You're probably looking at two listings right now that seem to tell opposite stories. One sits in a prestigious postcode with a strong asking price and polished marketing. The other is less glamorous, in a market that gets less attention, but the rent looks surprisingly resilient.

That tension sits at the centre of property investing. Price attracts attention, but income reveals quality. If you want to know how to calculate rental yields properly, you need to move past brochure language and reduce each deal to a comparable economic output.

Yield is the first filter because it tells you what the asset is producing relative to what it costs. It won't answer every question about a property, but it will stop you making one of the most common mistakes in global real estate: paying for prestige when the income profile doesn't justify it.

Beyond the Asking Price Why Yield Is Your Key Metric

A property can be expensive and still be mediocre as an investment. It can also look ordinary and perform well because the rent-to-value relationship is stronger. That's why experienced investors start with yield, not aesthetics.

In practical terms, rental yield turns a building into a financial instrument. It helps you compare a flat in a mature city market with a house in a secondary regional market, or a buy-to-let in the UK with an apartment in an emerging economy where pricing and rents behave very differently. The formula itself is simple. The interpretation is where investors make or lose money.

What headline prices hide

Asking price tells you what the seller wants. It doesn't tell you what the asset earns, what it costs to run, or whether the income stream compensates you for risk. That distinction matters most when comparing mature and emerging markets.

In established markets, investors often accept lower yields because they expect stronger legal certainty, deeper tenant demand, better financing access, and lower operational friction. In emerging markets, headline yields may look more attractive, but the investor has to ask a different set of questions about enforcement, vacancy risk, currency exposure, and local market transparency.

Practical rule: Yield is not just a return metric. It's a discipline that forces you to compare income, price, and risk on the same page.

A second trap sits in rent assumptions. Many investors rely on agent guidance without properly validating whether a quoted rent is realistic for that street, unit type, and finish level. A better approach is to study comparable lets before you run the numbers. If you need a practical framework, this guide on how to find rental comps is useful because it focuses on the mechanics of comparing nearby listings rather than relying on broad market averages.

Yield is the start of due diligence

The strongest use of yield is as a screening tool. Gross yield can tell you quickly whether a deal deserves more work. Net yield tells you whether the income survives contact with real operating costs. Beyond that, the metric becomes a way to benchmark one opportunity against another, especially when you're assessing multiple countries or cities at once.

Global investors also need local context. Global Property Guide notes that residential rental yields are calculated using median property prices and rental rates from local listings, and that the dataset is updated biannually in its methodology for yield comparison (Global Property Guide rental yields methodology). That matters because a national average can blur reality on the ground. One district can produce a very different yield profile from the next.

For a broader primer on definitions and market usage, see this explanation of what rental yields are. The key point is simple. Yield lets you see through pricing narratives and judge the income engine underneath the asset.

