Your Australian portfolio may already be doing its job. The home market has given you capital growth, borrowing power, and familiarity. But once you start looking for diversification, income in another currency, or a foothold in a market you know well from business or family ties, the question becomes practical very quickly: how do you buy property overseas from Australia without making an expensive structural mistake?

That's where most investors go wrong. They start with a destination. London, Florida, Lisbon, Milan. The better approach is to start with the bridge between Australia and that market. Finance, tax, legal process, currency movement, and ownership rules will shape the deal long before the property itself does.

For Australians, overseas buying isn't just a matter of finding a good apartment or a house in the right suburb. It's a cross-border transaction that sits across at least two legal and tax systems. If the structure is weak, a good asset can still become a poor investment. If the structure is sound, the search becomes much clearer.

I've found that experienced buyers usually have one of three motives. They want income diversification, long-term capital exposure outside Australia, or a dual-purpose asset they can use personally while still treating it as part of a portfolio. Each motive leads to a different market shortlist and a different financing plan.

A useful starting point is this broader guide on buying property abroad as an international investor. From there, the Australian-specific issues deserve their own playbook.

Introduction Thinking Beyond Australian Shores

An overseas property purchase often starts with a familiar frustration. You know the Australian market well enough to see its limits for your own portfolio, yet every overseas market looks opaque when viewed from Sydney, Melbourne, Brisbane, or Perth. The gap isn't usually ambition. It's confidence in the process.

That process becomes manageable once you stop treating it as a property search and start treating it as an international investment decision. The destination matters, but the sequence matters more. Define the goal. Test the financing. Map the tax position. Confirm the ownership rules. Only then should you spend serious time reviewing stock.

The appeal is obvious. A property in the UK can give exposure to a different economic cycle. A US acquisition can align with a dollar-based strategy. A Portuguese purchase may combine lifestyle optionality with a European foothold. Those are valid reasons, but none of them substitute for a proper acquisition framework.

Working rule: The best overseas purchase is rarely the property you like most. It's the one you can finance cleanly, own compliantly, operate efficiently, and exit without surprises.

That is the genuine discipline behind how to buy property overseas from Australia. Not hype. Not brochures. Not a romantic attachment to one city. Just a sequence of decisions that holds together under scrutiny.

