A lot of investors look at Cyprus the same way they look at any attractive international market. They see lifestyle, straightforward ownership, strong expat demand, and the possibility of combining a personal move with an income-producing asset. Then they ask the right question a bit too late: what's left after tax?

That question matters more in Cyprus than many buyers realise. Two investors can own similar properties, collect similar rent, and still end up with very different net returns because their tax residency, domicile status, and wider income mix aren't the same. A salaried resident, a non-resident landlord, and a Cyprus tax resident who qualifies as non-domiciled are not playing the same game.

That's why income tax in Cyprus needs to be approached as a planning exercise, not a checklist. If you understand which income falls into the progressive bands, which income may sit outside the main pain points, and where cross-border structuring starts to create risk rather than value, Cyprus can work very well. If you get those basics wrong, the headline appeal won't save the deal.

Why Cyprus Tax Rules Matter for Your Investment Returns

A typical Cyprus buyer today isn't only buying a flat in Limassol or a holiday let near Paphos. They're often buying a tax position as well. That buyer may still have UK dividends, a pension, freelance income, or overseas rent. In practice, the property becomes one part of a wider income picture.

That's where investors often misjudge Cyprus. They focus on purchase price, tenant demand, and gross yield, then treat tax as an admin issue. It isn't. Tax determines your real cash flow, your workable ownership structure, and whether relocating to Cyprus completely improves your position or merely moves the compliance burden.

The difference between gross return and usable return

For a property investor, the useful question isn't “what's the tax rate?” It's “which of my income streams are exposed to it?” Cyprus uses progressive personal taxation for certain income, but the result depends heavily on whether you remain non-resident, become tax resident, or move and qualify under the non-dom framework discussed later.

An investor comparing Cyprus with Dubai, Portugal, or Greece should also remember that tax systems are moving targets. If you're weighing Cyprus against the evolving UAE corporate tax environment, the lesson is the same in both places: headline branding around “low tax” is less useful than understanding what gets taxed, where, and under which status.

Good international tax planning starts with cash flow mapping. List every income source first, then apply local rules. Doing it the other way round leads to expensive assumptions.

A buyer living in London with one Cyprus rental property has a very different analysis from a buyer moving to Cyprus and drawing salary, pension, and portfolio income. If you're still assessing how foreign rent fits into your overall planning, this guide to overseas rental income is a useful starting point before you model Cyprus specifically.

What usually works and what usually fails

What works is simple. Investors who map residency early, separate labour income from passive income, and document their cross-border position tend to keep Cyprus efficient and manageable.

What fails is equally familiar:

- Buying first, structuring later. That often leaves the property in the wrong name or the wrong tax footprint.

- Assuming residency equals advantage. In Cyprus, residency can be helpful, but only when it aligns with domicile status and the type of income you receive.

- Ignoring non-property income. Salary, dividends, interest, and pensions often shape the outcome more than the rent itself.

Establishing Your Cyprus Tax Residency and Domicile

Before you calculate any liability, you need to know who Cyprus treats you as. Most mistakes happen here. Investors jump straight to rates and allowances without pinning down status.

Tax residency and domicile are linked, but they aren't the same thing. Residency is about where you meet the legal tests for tax residence. Domicile is a separate concept that becomes central if you want to access the main Cyprus non-dom advantages.

The residency question first

In practice, investors usually assess Cyprus tax residence through the established day-count tests used in planning. One is the simpler full-year residence route. The other is the shorter-stay route that can work for internationally mobile individuals with stronger factual ties to Cyprus.

If you're relocating through an investment and residence strategy, the property and immigration side often runs alongside tax planning. This overview of the Cyprus Golden Visa is useful for the residence angle, but the tax answer still depends on your actual residence pattern and supporting facts.

A practical way to handle this is to document:

- Your physical presence. Keep clean travel records, not rough estimates.

- Your centre of life. Where do you live, work, and manage day-to-day affairs?

- Your conflicting tax exposures. If another country may also claim residence, treaty analysis becomes important.

Why domicile is the real pivot

Many investors assume that once they become Cyprus tax resident, the best parts of the regime follow automatically. They don't. The central question is whether you're also treated as non-domiciled for Cyprus purposes.

That matters because domicile drives the treatment of certain passive income streams under the Cyprus framework. For an investor with portfolio income, retained savings, or a pension from abroad, domicile can matter as much as residence itself.

Practical rule: Don't ask “am I moving to Cyprus?” Ask “what exact status will Cyprus give me once I move?”

