a cheap holiday apartment. It's about assessing a sizeable Southeast Asian market with real depth, uneven geography, and a widening gap between assets that can compound and assets that look inexpensive.

Many foreign buyers still approach Malaysia with the wrong question. They ask where they can buy cheaply. Serious investors ask where tenant demand is durable, where resale liquidity is most defensible, and where equity can build over time without depending on sales hype. Those are very different filters.

That matters because Malaysia offers both genuine opportunity and visible risk. Residential property still dominates the market. Kuala Lumpur remains the main capital magnet. Johor Bahru is moving fast. Yet the country also carries a meaningful stock of unsold completed homes, and that overhang isn't just a headline. It's a warning that price alone doesn't create demand.

An Introduction to the Malaysian Property Market

Malaysia sits in an unusual position for global investors. It offers a large and still-expanding property market, but it also forces buyers to separate real demand from developer narrative. That's exactly why the country deserves serious attention. The upside is clear enough. The harder task is avoiding the wrong stock.

A disciplined approach to property investment in Malaysia starts with language. Many buyers use terms like yield, LTV, equity, overhang, and cash flow loosely, then make decisions on incomplete assumptions. If you want a quick refresher before comparing deals, Pie Assets' fractional real estate investing glossary is useful because it keeps the terminology straight.

Why Malaysia rewards selectivity

The strongest Malaysian assets usually share three traits. They sit in economically active districts, they attract repeat tenant demand, and they remain understandable to the next buyer. That tends to favour established urban nodes over peripheral launches built around future promises.

The weaker assets often look compelling on brochures. Entry pricing appears low, towers are new, and the marketing pitch leans on eventual infrastructure or a grand masterplan. But if the surrounding demand base is thin, the asset can stay vacant, under-rented, or difficult to exit.

Property investment in Malaysia works best when you treat it as a cash flow and liquidity exercise first, and a story second.

What actually deserves investor attention

The core questions aren't complicated:

- Where is demand anchored: near jobs, transit, universities, hospitals, or established family districts.

- What type of stock fits that demand: compact city apartments, family condominiums, landed homes, or mixed-use units.

- Can returns survive real-world friction: financing costs, vacancy, maintenance, and resale competition.

- Will equity build over time: not because of hype, but because the location remains relevant.

That's the lens worth using. Malaysia can be rewarding, but only if you stop equating affordability with value.