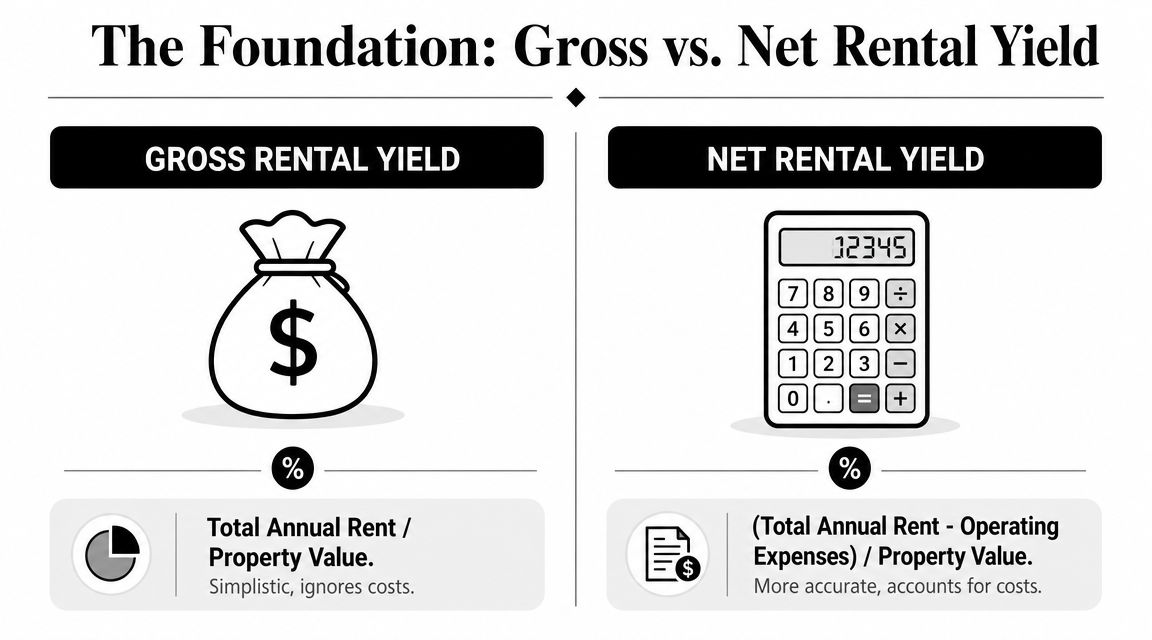

The Foundation Gross vs Net Rental Yield

Most investors learn one formula first and stop there. That's where analysis usually goes wrong. Gross rental yield is useful for speed. Net rental yield is useful for decisions.

Gross yield gives you the first read

In the UK, the basic approach is to convert rent into an annual figure, divide by the property's purchase price or market value, and multiply by 100. Wise summarises the first-pass approach this way: gross rental yield annualises the rent, while net rental yield becomes more decision-useful because it subtracts annual operating costs first (Wise guide to rental yield calculation).

Gross yield is best used when you need to compare several listings quickly. It answers a narrow question: what is this property producing before costs?

A simple expression looks like this:

| Metric | Formula | What it tells you |

|---|---|---|

| Gross rental yield | Annual rent ÷ property price or value × 100 | Income potential before expenses |

| Net rental yield | (Annual rent minus annual expenses) ÷ property price or value × 100 | Income after recurring costs |

Gross yield is helpful because it standardises comparison. But it can flatter a deal that later proves weak once management, repairs, insurance, and other recurring costs start eating into cash flow.

A worked UK example

Westpac provides a clean example that shows why gross yield alone can mislead. A property rented at £450 per week produces £23,400 a year when annualised as £450 × 52. On a £600,000 purchase price, that works out to a 3.9% gross yield. After £4,920 in annual costs, the yield falls to 3.1% net (Westpac rental yield example).

That change is the key lesson. The property didn't become worse overnight. The gross figure wasn't telling the full story.

Gross yield helps you shortlist. Net yield helps you decide.

Why net yield matters more

Net yield is closer to economic reality because it tests the durability of the income stream. If a property only looks compelling before costs, it isn't really compelling.

This is especially important in markets where headline rents appear strong but the running costs are heavier than expected. A building with service charges, older systems, intensive maintenance needs, or full-service management can look perfectly acceptable on gross yield and much less attractive on a net basis.

When investors ask how to calculate rental yields, what they usually mean is this: how do I avoid fooling myself? The answer is to calculate gross yield first, then move immediately to net yield with realistic expense assumptions.

If you want to model both approaches quickly, a rental yield calculator is useful for testing scenarios. The calculator isn't the analysis. It's the tool that helps you pressure-test your assumptions.