A common investor mistake

A UK national relocates, rents or buys a home in Cyprus, spends enough time there, and assumes the tax planning is finished. It isn't. You still need to determine whether Cyprus taxes you as a resident on broader income sources and whether your domicile position preserves the more favourable treatment that attracts many expats in the first place.

Paperwork matters in this context. Passport stamps, tenancy documents, employment contracts, proof of where companies are managed, and evidence of where your family and financial life are based all become relevant. Cyprus planning works best when the facts are boring and consistent.

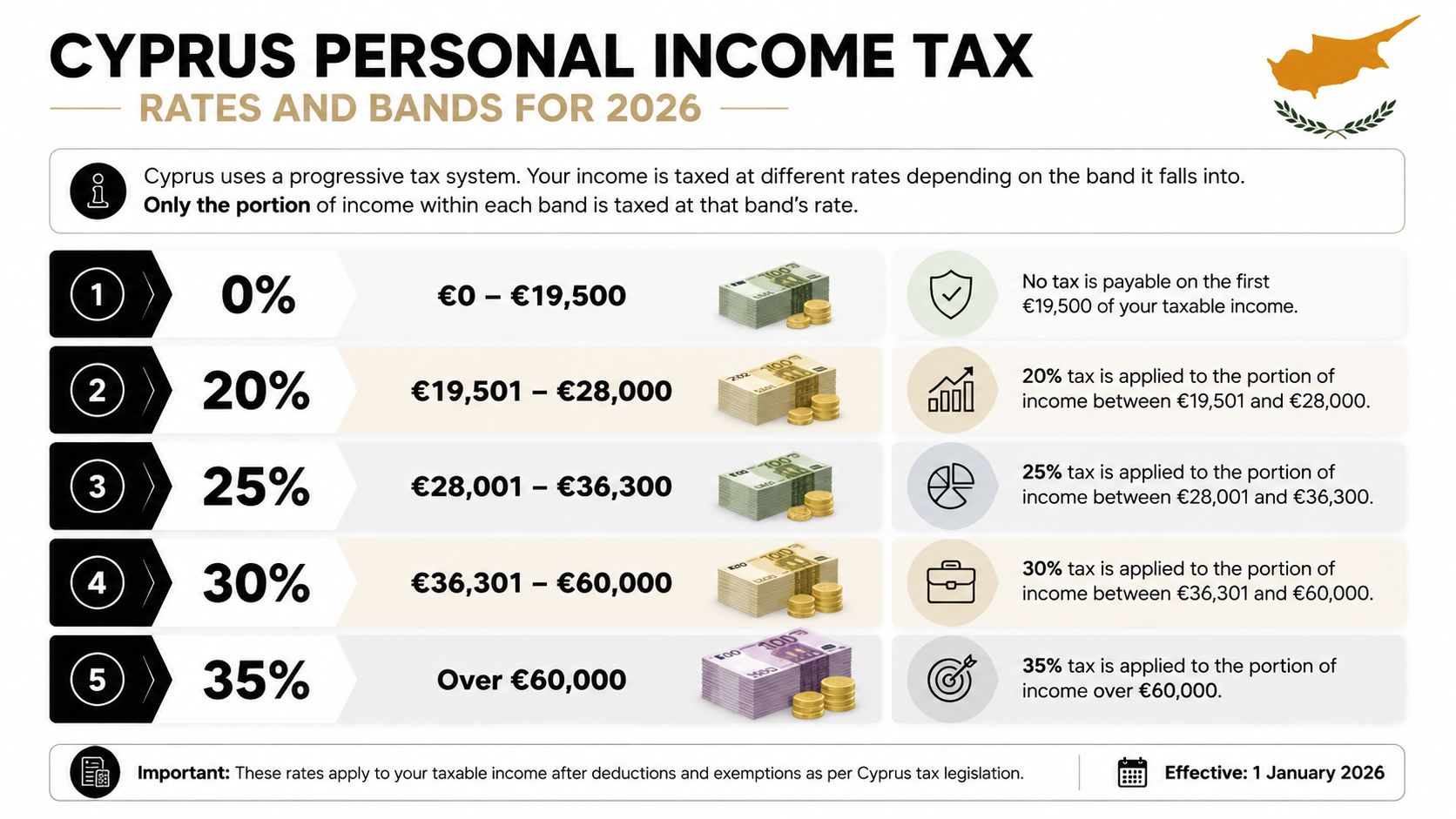

Cyprus Personal Income Tax Rates and Bands in 2026

A property investor moves to Cyprus, keeps a portfolio abroad, earns local rental income, and draws some director fees from a company. The first mistake is to look only at the top rate. The fundamental question is which parts of that income fall into the personal income tax bands, and which do not.

