You're close to exchange, the mortgage offer is in, and the property itself looks straightforward. Then your solicitor asks a question many buyers don't expect: do you own any residential property anywhere else in the world?

That's where stamp duty on overseas property exposure starts to bite. A flat inherited abroad, a holiday apartment in Spain, a family home in Australia, even a timeshare in Florida can change the UK tax result on a purchase you assumed was a standard residential acquisition.

I see this confusion often with internationally mobile buyers, expats returning to Britain, and investors building portfolios across several jurisdictions. They focus on price, rental demand, finance, and currency risk. The transfer tax bill comes later, and by then it can be expensive to rethink the structure or timing.

The Hidden Costs of Investing in Global Property

A buyer based overseas often looks at a UK purchase in isolation. They budget for the deposit, legal fees, finance costs, and refurbishments. What gets missed is that property taxes don't work in isolation. Tax authorities often look at the buyer's wider position, including assets held overseas.

In the UK, that issue is particularly sharp. Someone can be buying their first home in Britain and still be taxed as if they are buying an additional dwelling because they already own residential property abroad. That catches people who don't think of themselves as “second-home buyers” at all.

That problem isn't unique to Britain. Around the world, transaction taxes sit at the front end of the deal and reduce usable capital on day one. If you're buying across borders, you also need to think about banking friction, foreign exchange timing, and remittance mechanics. A practical starting point is comparing payment solutions for global businesses, especially if your purchase involves moving funds between jurisdictions rather than relying on a single domestic bank.

Tax mistakes at purchase stage are usually harder to fix than financing mistakes. The tax is triggered when you complete. By then, your options are limited.

For many investors, the issue isn't just the headline tax. It's the combination of transfer tax, cross-border ownership rules, and cash movement costs. That's why I always treat the tax estimate and the money-transfer plan as part of the same exercise, alongside a review of international transfer fees for property investors.

What Is Stamp Duty and How Does It Vary Globally

A buyer agrees a price of £500,000 for a flat in London and assumes the tax calculation starts and ends with the UK rate bands. In practice, the purchase tax can look very different once local transfer rules, residency tests, and ownership elsewhere are taken into account.

Stamp duty is the catch-all term many investors use for taxes charged on a property purchase, but each country builds that charge differently. In England and Northern Ireland, the main tax is Stamp Duty Land Tax (SDLT). Scotland applies Land and Buildings Transaction Tax (LBTT), including the Additional Dwelling Supplement, and Wales uses Land Transaction Tax (LTT). Outside the UK, the same cost may appear as transfer tax, registration duty, acquisition tax, or a mix of tax and filing fees.

The UK as the reference point

The UK is a useful benchmark because it shows how quickly purchase tax stops being a simple percentage. SDLT is banded. Surcharges can then sit on top. For overseas buyers, that stacking effect matters more than the headline rate.

Under the Scottish rules, Revenue Scotland states that the Additional Dwelling Supplement can apply where a buyer owns another dwelling anywhere in the world, and that one condition is that the dwelling is worth £40,000 or more. The supplement rate is 5% of the total purchase price of the dwelling being acquired (Revenue Scotland ADS guidance). That is a good illustration of the wider point. In cross-border property tax, the total cost often comes from layered surcharges, not from the base transfer tax alone.

Buyers who want a grounding in the UK rules before modelling an overseas acquisition should review what stamp duty on property means in practice.

Why global comparisons matter

The label changes by country, but the investor's question stays the same. How much cash disappears on day one, and what conditions trigger extra tax?

| Market type | Common approach | What investors should check |

|---|---|---|

| Established mature markets | Detailed rate bands, formal filing rules, and targeted surcharges | Residency status, ownership history, treaty position, reliefs |

| Emerging or fast-growing markets | Lower visible transfer taxes in some cases, but more execution risk outside the tax itself | Registry reliability, title process, local legal fees, enforcement practice |

| Lifestyle-driven destinations | Purchase taxes may look moderate, but second-home or non-resident charges can materially raise entry cost | Use restrictions, foreign ownership rules, resale taxes, annual holding taxes |

A lower transfer tax rate does not automatically make the deal cheaper. Some jurisdictions recover cost through registration charges, municipal fees, wealth taxes, or higher annual property taxes. Others look cheap at acquisition but create more legal and administrative risk around title, financing, or resale.