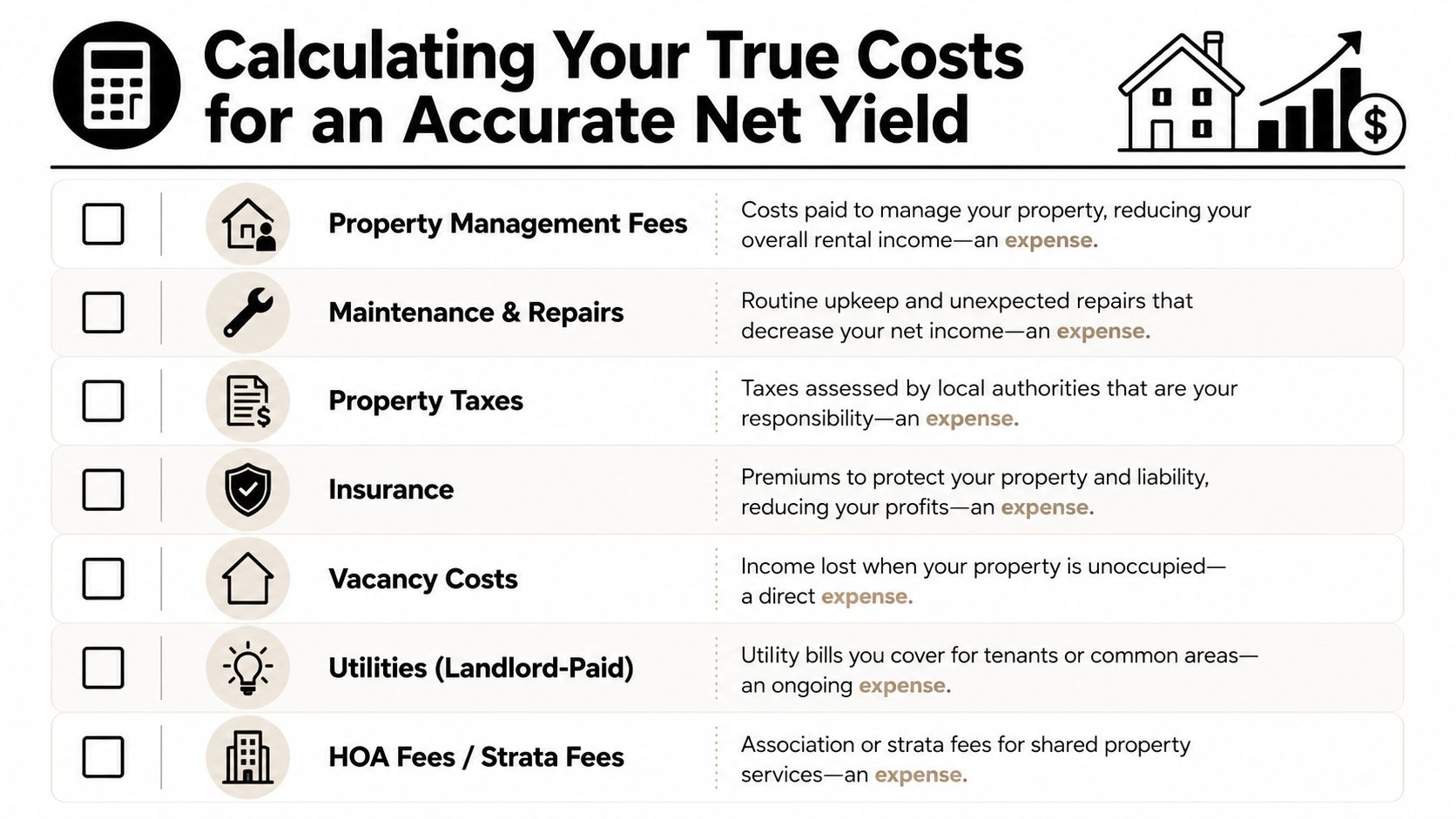

Calculating Your True Costs for an Accurate Net Yield

At this stage, many deals fall apart. The formula for net yield is straightforward, but the expense line is where optimism usually creeps in.

A robust underwriting model starts by annualising rent as weekly rent × 52 or monthly rent × 12, then deducting recurring costs. Industry guidance commonly places management fees at about 5%–8% of rent, which is one reason so many self-prepared yield models come out too high when investors forget to include professional management (Duplex Building Design rental yield guide).

The costs investors most often miss

Some expenses are obvious. Others are intermittent, irregular, or easy to underestimate. All of them matter if your goal is a credible net yield.