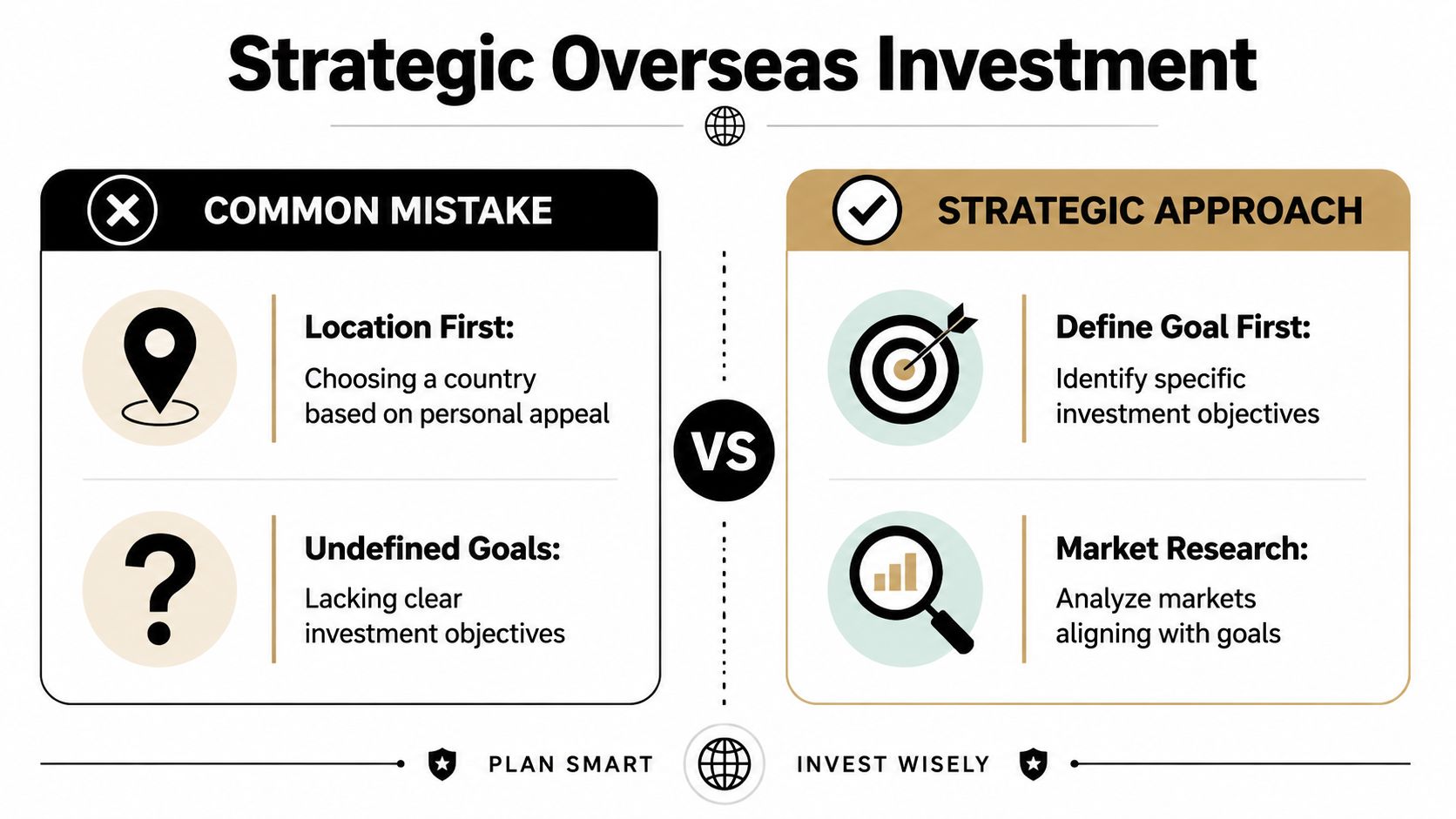

Choosing Your Market Strategy Before Location

Most investors pick a country too early. They visit a city, like the feel of it, read a few headlines, and start browsing listings. That's backwards.

You need an investment thesis before you need a postcode. If you don't define the role the asset will play in your wider balance sheet, every market can look attractive for the wrong reasons.

A practical starting point is to compare markets through three filters.

Define the purpose of the asset

If your primary goal is steady ownership in an established, rules-based market, the UK often sits high on the list. It's familiar to Australian investors, highly regulated, and relatively straightforward to understand at the title and tenancy level once you have local advisers in place.

If the goal is higher operational upside, some investors look at markets such as Portugal, parts of Southern Europe, or selected US cities where short-let or tourism demand may influence returns. The trade-off is that income can become more management-intensive, and the legal and tax treatment often needs closer attention.

If the goal is personal use with an investment backstop, your shortlist changes again. A holiday asset or future relocation option should be judged differently from a pure buy-to-let purchase. Many buyers blur those categories and end up with a property that satisfies neither objective particularly well.

Separate established markets from emerging opportunities

Established markets usually offer deeper liquidity, more transparent legal systems, and clearer rental demand. They also tend to be more competitive and less forgiving if you overpay. The UK is a good example of a market where regulation is part of the investment case. You may accept tighter margins in exchange for stronger institutional depth.

Emerging or less familiar markets can look compelling on paper because the story is easy to sell. New infrastructure, tourism growth, urban renewal, or residency-linked demand often attract international capital. What matters is whether those drivers are durable and whether foreign owners can operate efficiently once they own the asset.

Here's the comparison I use with clients at the shortlist stage:

| Market type | Usually works for | Main strength | Main risk |

|---|---|---|---|

| Established markets such as the UK | Buyers prioritising transparency and long-term defensibility | Strong legal and regulatory clarity | Lower margin for error on pricing and tax leakage |

| Lifestyle-led European markets such as Portugal | Buyers mixing personal use with income potential | Broader lifestyle utility and international demand appeal | Operational complexity and local compliance |

| Selected US metropolitan or Sun Belt markets | Buyers seeking scale and wider submarket choice | Depth of stock and varied strategies | Distance, local property tax exposure, and management execution |

Build a shortlist from fundamentals, not headlines

A market deserves attention when you can answer four questions clearly:

Who rents there and why

Students, professionals, corporate relocations, tourists, retirees, or local families create very different income profiles.What drives local demand

Universities, transport improvements, major employers, or supply constraints matter more than generic “growth stories”.How easy is it to manage from Australia

Remote ownership can work well, but only if the market supports reliable legal, banking, lettings, and maintenance infrastructure.What happens if you need to sell

Some markets are easy to buy into and slow to exit. That's not always obvious at entry.