That is why I compare property taxes in two layers. First, the published transfer tax. Second, every surcharge or related cost that can attach because of who the buyer is, what they already own, and how the property will be held. Investors also need to factor in downstream consequences such as rental profit taxation, especially if the purchase is part of a buy-to-let strategy. For that, essential 2026 landlord tax is a useful reference point.

The Surcharge Trap Owning Property Anywhere Affects Your UK Tax

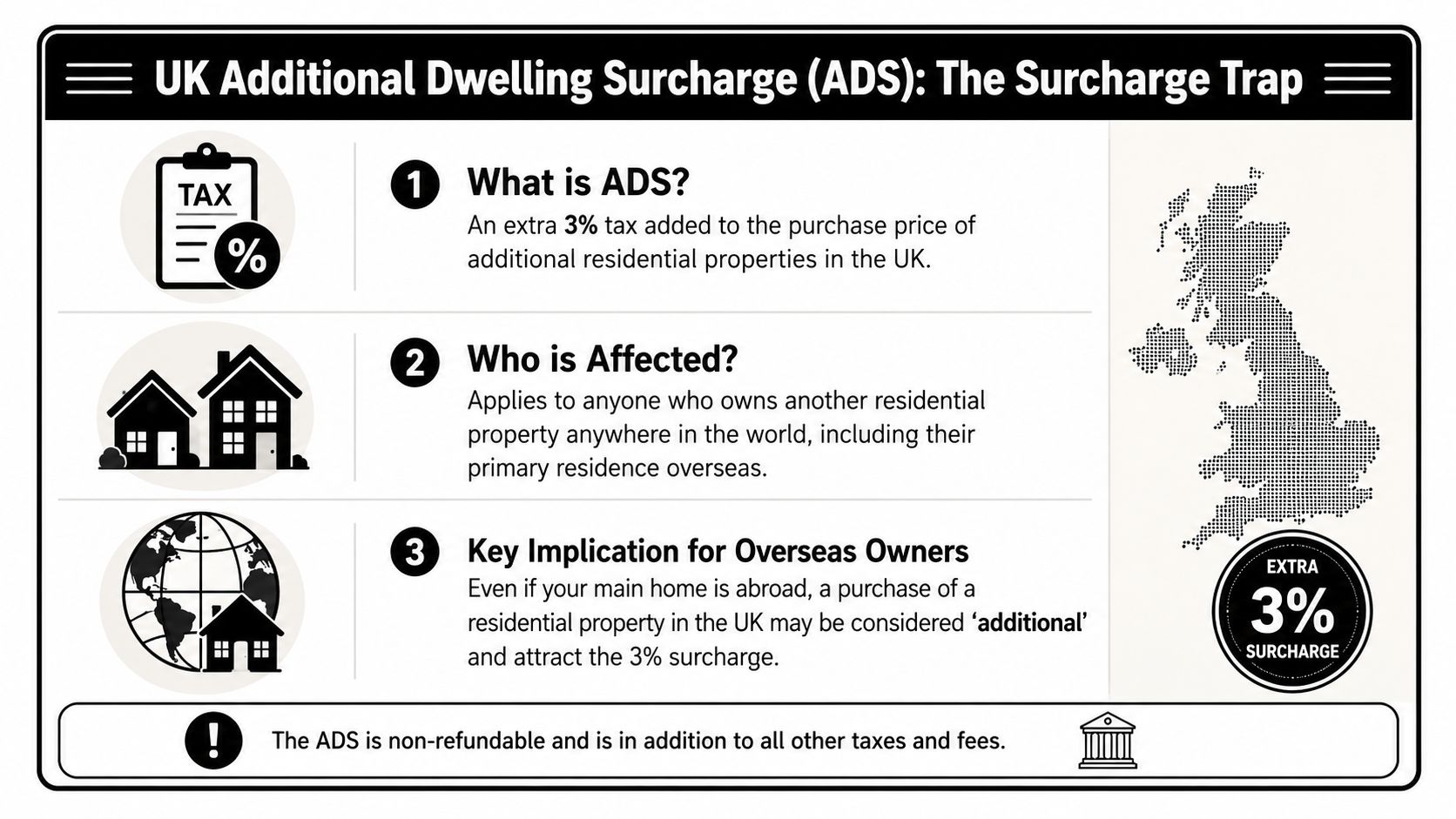

The most misunderstood rule in this area is the UK's worldwide property test for the additional dwelling surcharge. Buyers often assume that a main residence overseas should be ignored if the new UK purchase will become their home. That assumption is wrong far more often than people expect.

The rule looks at residential property ownership anywhere in the world. If you already own a qualifying residential property overseas, your UK acquisition can be treated as an additional dwelling even where it feels, commercially, like a straightforward move into the UK.

The worldwide property rule

The key point is unusually blunt. GOV.UK states that the rule applies to property “anywhere in the world” worth £40k+, with no exemption for a principal home abroad. That means a buyer with a £300k home in Australia pays a 5% extra surcharge, equal to £15k, on a new £300k UK purchase, even if that UK property becomes their main home (analysis of the property abroad UK surcharge rule).

That's where many buyers get caught. They aren't buying a pied-à-terre. They aren't building a buy-to-let portfolio. They're relocating. But if the old overseas home still exists at completion, the surcharge can still apply.

Practical rule: Don't rely on your own description of the property. “It's my family home overseas” isn't the legal test. Ownership, value, and timing matter more.

The non-resident surcharge is separate

A different charge can apply if the buyer is treated as non-UK resident for SDLT purposes. The rule is distinct from the worldwide property test. You can trigger one surcharge, both surcharges, or neither, depending on the facts.