Malaysia's Property Market at a Glance

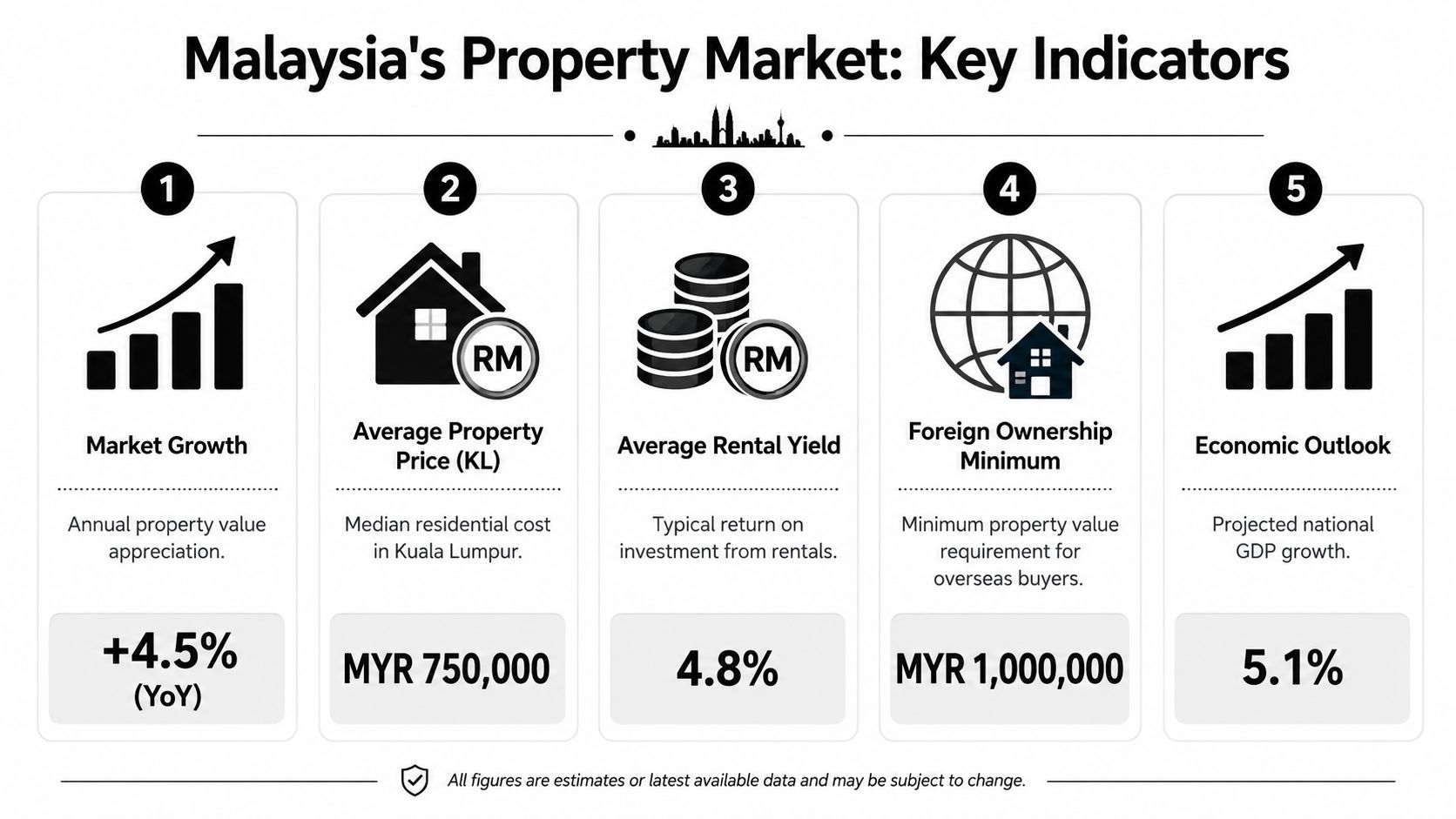

Malaysia's real estate market is projected at USD 42.43 billion in 2026 and USD 55.82 billion by 2031, with residential accounting for 61.35% of the market in 2025, according to Mordor Intelligence's Malaysia real estate report. Those numbers confirm scale, but scale alone is not an investment thesis. In Malaysia, the more relevant question is whether demand is concentrated enough to support occupancy, resale liquidity, and long-term equity growth in the specific submarket you are buying.

That distinction matters because the country's headline affordability often hides a weaker reality. Malaysia has a well-documented overhang problem in parts of the residential market, which means buyers can find units that look inexpensive yet still struggle on rent, vacancy, or exit. Cheap entry pricing reduces upfront capital outlay. It does not guarantee pricing power, tenant depth, or compounding equity.

The market is also uneven by geography. The same report found that Kuala Lumpur captured 44.90% of total revenue share in 2025, while Johor Bahru is projected to grow at a 6.78% CAGR through 2031. Analysts should read that split carefully. Kuala Lumpur has the country's deepest pool of jobs, finance, services, and repeat housing demand. Johor Bahru may offer faster expansion, but higher growth in a secondary market often comes with a narrower margin for error if supply rises faster than end-user absorption.

Residential still leads, but market composition matters more

Residential dominates transaction interest because it is easier for private investors to access and finance. According to the same report, commercial real estate is forecast to grow at a 6.47% CAGR through 2031, and rental assets at 6.32%. That suggests a more balanced reading of Malaysia than the usual condo-led sales pitch. Investors looking only at launch discounts or advertised gross yields can miss the stronger logic in established income-producing assets with proven leasing demand.

This is the point many overseas buyers get wrong.

A low purchase price in an oversupplied corridor can produce weaker real returns than a more expensive asset in a constrained, liquid district. The spread between gross and net yield can widen quickly once vacancy, service charges, maintenance, refurbishment, and resale competition are factored in. For that reason, long-term equity growth in Malaysia tends to come from scarcity, household formation, and durable urban relevance, not from buying whatever appears cheapest per square foot.