A more detailed market comparison framework is useful at this point. This guide on where to buy investment property globally helps narrow options before you spend money on due diligence.

A good overseas market should match your purpose before it promises a return.

What usually works and what usually doesn't

What works is boring, disciplined selection. Buyers define whether they want income, growth, personal use, or optionality. Then they choose a market that naturally supports that objective.

What doesn't work is buying in a place you enjoy visiting and then reverse-engineering an investment case around it. That mistake is common in Europe. It also appears in US resort and second-home markets where purchase enthusiasm outruns operating reality.

If you want a portfolio asset, act like an investor first and a future visitor second.

Securing Finance The Australian Investor's Playbook

An Australian buyer agrees on a flat in Manchester or a condo in Florida, assumes the overseas bank will lend against that property, then discovers the bottleneck is much closer to home. Borrowing capacity is often set by Australian equity, Australian income evidence, and how an Australian lender treats foreign commitments.

For Australians, funding an offshore purchase is usually a capital-structure exercise before it is a property exercise. The practical question is not, “Can I borrow?” It is, “Which balance sheet should carry this asset, in which currency, and with what tax and reporting consequences back in Australia?”

Australian buyers usually end up in one of three lanes. They release equity from property held in Australia, borrow locally in the destination market, or use an international private bank or specialist cross-border lender. Each route solves a different problem, and each creates a different risk profile.

The three funding routes and the trade-offs

Equity release in Australia is often the fastest and most controllable option if you already hold usable equity. Wise notes that Australians buying abroad may be able to release funds against an Australian property, while overseas lenders in some markets can require far larger deposits from non-residents (Wise guide for Australians buying property overseas). In practice, that can make an Australian refinance more attractive than waiting on a foreign credit committee.

The trade-off is concentration risk. You are increasing debt against Australian assets to buy an offshore one. That can work well if the foreign purchase is part of a deliberate portfolio plan. It is less appealing if your Australian properties are already heavily geared or you may need local borrowing capacity later.

A local mortgage in the destination country can be the better fit when the market has an established non-resident lending channel, especially in parts of the UK and selected US segments. The main advantages are currency matching and ring-fencing. Rent, loan, and property expenses sit in the same country and often in the same currency. The disadvantages are tighter underwriting, larger deposits, local legal charges, and slower execution.

An international bank or specialist cross-border lender tends to suit high-net-worth borrowers with multi-jurisdiction assets, more complex income, or a need for relationship-based underwriting. This route can be effective for clients with global banking relationships, but it is not automatically cheaper. It often buys flexibility rather than headline rate.

Why Australian equity is often the control point

Many Australian investors expect the overseas property to do the heavy lifting as security. Often it does not. Australian lenders are generally more comfortable taking Australian real estate as collateral than trying to enforce against a property in another country.

That changes how experienced buyers approach the deal. They arrange their capital in Australia first, then negotiate overseas from a stronger position. In a competitive market, that can matter more than shaving a small margin off the interest rate.

It also reduces transaction risk. If the foreign seller expects proof of funds, a local refinance or top-up in Australia can give you clearer purchasing power than an overseas application that is still moving through valuation, compliance, and non-resident credit review.

Before choosing a structure, it helps to compare the broader set of investment property loan options for overseas buyers.

What lenders actually examine

Credit teams do not assess the overseas purchase in isolation. They assess the borrower's full position. That includes Australian debts, overseas liabilities, income type, residency position, and the origin of the deposit.

Deals often stall at this stage. A borrower may have substantial assets and still fail a credit assessment because income is hard to verify across jurisdictions, tax returns do not line up cleanly, or living costs in another country reduce serviceability. Expected rent from the overseas property also does not solve every problem. Lenders give far more weight to proven income and a clear debt picture than to an optimistic rental projection.

For Australian applicants, foreign currency adds another layer. Income earned in pounds, US dollars, or euros may be shaded or converted conservatively. The same applies to foreign liabilities. If you have school fees, rent, or regular spending outside Australia, disclose them early. Hidden commitments are one of the fastest ways to lose time in underwriting.