That distinction matters because buyers often confuse residence with property ownership. They think if they are moving to the UK, that should neutralise the overseas ownership issue. It doesn't necessarily. Equally, someone may not own another property at all, but still face the non-resident position.

A practical review of non-resident landlord tax in the UK is worth reading alongside SDLT planning because investors often focus on the purchase tax and forget the ongoing income-tax obligations.

What usually works and what doesn't

In practice, these are the approaches I see most often:

- Good planning: Buyers review global property holdings before making an offer, not after survey and legal costs have already been incurred.

- Poor planning: They assume a solicitor will automatically optimise the position. Solicitors identify liability. They don't always provide broader cross-border tax strategy.

- Good planning: Families map out who legally owns each overseas asset, including part-shares and inherited interests.

- Poor planning: They ignore low-attention assets such as timeshares, minority interests, or older overseas apartments because they don't regard them as investment property.

For landlords, broader purchase planning should sit next to an annual tax review. Resources on essential 2026 landlord tax can help frame the ownership decision after completion, especially where the property is intended for rental rather than owner-occupation.

Calculating Your True Tax Cost How Surcharges Stack

The expensive part isn't that surcharges exist. It's that they stack.

For a non-UK resident buying an additional residential property, the standard SDLT rates don't disappear. The buyer pays those rates and then adds the relevant surcharges on top. GOV.UK confirms that the combined 2% non-resident surcharge and 5% additional dwelling surcharge create a 7% effective premium, and for a non-UK resident buying a second home over £1.5m, the top rate reaches 19% on that portion of the price (GOV.UK guidance on rates for non-UK residents).

How to think about the stack

Use this order when reviewing a deal:

- Start with standard SDLT bands. This is the base transaction tax.

- Add the additional dwelling surcharge if you already own qualifying residential property.

- Add the non-resident surcharge if your SDLT residence test puts you in that category.