Management fees

Even if you plan to self-manage today, a serious model should ask what the property looks like under outsourced management. That gives you a cleaner comparison across geographies and makes your underwriting less dependent on your own time.Maintenance and repairs

Repairs don't arrive smoothly. A property may run smoothly for months, then require several interventions at once. Investors who only budget for routine wear and tear often miss the effect that ageing systems, communal areas, or tenant turnover can have on annual cash flow.Insurance

Insurance isn't optional friction. It's part of the operating base of the asset. Premiums can also vary materially depending on building type, claims history, and local risk conditions.

Before you go further, this video gives a useful visual walkthrough of the mindset behind separating rent from real ownership costs:

The market-specific items that distort comparisons

Cross-border investors often compare properties using a single template and miss local charges that don't travel neatly from one market to another.

Service charges and building fees

Flats, managed blocks, and amenity-heavy developments can carry meaningful recurring costs. These should never sit outside your net yield model.Ground rent, association dues, or strata-style charges

The legal label varies by country, but the investment effect is the same. These costs reduce distributable income.Property taxes

Tax treatment differs sharply by jurisdiction. In the United States, for example, local tax assessments can become a major underwriting variable, which is why investors sometimes need practical guidance on understanding property tax appeals in Texas before they finalise assumptions for a deal.

Underwriting gets stronger when every recurring cost is treated as inevitable rather than exceptional.

Build a model that survives reality

A serious investor doesn't just ask, “What rent can I charge?” They ask, “What income is left after the property behaves like a real asset?”

That means including void periods, leasing costs, landlord-paid utilities where relevant, and any recurring compliance or licensing expense that attaches to the property. In mature markets, these costs are usually easier to identify but still easy to underweight. In emerging markets, the opposite problem often appears. The structure may look simple, but actual collection, maintenance coordination, and legal enforcement can be more operationally intensive than the spreadsheet suggests.

Transaction costs matter too, especially at acquisition. They don't usually belong in a standard net yield figure, but they do matter for return-on-cash analysis and total investment performance. If you're buying in the UK, a stamp duty calculator on property purchases helps place those upfront costs in the wider return picture.