Market-specific finance reality for Australians

The UK is often the most accessible starting point for Australians because non-resident lending is better established and the legal process is relatively familiar. Accessible does not mean easy. Deposit requirements are usually higher than domestic UK owner-occupier lending, and lenders can be selective about property type, building condition, lease length, and borrower profile. For a market-specific view, the UK mortgage for non residents guide is a useful reference.

The US offers scale and product variety, but finance can be fragmented. Terms differ sharply by state, lender type, and whether the asset is held personally or through an entity. Some Australian buyers assume the US mortgage market is broad enough to absorb any foreign borrower. It is broad, but non-resident underwriting is still document-heavy and often conservative.

Portugal and parts of Europe can work well for cash buyers or low-gearing buyers, but local banking processes may be slower and more administrative than Australians expect. That matters if your strategy depends on speed.

Documents that deserve attention early

Cross-border finance rewards preparation. A clean file gets better engagement from brokers, bankers, and credit teams.

Prioritise these documents first:

Income evidence

Salary, business income, trust distributions, dividends, and tax returns need to reconcile clearly.A full debt schedule

Include Australian mortgages, personal debt, guarantees, margin loans, and offshore liabilities.Source of funds records

If the deposit comes from equity release, sale proceeds, gifts, or a family trust, document the trail early.Residency and tax records

Lenders and lawyers may ask for more than identification. They may want tax residency details, foreign tax numbers, and proof of address across jurisdictions.Entity documents

If you are buying through a company or trust, expect extra KYC and extra time.

To see how borrower expectations differ in practice, this short explainer is useful:

What usually works

Buyers who perform best in cross-border transactions decide the funding route before they choose the property. They also test the downstream effects. Interest cost is only one variable. Currency exposure, Australian deductibility, cash flow pressure, and ATO reporting all sit behind the loan choice.

What usually fails is mixing strategies without a plan. For example, releasing equity in Australia can be efficient, but only if you are comfortable with the loan sitting against Australian property and you have mapped the tax treatment properly. A local overseas mortgage can reduce that linkage, but it may cost more in deposit, time, and compliance.

Good overseas investing from Australia starts with a finance structure you can carry through the full hold period, not just one that gets you to settlement.

Navigating Foreign Ownership Rules and Legal Hurdles

A market can be attractive, liquid, and well located, yet still be a poor fit if the ownership rules are awkward for a foreign buyer. In such situations, enthusiasm tends to outrun legal reality.

Every country draws its own line on what foreigners can buy, how they can buy it, and which approvals, registrations, or tax identifiers they need first. Some systems are open and orderly. Others are technically open but full of procedural friction.

Start with the rulebook, not the brochure

Australian foreign investment rules provide a useful contrast. The ATO notes that certain foreign buyers of Australian residential property must obtain advance approval before purchase, and that Australians buying abroad face the reverse problem. They must work within the foreign country's own investment restrictions, tax residency classifications, and local lending rules (ATO guidance on foreign investment planning).

That inverse burden matters. Australians often underestimate how many moving parts can sit between “offer accepted” and legal ownership overseas.

Open markets and restrictive markets feel very different on the ground

The UK is often perceived as relatively accessible for foreign buyers. Portugal is also frequently considered approachable from an ownership perspective, though the acquisition process may still require local tax registration, banking, and representation. In contrast, some jurisdictions limit ownership by property type, location, land classification, or buyer status.

That difference affects more than legal paperwork. It affects search strategy. In a relatively open market, you can screen assets based on investment quality. In a restrictive market, you first need to know whether you're even allowed to own the exact asset you're considering.

A disciplined buyer asks these legal questions before paying any reservation amount:

- Can a foreign individual buy directly, or is a company structure more practical

- Is the property type unrestricted

- Do you need a local tax number or fiscal representative

- Will a notary, solicitor, or both control the transfer

- Are there rules on holiday letting, licensing, or occupancy

- Can sale proceeds later be repatriated without unnecessary friction

Independent local legal advice isn't a nice extra. It's part of the acquisition cost.

Common legal friction points

The purchase process often slows down because of routine issues rather than dramatic legal disputes.

One buyer may need a local tax number before a bank account can be opened. Another may discover that the apartment is legal to own but awkward to let. Another may learn that the title history is clean, but the building itself has unresolved compliance issues that affect financing or insurance.