Global comparison helps keep expectations disciplined. In the UK, the average gross rental yield is 5.8%, according to Zoopla's buy-to-let analysis. Malaysia can exceed that on paper in selected submarkets, but paper yields are easy to market and harder to collect. A high quoted yield in an overbuilt tower is less valuable than a slightly lower yield with stronger occupancy, better financing treatment, and a clearer resale market.

Where capital tends to concentrate

International capital usually clusters in the most legible city first, then moves outward in search of price dispersion. Malaysia fits that pattern. Kuala Lumpur remains the reference market because valuers, lenders, corporate tenants, and future buyers all understand it better. Penang and Johor can work, but asset selection has to be tighter and the penalty for getting location wrong is usually harsher.

For readers assessing entry routes and asset availability, this guide to property sales in Malaysia helps clarify how stock is distributed across the market.

A short video overview can also help frame the market before drilling into city-level decisions.

What matters at the macro level

Three conclusions stand out:

- Malaysia is large enough to support multiple strategies, but only a narrow slice of the stock offers both income resilience and acceptable exit liquidity.

- Kuala Lumpur still anchors market confidence, because concentration of demand matters more than national averages.

- Growth projections need context, since faster expansion in a city or segment does not reduce risk if new supply is easy to add.

In Malaysia, the strongest investments usually come from buying into proven demand and holding for equity growth, not from chasing the cheapest unit or the highest advertised yield.

Key Investment Hubs Analysed

Around 25,000 completed residential units remained unsold in Malaysia as of Q3 2025, while the average house price in 2023 was about RM467,000, according to Statista's Malaysia real estate overview. Those two figures explain the market better than any promotional brochure. Malaysia is not short of property. It is short of demand for a meaningful share of what has been built.

That distinction matters. Cheap entry pricing can reflect weak absorption, limited financing support, poor tenant depth, or future resale friction. For long-term investors, the central question is not whether a unit looks inexpensive against Singapore, Bangkok, or Dubai. It is whether the asset can compound equity through sustained occupier demand and a credible exit market.

Kuala Lumpur

Kuala Lumpur remains the strongest base case because it has the broadest demand stack in the country. Owner-occupiers, domestic upgraders, professionals, students, multinational tenants, lenders, and valuers all understand the city better than any other Malaysian market. That usually supports tighter bid-ask spreads and more reliable resale evidence.

The practical advantage is liquidity. In global terms, Kuala Lumpur still trades at a discount to many regional capital cities, but the better comparison is not headline affordability. It is market function. A mid-market apartment in an established KL district is usually easier to finance, lease, and resell than a superficially cheaper unit in a peripheral growth corridor.

Asset selection still decides returns. Areas with concentrated employment, rail connectivity, and established retail and social infrastructure tend to hold up best. Fringe districts can show lower entry prices, but they often face direct competition from near-identical new stock. In that setting, rental yield projections are easy to market and hard to defend over a full cycle.

Penang

Penang is narrower and more nuanced. The island has real strengths. It benefits from lifestyle demand, a recognisable brand among expatriates and second-home buyers, and some supply-constrained neighbourhoods. In the right location, that can support pricing better than national averages suggest.

It is still easy to overpay.

Penang often attracts buyers who mistake attractiveness for scarcity. Those are not the same thing. A pleasant address, sea view, or holiday appeal does not guarantee strong long-term equity growth if the buyer pool is limited or if comparable stock can be added nearby. According to the same report, overhang pressure has been concentrated partly on the mainland, which reinforces the need to separate headline Penang demand from submarket-specific risk.

For disciplined investors, Penang works best where neighbourhood quality is already proven and where the unit has features that remain hard to replace. The market can reward patience, but exits are usually thinner than in Kuala Lumpur and pricing can be more sentiment-driven.

Johor Bahru

Johor Bahru offers the widest spread between narrative and execution. Its strategic logic is obvious. It sits next to Singapore, captures cross-border business activity, and benefits from recurring infrastructure and trade-related optimism. Those factors keep capital interested.

They do not guarantee investor returns.

Johor has also been one of the clearest examples of excess supply meeting ambitious marketing. Cross-border proximity helps only when a property matches real occupier demand, daily commuting patterns, and local affordability. Many projects were sold on regional potential rather than on current absorption. That gap is where investors get trapped.

The better approach in Johor Bahru is to treat it as a selective urban market, not a macro story. Focus on districts with proven occupancy, established amenities, and realistic resale depth. Be sceptical of projects priced mainly on future transformation. In Malaysia, "future growth" often arrives with more competing supply.