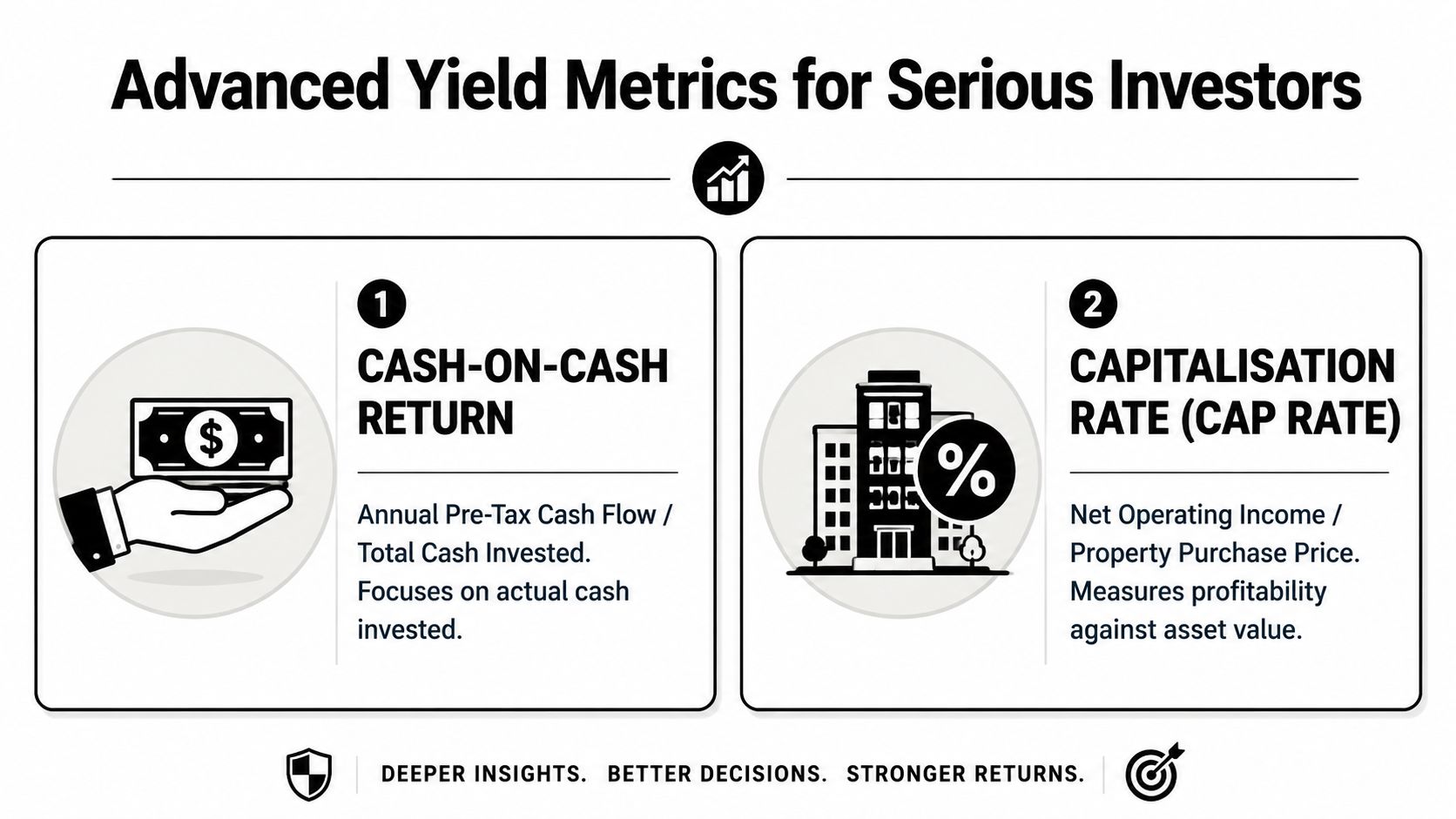

Advanced Yield Metrics for Serious Investors

Net yield is strong, but it isn't enough on its own. Professional investors usually add two more lenses: cash-on-cash return and capitalisation rate, often shortened to cap rate.

Each metric answers a different question. Net yield asks whether the asset produces income efficiently after operating costs. Cash-on-cash return asks whether your actual cash investment is working hard enough. Cap rate asks how the property performs before financing enters the picture.

Cash-on-cash return measures your money, not just the property

Cash-on-cash return becomes essential when debt is involved. Two investors can buy similar assets and record similar net yields, but their outcomes may differ sharply because one used substantial equity and the other financed with debt.

The formula is conceptually simple:

| Metric | Core idea | Best use |

|---|---|---|

| Cash-on-cash return | Annual pre-tax cash flow divided by total cash invested | Comparing financed deals |

| Cap rate | Net operating income divided by purchase price or value | Comparing assets without financing noise |

If you're investing in a market where mortgages are expensive, restricted, or unavailable to foreign buyers, cash-on-cash return may look very different from your debt-free property yield. In other words, a decent asset can become a weak personal investment if the financing stack is inefficient.

This is why serious investors separate asset quality from capital structure. The building may be acceptable. Your financing may not be.

Cap rate strips out financing so you can compare assets cleanly

Cap rate is especially useful when you need a neutral comparison across similar income-producing properties. It focuses on the operating income of the asset relative to price or value, without the distortions created by personal borrowing decisions.

That matters when comparing one block to another, one city to another, or one market cycle to another. If you only use cash-on-cash return, you can confuse a favourable debt structure with a strong property. Cap rate helps correct that.

A good investment process asks two separate questions. Is the asset efficient? And is my capital deployed efficiently?

Use the metrics together, not in competition

These measures aren't substitutes. They are layers.

A practical sequence often looks like this:

- Start with gross yield to eliminate listings that don't justify deeper work.

- Move to net yield to understand recurring profitability.