A simple comparison helps:

| Issue | Why it matters |

|---|---|

| Local tax ID | Needed for contracts, tax registration, banking, or utility setup in many countries |

| Bank account | Often required for completion funds, direct debits, or landlord operations |

| Property classification | Residential, agricultural, heritage, or tourism-linked categories can carry different rules |

| Letting permissions | A strong yield assumption is worthless if the intended use isn't compliant |

| Legal representation | The right local solicitor can spot title, planning, and contract risks before deposit money is at risk |

What sophisticated buyers do early

They appoint independent local counsel before they appoint anyone else. Not a lawyer recommended solely by the seller. Not a generalist with no foreign-buyer track record. Someone who acts only for the buyer and understands the issues that matter to non-residents.

They also ask for a written summary of the acquisition path before making a binding move. That summary should cover who signs what, when money becomes non-refundable, what registrations are required, and whether the intended holding and letting structure is viable.

That preparation won't make the process glamorous. It will make it investable.

Understanding Your Global Tax Obligations

Tax is where many overseas property strategies stop being as attractive as they looked in the estate agent's window. Gross income is easy to admire. Net after cross-border tax and compliance is what matters.

For an Australian resident, the core issue is straightforward. You may have tax obligations in the country where the property sits, and you may also have Australian reporting obligations on the income and gains connected to that asset. The practical challenge isn't just paying tax. It's understanding which country taxes what first, what relief is available, and how the paperwork aligns.

Why the UK deserves special attention

The UK is one of the most common destinations for Australian buyers, but it's also one of the most misunderstood from a tax perspective.

Non-UK residents are generally taxed on UK property income and gains, with separate non-resident capital gains tax rules for disposals of UK residential property. That means an Australian buyer needs to assess UK rental taxation, UK capital gains treatment, Stamp Duty Land Tax, any non-resident SDLT surcharge rules, letting compliance, and then how the Australia-UK treaty position interacts with the Australian Foreign Income Tax Offset (HSBC overview on financing and tax issues when buying abroad).

That's the point many generic guides miss. “Get tax advice” is true, but incomplete. Essential work involves modelling after-tax cash flow and after-tax exit proceeds before exchange.

How to think about dual tax exposure

A clean way to assess an overseas property is to split the tax analysis into three layers.

Entry taxes

These are the costs tied to acquiring the asset. In the UK, that means understanding SDLT and whether non-resident treatment changes the cost base. In other countries, the equivalent might be transfer taxes, registration taxes, or notarial charges.

These costs affect your true basis in the investment. If you ignore them when calculating expected return, your projected performance starts off distorted.

Ongoing income taxes

Rental income can be attractive in headline terms but far less compelling once local tax, local compliance, management fees, maintenance, and Australian reporting are included.

Many investors should slow down here and ask whether they are buying an income asset or buying complexity disguised as income.

Exit taxes

Selling an overseas property may trigger a local capital gains charge, an Australian tax consequence, or both, depending on your status and the treaty interaction. If you plan to sell within a relatively short holding period, this deserves much more attention than most buyers give it.

A more detailed technical read on this topic is this guide to capital gains tax on foreign property.

Practical tax questions worth asking before you buy

Use a tax adviser who understands both jurisdictions, then push for clear answers to these points:

- How is rental income taxed locally

- What records must be kept in the foreign country and in Australia

- Can local tax paid be credited in Australia

- How are exchange movements treated in your reporting

- What happens on sale if you hold through an individual name, trust, or company

If you want a plain-English primer before speaking with your accountant, this guide to the foreign income tax offset is a useful starting point.

The wrong tax structure can turn a sound property into a mediocre investment without changing the asset at all.

What strong buyers do differently

They underwrite tax before they underwrite upside. They don't treat tax advice as a completion-stage formality. They build it into acquisition screening.

They also recognise that the best market on a pre-tax spreadsheet may not be the best market after all obligations are priced in. That's particularly true in highly regulated landlord markets, where compliance is part of ownership rather than an occasional inconvenience.

The Purchase Process From Offer to Handover

A common mistake looks like this. An Australian buyer agrees to a price on a London flat or a Portuguese apartment, pays a reservation deposit, then discovers the contract terms, funding timetable, and local signing rules do not line up with how Australian deals usually run. At that point, the asset may still be sound, but the process has become expensive.