In Johor Bahru, low prices and high quoted yields often signal market stress rather than opportunity.

Side-by-side comparison

| Metric | Kuala Lumpur | Penang | Johor Bahru |

|---|---|---|---|

| Core investment case | Deepest occupier and resale market in Malaysia | Lifestyle-led market with selective scarcity | Cross-border city with high dispersion between strong and weak submarkets |

| Typical investor stock | Condominiums and serviced residences in established urban districts | Condominiums, selected heritage stock, limited premium lifestyle assets | Condominiums in established districts with real local demand |

| Main strength | Better liquidity, financing familiarity, and tenant depth | Distinctive location appeal and tighter supply in select areas | Strategic position near Singapore |

| Main weakness | Oversupply risk in fringe locations and commoditised towers | Slower exits and a narrower buyer pool | Persistent overhang risk and weaker absorption in some precincts |

| Best suited to | Investors prioritising capital preservation and exit flexibility | Buyers comfortable with a more selective, slower-moving market | Higher-risk investors prepared for sharper due diligence |

If you're benchmarking Malaysia against other major urban markets, this guide to best cities for investment property gives useful international context.

Due diligence at city level also needs tenant-quality screening at asset level, especially for investors underwriting rental income. Spotting AML red flags in lettings is a useful reference when assessing counterparties and compliance exposure.

The disciplined conclusion

For most international investors, Kuala Lumpur is the clearest first market because it offers the best combination of depth, financing logic, and exit clarity. Penang can justify selective exposure where scarcity is real rather than marketed. Johor Bahru can produce upside, but only with tighter filters and a higher tolerance for execution risk.

The common mistake across all three markets is the same. Investors buy "cheap" stock and underwrite returns from advertised yield instead of long-term equity growth. In Malaysia, that is often how capital gets tied up in buildings with limited resale support.