For income that sits inside the personal tax net, Cyprus uses a progressive scale. That matters for salary, director fees, trading income, and some property-related income received personally. Analysts at Trading Economics show Cyprus has kept a top marginal personal income tax rate of 35% for many years and project 35.00% again in 2026 (Trading Economics on Cyprus personal income tax). Stability helps planning. It gives investors a tax system they can model with some confidence, even if Cyprus is clearly not in the camp of countries with no personal income tax.

The 2026 band structure investors should watch

The current 2026 framework is widely reported as follows:

- 0% on income up to €22,000

- 20% on €22,001 to €32,000

- 25% on €32,001 to €42,000

- 30% on €42,001 to €72,000

- 35% above €72,001

The practical effect is straightforward. Someone earning moderate active income in Cyprus keeps more before reaching the higher bands. Someone with much higher earned income still ends up at 35% on the top slice, but only after a larger portion has been taxed at lower rates.

For investors, that changes the maths in a few specific situations.

- Relocated professionals earning a Cyprus salary usually feel the benefit first.

- Owner-managers taking director remuneration may have more room to manage how much income is exposed to the upper bands in a given year.

- Property investors holding rentals personally need to add taxable rental profit to their wider income picture, rather than reviewing property income in isolation.

A short explainer is worth watching before you run your own figures:

Why sophisticated investors look past the headline rate

The 35% headline rate gets attention because it is easy to quote. In practice, investors need to separate earned income from passive income, then test each stream against residence, source, and domicile treatment. That is where the actual liability is determined.

A client with €60,000 of salary and €20,000 of rental profit has a very different Cyprus tax profile from a client with €20,000 of salary and €60,000 of dividends and interest. On paper, both have €80,000 coming in. In the tax return, they do not look the same.

That distinction matters for returns. If most of your cash flow comes from active earnings, the income tax bands deserve close attention because more of your annual income may be exposed to progressive rates. If your wealth is driven mainly by investment income, the band structure still matters, but often less than investors expect. The tax cost then depends more heavily on how each income stream is classified and whether your Cyprus status gives access to better treatment elsewhere in the regime.

The Non-Domicile Regime A Game Changer for Investors

For many internationally mobile investors, this is the part of Cyprus that changes the whole analysis. The value isn't just in where the personal bands sit. It's in the fact that a Cyprus tax resident who remains non-domiciled may access materially better treatment for certain passive income.

That's why income tax in Cyprus can look ordinary if you review only salary bands, but much more compelling once you layer in domicile status. For property investors with broad portfolios, that distinction often determines whether Cyprus works as a serious base or merely a lifestyle choice.

Where the regime becomes powerful

The BBC InCorp summary notes that for UK nationals who become Cyprus tax residents but remain non-domiciled, dividends and most interest can be exempt from the Special Defence Contribution, while foreign pensions can be taxed at a flat 5% on amounts over €3,420 (BBC InCorp on Cyprus income tax).

That matters because many expats don't live on one income source. They may have:

- A local or overseas salary

- UK or international dividends

- Interest from cash or fixed-income holdings

- Rental receipts from property

- A pension from abroad

Those streams don't all behave the same way. Investors who understand that early can avoid poor decisions, especially the common mistake of assuming all income is funnelled through one standard rate table.

The real investor use case

A pure landlord with modest rental income may find Cyprus attractive, but a landlord with dividends and pension income often finds it much more attractive. That's because the non-dom position can soften the tax impact on passive wealth while the property itself remains one part of the plan.

This is also why Cyprus often appears on lists of countries with no personal income tax, even though that label is technically too broad for serious planning. Cyprus does have personal income tax. What many investors really mean is that some categories of passive income can be treated very favourably if the individual has the right residence and domicile profile.

The best Cyprus outcomes usually come from mixed-income households, not from trying to force every activity through a single company or a single tax theory.

What works and what doesn't

What works is using Cyprus for the kind of income it handles well. Dividends, most interest, and foreign pension planning can all be relevant, provided the facts support non-dom treatment and the income is analysed correctly.

What usually doesn't work is overcomplicating the structure. Investors sometimes arrive with offshore companies, nominee arrangements, or layered holdings built for a different jurisdiction. Those structures often create cost and scrutiny without improving the Cyprus result.

A cleaner approach is often better:

- Hold the property where ownership is commercially sensible.

- Separate personal residence planning from corporate structuring.