Execution matters more overseas because the handoff points are different. In the UK, the deal can stay fluid until exchange. In parts of Europe, a preliminary contract can create real financial exposure well before final completion. In the US, title, escrow, inspections, and local disclosure rules can shift the practical timetable even when the headline process looks familiar.

A purchase sequence that protects the buyer

Start with an offer that reflects the local process, not Australian habits. Price is only one term. The offer should also address due diligence, any finance condition that is enforceable in that market, included chattels or fixtures, completion timing, and the deposit structure.

Then build the file quickly. Your local lawyer should review title, zoning or planning issues, seller authority, existing leases, building compliance, and any restrictions on foreign buyers or short-term letting. If the deal depends on Australian equity release, line up the funding path early so the local seller is not waiting on an Australian credit process they do not understand.

A practical sequence usually looks like this:

Offer accepted in principle

Terms are agreed, subject to contract, legal review, and any market-standard conditions.Local due diligence starts

Your lawyer checks title, encumbrances, planning position, body corporate or strata obligations, tenancy status, and contract language.Reservation or preliminary contract stage

This is often where Australians take on risk too early. Deposits may become partly or fully exposed if you withdraw outside the permitted grounds.Funding and transfer arrangements are locked in

Equity drawdown, local lending if relevant, source-of-funds evidence, and foreign exchange transfers should all be matched to the contractual dates.Completion and registration

In some jurisdictions, signing transfers ownership. In others, registration is the legal endpoint and the timing gap matters.

The main discipline is simple. Do not let the seller's timetable force your legal and funding work into the wrong order.

Contract risk usually sits earlier than Australians expect

Australian buyers are used to a clearer separation between offer, contract, and settlement. Overseas, that separation can be much thinner. A reservation agreement in Portugal, a compromise in France, or an exchanged contract in England can change your position fast.

Read the deposit clauses closely. Ask three direct questions before signing anything: when does the deposit become non-refundable, what events let you terminate without loss, and who is holding the money. If the answer to any of those points is unclear, the file is not ready.

I also tell clients to test the practical side of possession. Are there tenants in place, unpaid charges, inherited utility balances, unapproved alterations, furniture disputes, or works promised by the seller after signing. These issues rarely kill a deal. They regularly delay one.

Keep Australian funding aligned with foreign deadlines

The financing point here is not serviceability. That has already been dealt with earlier. The issue during execution is timing.

If you are using equity from an Australian property, the drawdown date, transfer limits, bank verification steps, and FX conversion process all need to match the foreign contract schedule. A lender can approve the facility, yet the transaction can still stall because the money is not where it needs to be on the required day. Sellers and lawyers in overseas markets are usually unsympathetic to delays caused by Australian banking logistics.

Experienced buyers keep liquidity in reserve for this reason. They do not run the deal so tightly that one valuation delay, one compliance query, or one transfer hold puts the deposit at risk.

Treat foreign exchange as part of pricing

Currency is part of acquisition cost, not an afterthought. If the property is priced in US dollars, pounds, or euros and your balance sheet is in Australian dollars, your entry price can move between offer and completion even if the seller never changes terms.

That matters most when deposits are staged. A buyer may secure a good asset and still erode returns through poor conversion timing. Decide in advance how much currency exposure you are willing to carry between exchange and completion, and who is responsible for executing transfers if approvals are needed across entities, trusts, or family offices.

For investors comparing total entry costs across markets, a property stamp duty calculator for overseas purchases is a useful sense-check before funds are committed.

Put the right people around the deal

Overseas property purchases rarely fail because the asset looked attractive. They fail because the buyer used the wrong advisers or used the right advisers too late.

Keep the team lean, but make sure each role is covered:

Local lawyer or notary

Reviews title, contract terms, transfer mechanics, and local legal risk.Australian banker, broker, or mortgage contact

Keeps the equity release or lending side aligned with foreign deadlines.FX provider or private bank relationship manager

Handles conversion, transfer timing, and source-of-funds documentation.Local accountant where pre-completion registration matters

Useful in jurisdictions where tax numbers, VAT issues, or purchase structuring affect completion.Property manager if immediate leasing is planned

Helps verify rent readiness, tenant handover, and compliance items before settlement.

For buyers looking at Southern Europe, Italian tax strategies for HNW investors is a good reminder that process, taxes, and ownership structure often intersect before handover, not after it.