- Review whether any relief applies. Relief is not assumed. It has to be tested.

This is why headline online calculators often understate the true figure unless you input every relevant fact correctly. Investors who model only the standard rate can approve a deal that looks acceptable on gross yield and then discover the net entry cost is much heavier.

Worked logic without false comfort

Take a London investor who is non-UK resident for SDLT purposes and already owns residential property abroad. The purchase isn't analysed at one blended rate. It is analysed through the standard SDLT framework, then increased by the relevant surcharges.

That means the tax drag applies from the lower bands upward, not just at the top end. Buyers often think the surcharge only matters for expensive prime property. That's wrong. The stack affects mainstream purchases as well, and it changes the break-even period on the investment from the day of completion.

If your acquisition model only shows purchase price, legal fees, and mortgage costs, it isn't a real acquisition model.

A reliable sense check is to compare your own estimate with a specialist tool such as a stamp duty calculator for property investors. Use that only as a starting point. It won't replace legal and tax advice, but it will usually reveal whether your assumptions are missing a surcharge.

The investment consequence

This stacking effect changes more than the tax line. It can alter:

- Net yield on entry: More capital is tied up before the property earns anything.

- Cash buffer requirements: Investors need more liquidity for tax and completion costs.

- Refinancing assumptions: The extra tax is equity outlay, not mortgageable value in most structures.

- Exit discipline: A deal with a heavy entry tax usually needs a longer hold or stronger rental profile to compensate.

In established markets, buyers often accept these costs because legal systems, finance options, and tenant demand are more predictable. In emerging markets, the transfer tax may look lighter, but buyers can face more uncertainty in enforcement, title, and resale. Good planning weighs both sides.