- Treat pensions, dividends, and rent as distinct categories.

- Review the home-country consequences before assuming Cyprus gives the final answer.

The trade-off sophisticated investors should accept

Cyprus can be tax-efficient, but it isn't frictionless. You still need evidence of genuine tax residence. You still need consistency across immigration, tax filings, banking, and practical life. And if you're moving from the UK or another high-compliance jurisdiction, you need both sides of the move to agree with the narrative.

That's the core advantage of Cyprus. Not a gimmick. A coherent legal framework that can work very well for the right investor, especially one living on more than salary alone.

Tax on Rental Income and Property Sales

For a property investor, theory meets the bank account here. Rent is the income stream most buyers underwrite, so the tax treatment needs to be understood in operational terms, not just as a line in a brochure.

The key practical distinction from earlier is residence. PwC's 2025 guide, as cited in the verified material, states that tax resident individuals are taxed on chargeable income from all sources in Cyprus and abroad, while non-residents are taxed only on certain Cyprus-source income. That resident versus non-resident divide is the starting point for rental analysis.

How to think about Cyprus rental income

If you receive rent from Cyprus property, the immediate question isn't just the rate. It's whether that rent forms part of a wider personal tax base in Cyprus because you are resident, or whether Cyprus is taxing you only on local-source income because you are not.

For property investors, that distinction affects planning in three ways:

- A resident investor may need to think about worldwide income interactions, not just local rent.

- A non-resident owner is usually analysing Cyprus-source property income more narrowly.

- A resident non-dom investor may still find that rental income and passive portfolio income are treated very differently.

Tax treatment of rental income by residency status

| Status | Tax on Rental Income | Tax on Dividend/Interest Income | Key Consideration |

|---|---|---|---|

| Cyprus tax resident | Falls within the personal tax framework on chargeable income, alongside other relevant income streams | Depends on whether the person is domiciled or non-domiciled and on the character of the income | Worldwide position matters, not just the property |

| Cyprus tax resident and non-domiciled | Rental income still needs separate analysis within the personal tax system | Dividends and most interest may benefit from the non-dom SDC exemption discussed earlier | Mixed-income planning is where Cyprus is strongest |

| Non-resident | Cyprus generally taxes certain Cyprus-source income only | Overseas dividend and interest income is outside the usual Cyprus resident analysis | The focus is local-source exposure and treaty interaction |

Rental income is rarely the hardest part. The hard part is how it interacts with everything else you earn.

Property sales and record-keeping

A rental strategy also needs an exit plan. The income tax position on rent is not the same thing as the tax treatment on a sale. Property disposals, VAT on relevant acquisitions, and transaction structuring need separate advice because they sit in a different part of the tax analysis.

That separation matters in practice. I often see investors model the purchase and rent correctly, then leave the sale assumption dangerously vague. If you want a realistic view of lifetime return, your tax review has to cover acquisition, holding period income, and eventual disposal.

For investors who own property across several markets, record-keeping becomes its own risk factor. If you're trying to reconcile historic tax charges and property records in the US context, tools that can fetch property tax history from Zillow can help standardise due diligence. The same principle applies in Cyprus. Clean records support clean tax outcomes.

If you're still at the acquisition stage, this guide to investment property in Cyprus is a practical companion to the tax analysis.

Worked Examples and Practical Tax Planning

A landlord moves to Cyprus in September, keeps a consulting salary, receives overseas dividends, and collects rent from one apartment in Limassol. Another investor stays non-resident and owns the same type of property through the same year. The property income may look similar on paper, but their Cyprus tax exposure can end up very different once residency, non-dom status, and the mix of income streams are tested together.

As noted earlier, the 2026 rate changes improve the position for many mid-income taxpayers. For investors, that matters less in isolation than people expect. What drives the outcome is how employment income, pensions, rent, dividends, and interest sit beside each other in the same tax year.

Example one with salary and portfolio income

A UK national relocates to Cyprus, becomes tax resident, qualifies as non-domiciled, and earns a Cyprus salary. They also receive overseas dividends and bank interest.

The salary sits inside the progressive income tax system. The investment income needs separate treatment. In many cases, that is where the value of Cyprus residence is felt, because passive income and earned income do not always produce the same Cyprus result.

I tell clients to model this in cash terms, not just headline rates. If salary covers living costs and the portfolio funds wealth accumulation, non-dom status can materially improve after-tax retention. If the household relies mainly on employment income, Cyprus may still work well, but the tax advantage is usually less dramatic than marketing brochures suggest.