What to confirm before you authorise completion

Before funds are released, confirm the title position is clear, the completion statement matches the contract, transfer taxes and fees are understood, insurance can start on time, and the handover mechanics are documented. Keys, codes, tenancy files, appliance warranties, access credentials, and body corporate records should not be left to assumption.

Good buyers stay patient until the file is clean. Then they move quickly. That balance usually protects more value than negotiating one last discount on price.

Your Post-Purchase Checklist and Exit Strategy

Settlement is not the point where execution risk ends. For an Australian buyer, it often shifts from contract risk to operating risk. I have seen well-bought assets in the UK, USA, and Portugal lose momentum in the first 90 days because the owner assumed rent collection, insurance, utility transfer, tax registration, and reporting would sort themselves out locally. They rarely do.

Distance changes the margin for error. If you live in Sydney or Melbourne and the property sits in Manchester, Orlando, or Lisbon, every weak handover creates delay, extra cost, or both. The post-purchase phase needs the same discipline as the acquisition phase, especially if the deposit came from Australian equity release and the ATO will expect clean records later.

Start by treating the property as an operating business, not a completed transaction.

The first 30 days after completion

A useful post-purchase checklist covers control, income, compliance, and records. Miss one of those and the problem usually shows up in cash flow or tax reporting.

1. Lock down operational control

Confirm who holds keys, alarm codes, building access credentials, mail access, parking permits, and body corporate or HOA logins. Change passwords for any smart locks, cameras, utility portals, and letting platforms. If the property is tenanted, get the full tenant file immediately, including lease, deposit records, condition report, rent ledger, and any maintenance history.

2. Put insurance in force and read the exclusions

Many offshore buyers only check that a policy exists. The better question is whether the cover matches actual use. A vacant apartment, a short-stay unit, and a standard long-term rental often need different cover. In some markets, water damage, storm, flood, liability, and loss-of-rent settings need active selection rather than assumption.

3. Confirm utilities, council rates, owners corporation charges, and local taxes are correctly transferred

This sounds administrative. It affects occupancy, tenant satisfaction, and arrears. A missed utility account can lead to service interruption. A missed owners corporation notice can lead to penalties or missed votes on major works.

4. Complete all local registrations tied to income and ownership

This may include landlord registration, tax identification numbers, rental licensing, short-stay permits, safety certificates, and local revenue registrations. The exact list differs by market, but delay creates predictable problems. Rent may be collected under the wrong entity, expenses may be paid before the tax structure is properly set, and later bookkeeping becomes expensive to fix.

5. Build a document file for both local advisers and your Australian accountant

Store the contract, completion statement, transfer tax receipts, legal invoices, loan documents, insurance schedule, property management agreement, rent statements, repair invoices, foreign tax filings, and bank transfer records. Australians who buy overseas often underestimate how often ATO reporting later depends on documents created at purchase and in the first year of ownership.

Appointing a local manager properly

A local manager can protect yield or drain it. The gap is wide.

Do not appoint based on a low headline fee alone. Cheap management often shows up later as longer vacancy, weak arrears control, poor maintenance supervision, or thin record-keeping. For an Australian owner, reporting quality matters almost as much as leasing ability because your local accountant and Australian tax adviser both need clean information.

Ask direct questions before signing:

- How many properties do you manage in this suburb or building?

- What is your average vacancy period for comparable stock?

- How do you screen tenants, and who approves the final applicant?

- How quickly do you chase rent arrears, and what is the escalation process?

- What maintenance spending can you approve without owner consent?

- Do you use in-house contractors, and how are contractor margins handled?

- How often will you inspect the property, and will you provide written reports with photos?

- What monthly reporting do you provide on rent, costs, and outstanding issues?

- Can you separate capital works from repairs clearly for tax records?

- How do you handle after-hours emergencies?

- What happens if the tenant damages the property or breaks lease early?

- What fees apply beyond the base management fee, including leasing, renewal, inspection, tribunal, or project management fees?

- How do you remit net rent to an overseas owner, and what banking information do you need?

One more test helps. Ask for a sample monthly owner statement and a sample inspection report. You are not buying promises. You are buying process quality.

Set up your cash flow and reporting early

Open the right bank account structure for rent collection and expense payment. In some cases that means a local account in personal name. In others, it may sit under a company or trust structure, depending on legal and tax advice already obtained. The point is control and clean tracing of funds.