- Apply cap rate thinking when comparing similar assets or markets independent of debt financing.

- Finish with cash-on-cash return to judge whether the deal still works once purchase costs, debt terms, and equity requirements are included.

This layered approach is particularly valuable across borders. A mature market may produce modest property-level income efficiency but still suit a conservative portfolio because the legal, financing, and resale conditions are stronger. An emerging market may show more attractive income on paper, yet your personal return may weaken once operational friction and limited financing are factored in.

For a deeper look at market-level asset comparison, this guide to rate of capitalisation in property investing helps place cap rate in context. The important point is that no single metric deserves total authority. Serious investors triangulate.

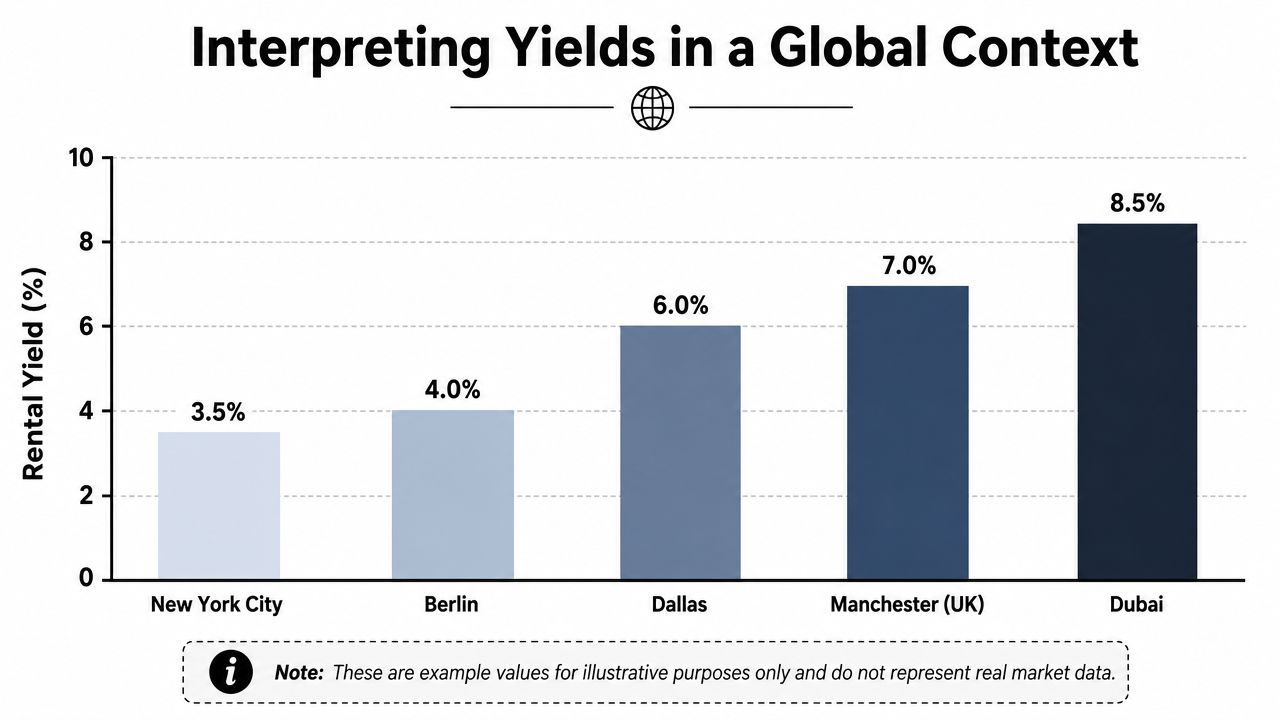

Interpreting Yields in a Global Context

A yield figure only becomes meaningful when you place it inside a market. The same percentage can signal stability in one country, overpricing in another, and high risk in a third.

That's why experienced investors don't ask whether a yield is “good” in isolation. They ask whether it is attractive for that market, at that point in the cycle, with that level of legal and operational risk.