Example two with pension and rent

A retired investor moves to Cyprus and keeps two main income streams. A foreign pension and rent from a Cyprus apartment.

Foreign pensions may qualify for the special Cyprus option under which amounts above a low threshold are taxed at 5%, if the taxpayer elects that treatment and the conditions are met. The rental income does not automatically follow the pension result. It must be reviewed under the ordinary rules that apply to property income.

Planning often goes wrong in practice for this reason. Retirees see one favourable pension rule and assume the rest of their income follows the same pattern. It does not. Pension elections, rental profit calculations, and property exit planning each need their own file, their own assumptions, and their own evidence.

A good Cyprus tax file separates each income stream from the start. Pension documents in one folder, tenancy records in another, and investment statements in a third.

If that investor may also dispose of property outside Cyprus, the wider picture matters. A sale can trigger tax where the property is located even if Cyprus residence changes the investor's personal tax profile. This guide to capital gains tax on foreign property is a useful reference point when modelling the full return.

Example three with a non-resident landlord

A non-resident investor owns one Cyprus rental property, lives abroad full-time, and earns everything else outside Cyprus.

This is usually narrower from a Cyprus income tax perspective. The analysis tends to centre on Cyprus-source rental income, local compliance, and whether the home country also taxes the same profit. Narrower does not mean easier. Cross-border filing errors are common because the investor treats the Cyprus property as a side issue while the home jurisdiction treats it as part of the worldwide income picture.

Admin discipline has a direct financial effect here. Missing invoices, weak expense support, and inconsistent tenancy records make it harder to defend the profit calculation in either country. If you want to reduce administrative burdens for landlords, using tools for rent tracking, maintenance logs, and document storage can make cross-border compliance much easier.

What these examples show

Cyprus tax planning works best when each income stream is tested separately and then brought back into one model. That sounds obvious, but many investors still do the reverse. They pick a residency narrative first and only later ask how rent, salary, pensions, and investment income interact.

The practical steps are usually simple:

- Classify each income stream correctly before choosing a structure or making a move.

- Match ownership to the investment plan rather than copying a structure that worked for someone in a different country.

- Document residence and non-dom status early if you have recently relocated.

- Run both jurisdictions together when another country may still tax the same income or gain.

Good Cyprus planning is rarely about finding one favourable rule. It is about combining the right status with the right income mix, then keeping records strong enough to support that position if either tax authority asks questions.

Compliance Filing Deadlines and Double Tax Treaties

Once the structure is sensible, the next priority is compliance. Investors often lose more money through poor administration than through tax rates themselves. Late registration, inconsistent filings, and weak supporting records are what turn a manageable profile into a difficult one.

The practical rule is simple. Register promptly, keep records that match your tax narrative, and don't assume your accountant can fix contradictory facts after the year has closed.

What to keep under control

Your Cyprus compliance file should cover at least these points:

- Residency evidence such as travel logs and proof of presence.

- Income support including tenancy agreements, dividend statements, pension records, and payroll documents.

- Ownership documents for every asset producing Cyprus-source income.

- Cross-border analysis if another jurisdiction may still tax the same income.

If you also expect to sell property abroad, it helps to understand how the home-country side may tax that disposal. This guide to capital gains tax on foreign property is useful context when you're aligning Cyprus planning with an overseas exit.

Why treaties matter

Double tax treaties are often what stop a good Cyprus move becoming a bad cross-border mess. They help allocate taxing rights and reduce the risk that two countries both claim the same income without relief. For UK-linked investors, treaty review is usually essential if salary, rent, pensions, or dividends continue to touch both jurisdictions.

Treaties don't replace domestic tax law. They sit on top of it. That means you still need the basic Cyprus analysis right before treaty protection becomes useful.

New anti-avoidance pressure from 2026

The compliance picture is also tightening at the international level. Chase Buchanan notes that from 1 January 2026, Cyprus will apply new rules for payments to companies in low-tax jurisdictions, including potential withholding taxes on dividends, interest, and royalties to entities in blacklisted jurisdictions (Chase Buchanan on Cyprus expat tax changes).

For property investors, the message is clear. If your holding structure relies on aggressive cross-border routing, Cyprus is becoming less forgiving. Straightforward ownership and well-supported commercial arrangements are more resilient than clever paper structures.

Keep the story simple enough that your tax return, bank records, company documents, and day-to-day reality all say the same thing.

If you're comparing Cyprus with other international property markets, World Property Investor publishes detailed country guides, tax explainers, and market comparisons that help you assess returns, risks, and ownership structures before you buy.