Keep private spending away from the property account. If you pay for furniture, travel, repairs, or legal costs from mixed personal accounts, year-end reporting becomes harder than it should be. This matters even more for Australians claiming foreign income and expenses across multiple jurisdictions.

FX discipline matters after purchase as well, not just before settlement. Rental income received in pounds, euros, or US dollars may look fine locally and still disappoint in Australian-dollar terms after conversion. Some clients convert regularly to reduce currency concentration. Others hold foreign income to fund local expenses or future works. Neither approach is automatically right. The right choice depends on loan exposure, spending currency, and how much AUD volatility you are willing to carry.

Plan maintenance before it becomes urgent

Offshore owners pay more for rushed work. That is a pattern, not bad luck.

Within the first few weeks, identify any known maintenance items that can turn into vacancy, insurance, or compliance problems. Water ingress, heating or cooling reliability, electrical defects, roof issues, and building envelope problems deserve early attention. If the asset sits in a strata or HOA scheme, review recent minutes and budgets for signs of upcoming special levies, façade works, lift replacement, or litigation.

For furnished or short-stay assets, check inventory condition against the handover list. Missing items, damaged appliances, and poor presentation affect reviews and occupancy quickly.

Treat the exit as part of the underwriting

Exit strategy starts before the first tenant moves in. A property that is easy to hold but hard to sell is not as attractive as the original spreadsheet suggests.

Australians should assess exit in three layers. First, who is the likely next buyer? Second, what sale costs and taxes will apply locally and in Australia? Third, what does the result look like after converting proceeds back into AUD?

The buyer pool matters more than many offshore buyers expect. A city-fringe apartment in Lisbon may attract international lifestyle buyers in a rising market, but rely more heavily on local pricing discipline in a softer one. A suburban single-family home in the US may appeal mainly to local owner-occupiers. A tenanted flat in a northern UK city may suit yield-focused investors more than emotional lifestyle buyers. Each buyer group values vacancy, lease terms, furnishing, and condition differently.

A practical exit comparison

Take a simple example. An Australian investor owns a well-located overseas apartment and is deciding between two realistic exit paths.

Option A: sell with vacant possession to a local owner-occupier

This can produce a stronger headline price in markets where owner-occupiers pay for presentation, school catchment, lifestyle, or renovation quality. The trade-off is timing. You may need to wait for lease expiry, absorb vacancy, complete cosmetic work, and carry holding costs while marketing.

Option B: sell tenanted to another investor, including overseas buyers

This can shorten the path to sale if the rent is market-aligned and the management history is clean. The trade-off is price ceiling. Investor buyers usually focus on net yield, lease quality, building costs, and tax friction. If the tenant is below market rent or the service charge profile is poor, they price that in quickly.

The better option depends on the market. In practice, I would compare both routes on net proceeds, not gross sale price. That means subtracting agent fees, legal costs, local taxes, vacant holding costs, repair spend, loan break costs if any, and expected FX impact on repatriation. The higher sale price is not always the better result once those items are counted.

Exit checklist for Australian investors

| Exit issue | Why it matters in practice |

|---|---|

| Buyer pool depth | A deep local buyer pool usually means faster sales and better price tension |

| Sale method | Off-market, private treaty, and auction-style processes suit different markets and buyer types |

| Local selling costs | Agent commissions, legal fees, transfer charges, and clearance costs reduce net proceeds |

| Capital gains treatment in the foreign country | The local tax bill changes what you actually repatriate |

| Australian tax treatment | Foreign gains still need to be reconciled properly for ATO purposes |

| Loan discharge and lender approvals | Some lenders, especially where Australian equity release funded the strategy, require coordination before funds are fully freed up |

| Lease status at sale | Vacant or tenanted stock can appeal to very different buyers |

| FX conversion timing | A good local sale can still produce a weak AUD result if currency moves against you |

| Repatriation paperwork | Source-of-funds evidence, settlement statements, and tax documents are often needed by banks and advisers |

Keep reviewing the exit while you hold the asset. If local regulation shifts, tax settings change, short-stay rules tighten, or the buyer pool shrinks, the original hold period may no longer be the best one.

The strongest overseas purchases are easy to operate, easy to evidence to the ATO, and realistic to sell without giving back years of gains in friction. That is the standard worth using.