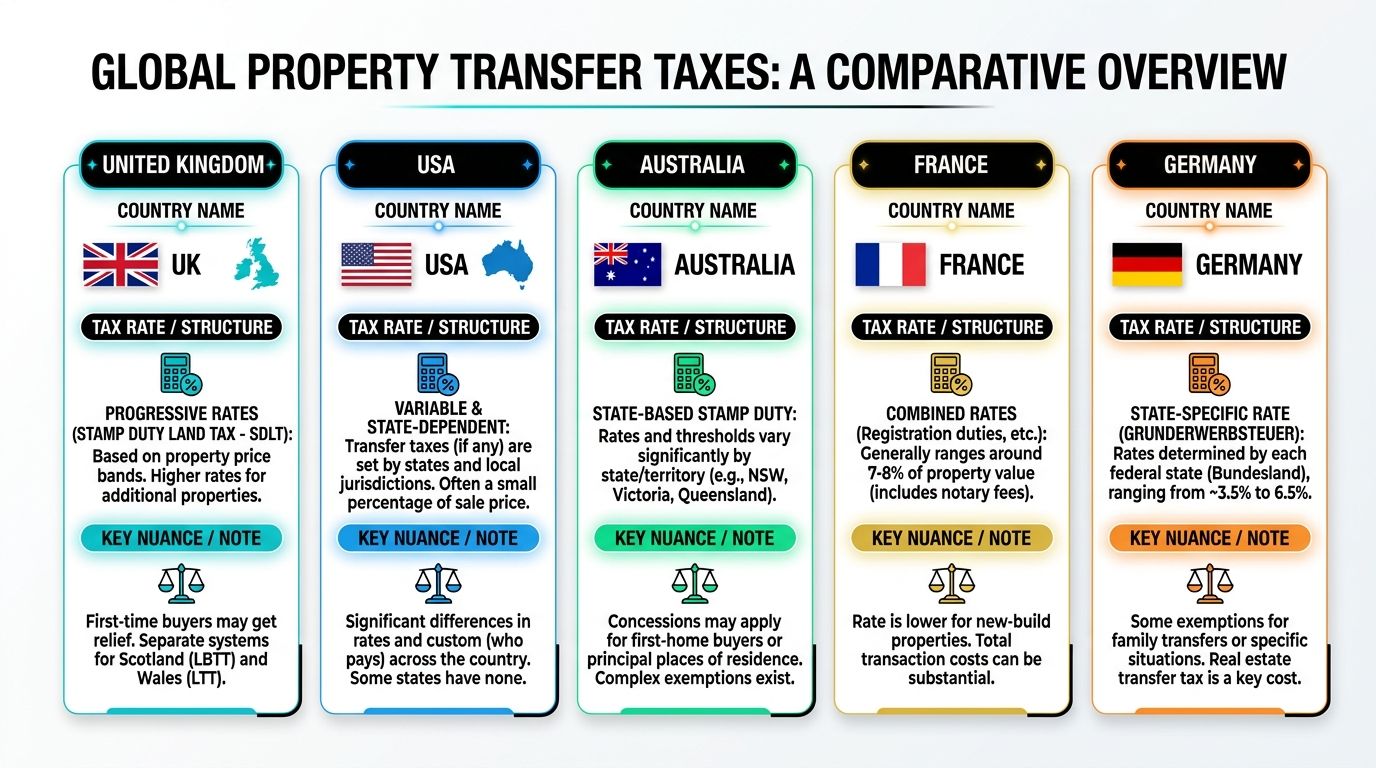

Global Snapshot Property Transfer Taxes in Key Markets

Investors often ask whether the UK is unusually harsh. The honest answer is that each market punishes a different mistake. Some penalise second homes. Some focus on non-residents. Others keep the transfer tax framework simpler but introduce complexity through registration, municipal charges, or restrictions around ownership and use.

Comparing established and emerging markets proves beneficial. Mature markets usually have more codified systems. Fast-growing markets can be easier to enter on paper, but less forgiving if you assume the buying process works like London, Manchester, or Birmingham.

A practical comparison table

| Market | Main transfer tax label | What tends to define the investor experience |

|---|---|---|

| United Kingdom | SDLT in England | Progressive structure with surcharge layering that can be severe for additional dwellings and non-residents |

| Spain | Commonly ITP on resales | Regional variation matters. Buyers need local review rather than national assumptions |

| Portugal | IMT | Purchase tax sits within a wider cost stack that can include registration and legal expenses |

| Dubai | DLD fee structure | Often feels administratively efficient, but investors should still test title, service charges, and holding costs |

| Australia | Stamp duty | State-based rules matter, and foreign-buyer treatment can differ materially by location |

Established markets and the price of certainty

In places such as the UK and Australia, investors usually get stronger institutional process, clearer lender expectations, and more predictable enforcement. The trade-off is that the tax system is rarely simple. Rules are documented, but that doesn't mean they are intuitive.

For example, the UK's surcharge framework is conceptually clear once you know it. The problem is that many investors don't realise the tax analysis begins with their global asset base, not just the property under contract.

Australia illustrates a different version of the same lesson. The country is attractive to many overseas investors, but tax and foreign ownership treatment can vary depending on the state and the buyer's status. Anyone considering that market should review a dedicated guide to foreign property investment in Australia before comparing headline costs with Britain or southern Europe.

Emerging and lifestyle markets need a different filter

Spain, Portugal, and Dubai are popular for different reasons. Spain and Portugal draw lifestyle buyers, retirees, and holiday-let investors. Dubai attracts globally mobile capital looking for liquidity, newer stock, and a different tax environment.

The mistake is to compare these markets only on purchase tax. I'd use a broader checklist:

- Title and registry process: Is the legal transfer system efficient and well understood by foreign buyers?

- Use restrictions: Can you let the property short term, long term, or only under licence?

- Funding reality: Will local banks lend to non-residents on terms that make the acquisition viable?

- Exit route: Can you resell easily to domestic and foreign buyers, or is the market thin?

The cheapest entry tax can still lead to the weakest investment if the exit market is narrow and the legal process is slow.