Understanding Malaysia's Legal and Financial Framework

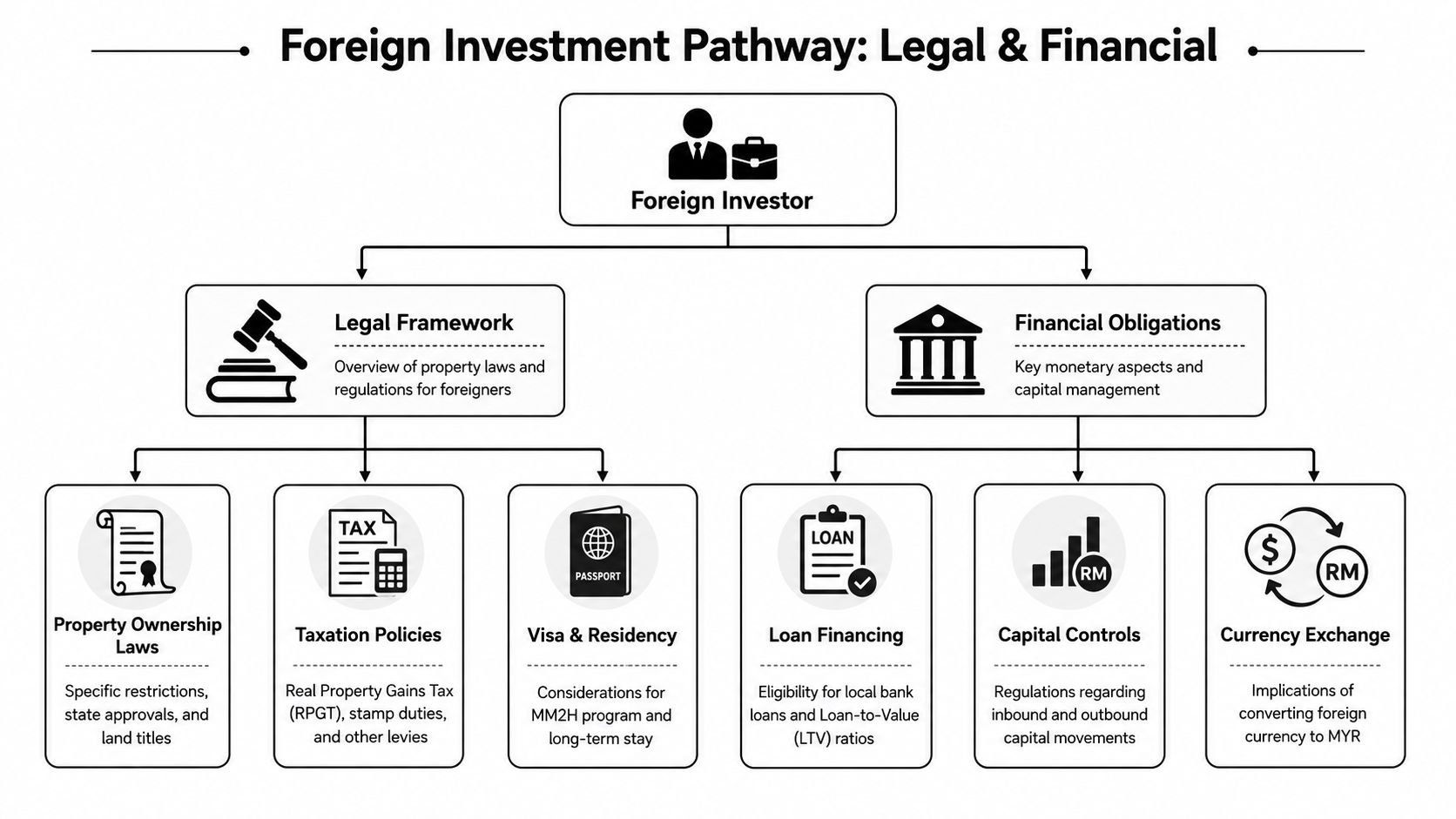

Foreign buyers account for only part of Malaysia's demand base. That matters because resale value is set by the depth of the eventual buyer pool, not by how accessible a launch appears at entry. In a market with visible overhang in several segments, legal eligibility is only the first filter.

Foreign ownership is permitted, but rules are fragmented

Malaysia does not operate as a single rule set for foreign purchasers. State thresholds, approval processes, and asset-type restrictions differ, and those differences can alter both what you can buy and how easily you can sell later. A unit that is legally purchasable is not automatically liquid.

Treat every acquisition as state-specific until counsel confirms the title class, minimum purchase threshold, consent requirement, and any Bumiputera or category restrictions. Investors comparing jurisdictions can use this guide to foreign ownership restrictions by country as a reference point. Malaysia is more open than some regional markets, but openness alone does not create pricing power.

Legal due diligence should test exit quality, not just entry compliance

International buyers should review title, encumbrances, transfer restrictions, management disputes, sinking fund condition, and approval requirements before committing funds. Tax treatment and remittance mechanics also need to be clear at the start, especially for investors who may refinance, repatriate sale proceeds, or hold through a local vehicle.

The sharper question is whether the legal structure supports a credible exit. In overhang-heavy pockets, a foreign buyer can complete a technically valid purchase and still own an asset with limited resale support because the future buyer base is narrow, financing is less available for the next purchaser, or the development has already lost pricing discipline in the secondary market.

Debt only works when the asset is resilient

Cheap stock and available financing are often a bad combination. If the building has weak occupancy, aggressive service charges, poor maintenance, or too many investor-owned units chasing the same tenant pool, debt magnifies the weakness instead of improving returns.

That is why financing analysis has to be tied to asset quality. Stress-test rent against actual achieved comparables, not launch projections. Model vacancy, maintenance, and refinancing risk. Ask whether the building attracts owner-occupiers, stable long-term tenants, or mostly speculative buyers. Those distinctions shape downside risk more than headline yield.

Compliance failures are often early warning signs

Cross-border buyers should also review source-of-funds checks, payment routing, intermediary conduct, and tenancy documentation with the same discipline used for title review. Weak verification standards often sit alongside broader execution problems, including unclear beneficial ownership, side agreements, and inconsistent rental records. For a practical reference, Spotting AML red flags in lettings is useful.

What to verify before committing capital

Use a short, hard filter:

- Confirm purchase eligibility: state threshold, property category, consent process, and title status.

- Check exit depth: local owner-occupier demand, resale comparables, and whether the next buyer is likely to obtain financing.

- Test debt conservatively: interest cost, vacancy assumptions, service charges, and net cash flow under weaker rent.