Mature markets and emerging markets don't reward investors the same way

In established markets, lower yields can still make sense if the investor is buying transparency, liquidity, financing depth, and predictable tenant demand. Those markets often suit investors who value resilience and lower operational variance more than maximum current income.

Emerging markets can look more generous on yield, but that premium usually exists for a reason. The investor may be taking on more uncertainty around valuation, legal process, currency, title clarity, taxation, rent collection, or resale execution.

A useful comparison looks like this:

| Market type | Typical investor attraction | Common trade-off |

|---|---|---|

| Established market | Legal clarity, financing access, deeper comparables | Lower running yield |

| Emerging market | Higher income potential, lower entry pricing in some areas | Higher execution and governance risk |

This is why yield should never be read as a universal score. It is a market-specific signal.

Purchase price versus current market value

One of the most important interpretation questions is whether to calculate yield on the original purchase price or the current market value. Both can be valid, but they answer different questions.

Yield on purchase price tells you how the asset performs relative to the capital you originally committed. Long-term owners often care about this because it shows how efficiently their initial basis is working today.

Yield on current market value asks a sharper portfolio question: if this property were cash today, would you still choose to hold it? That makes it the more useful figure for capital allocation decisions.

Wall Street Prep notes the importance of this distinction and highlights current UK conditions that sharpen it. The Office for National Statistics reported that average private rents rose 9.0% year on year in England in the 12 months to May 2026, while the UK House Price Index showed annual house price growth of 2.8% in March 2026, creating a wider rent-to-price gap that can make purchase-price yields and current-value yields diverge materially (Wall Street Prep on rental yield and UK rent-price divergence).

If rents rise faster than property values, long-held assets can look far better on original cost than on current market value. That doesn't make either figure wrong. It means they answer different strategic questions.

What the comparison really tells you

In a mature market, compressed yields may still be acceptable if you expect steadier tenancy, easier debt, and lower friction. In an emerging market, a stronger yield may be justified only if the premium is large enough to compensate for additional uncertainty.

That's where market benchmarks become useful. You need local rent evidence, realistic expenses, and a current view of values in that city or submarket. Without that, yield becomes a false precision exercise.

If you're benchmarking opportunities internationally, a country-level view of rental yield by country can help frame what is normal before you assess any one property in detail. The point isn't to chase the highest number. It's to understand what the number is paying you for.

From Calculation to Confident Investment Decisions

The best investors don't treat yield as a verdict. They treat it as a toolkit.

Gross yield helps you discard weak listings quickly. Net yield shows whether the income holds up after the property starts incurring real costs. Cash-on-cash return tells you whether your equity is being used well. Cap rate helps you compare properties without letting financing structure distort the picture.

A disciplined way to use the numbers

A practical decision process usually looks less glamorous than people expect:

- Screen for economic logic using gross yield.

- Stress-test operating reality with net yield and a cost model that includes the expenses investors prefer to ignore.

- Judge asset quality separately from financing by comparing cap rate and cash-on-cash return.

- Recheck the market context before you conclude that a higher yield is automatically better.

That final step matters most. A stronger yield can reflect efficiency, but it can also reflect hidden fragility. A lower yield can reflect overpricing, but it can also reflect legal certainty and durable demand. The number only becomes useful when you connect it to market structure, tenant depth, taxation, and your own investment horizon.

The real objective

Most mistakes in property investing come from mixing signals. Investors confuse rent with profit, price with value, and headline yield with durable return. Once you calculate each metric properly, the fog clears.

If you want to sharpen that decision process further, resources on understanding investment property data can help you think more systematically about how local rent evidence, market fundamentals, and operating assumptions fit together. Better property decisions usually come from better data discipline, not from more optimism.

A strong portfolio doesn't come from buying the property with the best story. It comes from buying the asset whose numbers still make sense after you've challenged them from every angle.

World Property Investor helps you compare markets, analyse rental yields, and research property opportunities across major global destinations. If you want practical country guides, city-level investment analysis, and tools for smarter cross-border buying, visit World Property Investor.