What investors should compare before choosing a market

A useful side-by-side review should include more than tax labels. Assess each market under four headings:

| Decision area | Established markets | Emerging or faster-moving markets |

|---|---|---|

| Transfer tax clarity | Usually stronger | Sometimes simpler, sometimes less transparent in practice |

| Financing access | More standardised | Can be uneven or relationship-driven |

| Rental demand visibility | Better historic data | Often more story-driven, with less dependable data depth |

| Execution risk | Lower process risk | Higher risk around title, regulation, or resale timing |

That's why stamp duty overseas property analysis should sit inside a full market review. Tax is the first filter, not the only one.

Strategic Planning Exemptions Reliefs and ROI

A common pattern causes expensive mistakes. A buyer owns a home in Dubai, Spain, or Singapore, assumes it sits outside the UK stamp duty analysis, then discovers too late that HMRC looks at worldwide residential property ownership when testing the additional dwelling surcharge. If the buyer is also non-UK resident for SDLT purposes, the charges can stack from day one.

That is why planning starts with facts, not structures. The key questions are simple. What do you own anywhere in the world on completion day, which property is your only or main residence, and will any disposal happen within the refund window?

The main relief investors focus on is replacement of main residence. It can reduce or recover the higher rates charge, but only where the statutory conditions are met. HMRC's guidance confirms that a previous main residence can be located outside the UK, and a refund may still be available if that former main residence is sold within 36 months after the new purchase (HMRC SDLT Manual, higher rates for additional dwellings).

In practice, timing does most of the work.

A sensible pre-exchange review should test four points:

- Whether the overseas main home can be sold before the UK completion date

- Whether the facts support a genuine main residence replacement claim, rather than ownership of an extra property

- Whether UK non-resident SDLT status applies on the effective date of the transaction

- Whether the acquisition still meets the target return if no refund is available

The commercial point is easy to miss. Surcharges do not just increase tax. They raise the amount of capital tied up at entry and lower your real return on equity.

For a £500,000 residential purchase in England or Northern Ireland, the standard SDLT position, the higher rates for additional dwellings, and the position after the October 2024 increase produce very different outcomes under the published rates. HMRC sets out the standard residential bands, and GOV.UK confirms that the higher rates surcharge for additional dwellings increased from 3 percentage points to 5 percentage points from 31 October 2024 (SDLT rates on GOV.UK, Autumn Budget 2024 policy paper on higher rates for additional dwellings). On that price point, the surcharge increase alone adds £10,000 compared with the earlier 3 percent regime.

That extra cost buys nothing operationally. It does not improve rent, financing terms, or resale prospects. It raises the hurdle your investment has to clear.

I model purchase tax as part of total capital employed from the outset. If the deal only works on a gross yield before transfer tax, financing, and likely exit tax, it is usually too thin. Cross-border buyers should underwrite the asset after all entry charges, with the worldwide property rule and any stacked surcharges built into the numbers before exchange.

Key Takeaways for Global Property Investors

Cross-border property buying looks simple until the tax system starts looking at your wider footprint. That's why stamp duty overseas property planning matters so much. The issue isn't only the local purchase. It's how your overseas assets, residence status, and transaction timing interact.

Three points matter most:

- Transfer taxes vary widely by country. The same property budget can produce very different acquisition costs in the UK, Spain, Portugal, Dubai, or Australia.

- Owning property abroad can directly increase UK stamp duty. A buyer's first UK home can still be taxed as an additional dwelling if another qualifying residential property is already owned overseas.

- Surcharges can stack. If non-resident and additional dwelling rules both apply, the total cost can be far higher than many buyers expect.

The practical answer isn't guesswork or forum advice. It's coordinated legal and tax analysis before exchange, based on the jurisdictions involved and the exact ownership facts. If you're signing a purchase contract before that review is done, you're taking avoidable risk.

If you're comparing countries, evaluating yields, or stress-testing the full costs of an international acquisition, World Property Investor offers market guides, tax-focused buying advice, and country-by-country analysis to help you research property investments with more confidence.