- Review building quality: occupancy mix, management standards, sinking fund health, and signs of investor oversupply.

- Audit the paper trail: seller identity, payment path, tenancy records, and tax treatment.

Malaysia's legal and financial framework can be workable for foreign capital. It does not rescue a weak asset. In this market, "cheap" frequently means abundant supply, limited pricing tension, and slower equity growth than the marketing suggests.

A Step-by-Step Guide to Acquiring Property

Buying in Malaysia is not especially mysterious, but foreign investors need a process that is disciplined from the first viewing to handover. Most problems don't begin at completion. They begin when a buyer treats marketing material as due diligence.

Engaging professionals

Start with two people, not ten. You need a local lawyer who handles cross-border buyers regularly, and you need an agent who can provide transaction evidence rather than only sales language. If either one becomes evasive when asked for comparables, title information, or management data, move on.

The first round of due diligence should focus on verifiable facts. Ask for rental comparables from completed units, not projections. Ask for management office confirmation on occupancy patterns. Ask whether the building attracts owner-occupiers, long-term tenants, or primarily speculative owners. Those answers shape the investment case more than showroom finishes do.

Offer stage and reservation

Once you identify a target property, keep the negotiation narrow and document-driven. Your offer should be made subject to legal review, title verification, and any foreign purchaser approvals that may be required. Don't negotiate only on price. Negotiate on fixtures, completion timing, vacant possession status, and any rent or tenancy details if the unit is already occupied.

This is also where foreign buyers need discipline on funding. You should know whether you're buying with cash, local debt, or offshore financing before the offer progresses too far. If the funding route is unclear, the seller often gains an advantage.

The Sale and Purchase Agreement

The SPA is the centrepiece of the transaction. It records price, conditions, completion mechanics, default consequences, and the legal transfer process. For foreign buyers, the SPA also needs to work alongside state approval and any conditions imposed by the title or authority requirements.

Don't treat the SPA as a formality. It's the document that decides what happens when the transaction stops being friendly.

A good lawyer will explain what happens if approvals take longer than expected, if defects are discovered, or if the seller fails to deliver on agreed terms. Those aren't edge cases. They are exactly the issues contract drafting exists to manage.

Financing and completion

If you're borrowing, coordinate the bank and solicitor early. Delays often come from poor sequencing rather than from any single major problem. The lender will need documentation, valuations, and legal certainty. Your lawyer will need timing that matches the lender's release process. The cleaner that coordination, the lower the completion risk.

For investors using international finance, this guide to buying property abroad with a mortgage is a useful parallel reference because the underlying principle is universal. Secure the capital route before you become emotionally committed to the asset.

Handover and post-completion checks

Completion is not the end of due diligence. At handover, inspect the property carefully, confirm meter transfers, review management records, and document the unit's actual condition. If the property is tenanted, verify deposit handling, contract continuity, and tenant payment history.

A practical acquisition sequence looks like this:

- Shortlist with evidence: choose only assets backed by real comparables and clear demand drivers.

- Instruct your lawyer early: title checks and foreign buyer requirements should begin before momentum builds.

- Negotiate terms, not just price: possession, timelines, inclusions, and contingencies all affect return.

- Align finance with the asset: don't let a bank's willingness to lend substitute for your own underwriting.

- Close with a manager's eye: think immediately about leasing, maintenance, and exitability.

Buyers who stay methodical usually avoid the obvious traps. Buyers who rush because a project is “selling fast” usually discover too late that sales momentum and investment quality are not the same thing.

Calculating Returns and Avoiding Common Pitfalls

Most mistakes in property investment in Malaysia come from one of two habits. Investors either overestimate income, or they confuse a low purchase price with a good deal. Both errors are common. Neither is hard to avoid if you use stricter filters.

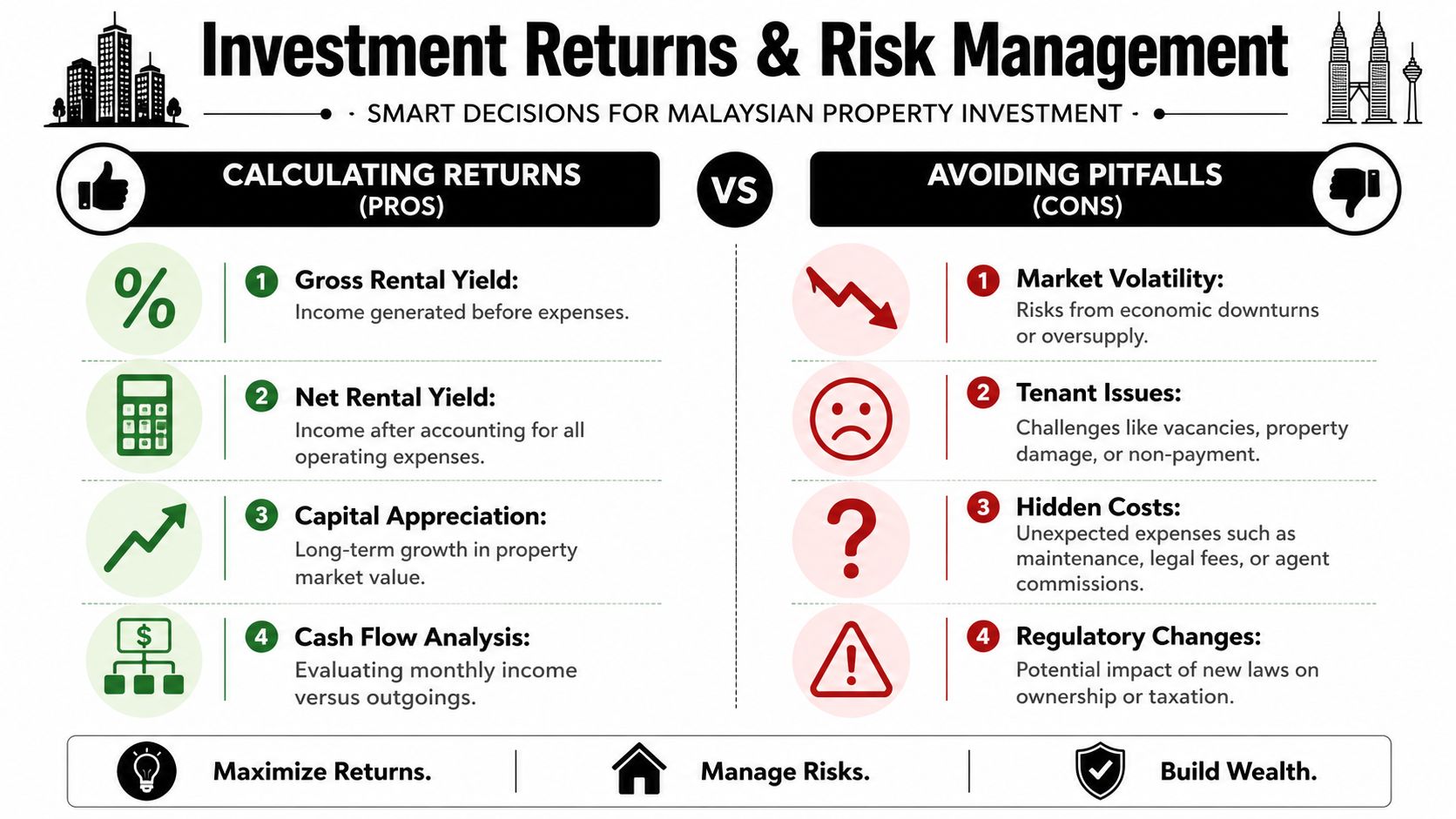

Start with gross yield, but don't stop there

Gross rental yield is only a first pass. It tells you what annual rent looks like relative to the purchase price before costs. That helps compare listings quickly, but it doesn't tell you whether the asset works once service charges, maintenance, vacancy, and financing enter the model.

Net yield is what matters. It is the return left after operating friction. In Malaysia, that distinction is especially important because some projects are marketed with optimistic rents that don't match achieved leases in the building itself. Use actual comparables from completed units. Ignore projections from launch material.

If you want a practical framework for structuring the maths, this guide to how to calculate return on investment property is helpful for building a cleaner model.

Cheap does not equal profitable

This is the most persistent misunderstanding in the market. The presence of unsold lower-priced homes proves that affordability on its own doesn't solve demand. The sharper observation is that some homes priced at $94,100 to $94,000 still remain unsold because of location mismatches and demand deficits, not affordability, as discussed in this analysis of Malaysia's unsold homes and the affordability myth. That directly undermines the beginner's assumption that the cheapest unit is the safest entry point.

A low-entry purchase in the wrong place can lock you into weak rents, low occupancy, and a poor resale market for years.

The better concept is below-market-value in a high-demand zone, not only low nominal pricing. There is a critical difference. One gives you margin in an area people already want. The other gives you exposure to a place people keep avoiding.

The validation criteria that actually matter

The strongest Malaysian deals usually pass objective tests before they ever become “interesting” stories. Use the following framework:

- Demand proof: look for buildings where occupancy is visibly established, not merely forecast.

- Transit relevance: properties close to MRT, LRT, or BRT systems tend to retain broader tenant pools.

- Resale clarity: if the next buyer can't easily understand why the property matters, your exit may be weak.

- Supply discipline: too much similar stock nearby can suppress both rent growth and liquidity.

These tests matter more than brochure incentives, furnishing packages, or temporary rebates.

Don't ignore equity building

There is also a third mechanism of return that many investors underweight. Rental income matters. Capital appreciation matters. But long-term equity building matters just as much because debt amortisation and gradual asset value growth can compound even when short-term gains look unimpressive. The problem is that many investors fixate on headline yield and miss the fact that durable wealth creation often comes from holding the right asset through time rather than trading aggressively.

That perspective is particularly useful in Malaysia, where some districts may produce modest-looking short-term metrics but still offer stronger long-term portfolio value than a superficially higher-yielding unit in a structurally weak location.

Common pitfalls worth rejecting outright

If the investment case depends on future hype, unverified rents, or “cheap entry”, it isn't conservative no matter how low the sticker price looks.

Avoid these errors:

- Buying the developer story instead of the submarket reality

- Using projected rent instead of achieved rent

- Assuming any new build is superior to a well-located subsale

- Ignoring overhang in nearby competing schemes

- Treating yield as the whole return instead of one component

The investors who do best in Malaysia usually look boring at the start. They buy connected, occupied, understandable assets. Then they let time and discipline do the work.

Your Next Steps in Malaysian Property Investment

Unsold stock is still the fact that should shape your next move. In Malaysia, a low entry price can reflect weak absorption, too much competing supply, or a resale market with limited depth. The right next step is to treat your first month as a screening exercise, not a buying trip.

Start by narrowing your search to one city and two or three micro-markets. Build a simple comparison sheet and rank each location on four variables only: achieved resale liquidity, tenant depth, incoming competing supply, and long-term owner-occupier appeal. If a location fails on two of those four, drop it. Cheap units in oversupplied districts often stay cheap.

Then test financing before you spend time on viewings. Foreign buyers should book a call with a Malaysian mortgage adviser or private banker and get a realistic indication of loan-to-value, interest cost, required cash buffers, and whether income earned abroad will be treated favourably. This changes the investment case quickly. A deal that looks acceptable at a headline asking price can become mediocre once financing friction, stamp duties, legal fees, quit rent, assessment tax, and maintenance charges are fully loaded.

Your next action after financing is market verification. Pull recent asking listings, then compare them with achieved rents and observed occupancy where possible. Do not rely on developer material or gross yield tables. In an overhang market, the spread between marketed rent and executed rent can determine whether the asset compounds equity over time or absorbs holding costs.

A practical short list for the next 30 days:

- Book one consultation with a mortgage adviser to test your actual borrowing position

- Select three buildings only and track asking prices, rent levels, and listing age each week

- Visit the micro-location at different times to assess vacancy, retail activity, traffic, and lived demand

- Stress-test the deal with lower rent and slower resale assumptions

- Set a clear reject price before negotiation starts, then keep to it

One more point matters. Decide what would make you walk away. If your strategy depends on fast appreciation, a foreign buyer resale premium, or a future supply correction that has not yet arrived, you are speculating on sentiment rather than buying an asset with durable equity growth.

That discipline matters more in Malaysia than in many tighter global markets. In cities where supply is constrained, investors can sometimes survive a mediocre entry. In oversupplied submarkets, entry discipline is the whole trade.

If you're comparing Malaysia with other international markets, World Property Investor publishes data-led country and city guides that help you assess yields, foreign ownership rules, taxes, and buying processes across global property markets before you commit capital.