For many, life in Portugal conjures images of sun-drenched beaches and historic cities. For the global property investor, it represents something far more tangible: a stable, high-quality European market where solid financial returns and an exceptional lifestyle converge.

This rare combination has elevated Portugal from a popular holiday destination to a serious contender for international capital. It offers an affordable entry point into the EU property market without compromising on the fundamentals that protect long-term wealth.

Your Executive Briefing on Portugal

Why has this Iberian nation captured the attention of investors worldwide? The answer lies beyond headline-grabbing visa schemes and into the fundamentals that create a secure environment for capital growth.

Years of steady public investment in infrastructure, combined with a stable political landscape, have built a foundation of trust. For any investor seeking to acquire overseas assets, such predictability is paramount. It provides the necessary backdrop for long-term growth strategies, rather than short-term speculation.

The market fundamentals are only half the story. The other key driver is Portugal’s exceptional quality of life, which directly fuels residential and rental demand. Three factors are critical for investors to understand:

- Exceptional Safety: Portugal consistently ranks as one of the safest countries globally, according to various international indices. This is a significant draw for the expats, retirees, and families who constitute a reliable, high-quality tenant base.

- Affordable Healthcare: The country’s public and private healthcare systems are significantly more affordable than those in the UK or North America. This is a key decision-making factor for long-term residents.

- A Year-Round Climate: With over 300 days of sunshine annually in regions like the Algarve, the climate supports a robust, year-round rental market, particularly for short-term lets which are not confined to summer months.

This powerful mix of affordability, safety, and lifestyle makes the country a magnet for a growing global community. As more professionals and retirees make Portugal their home, they create sustained demand for high-quality rental properties, underpinning both rental income and future capital appreciation.

For an investor, the true value of life in Portugal lies in its dual appeal. It is a jurisdiction where one can secure assets that generate reliable returns while also offering a personal destination that enhances one's own quality of life.

Understanding these dynamics is the first step for any investor evaluating opportunities in this market. To put this into context, we have summarised the key metrics below.

Portugal at a Glance for Property Investors

This table consolidates the key metrics and lifestyle factors critical for evaluating life in Portugal from an investment perspective.

| Metric | Data/Insight | Relevance for Investors |

|---|---|---|

| Quality of Life | High safety, excellent climate, strong healthcare. | Drives demand from high-quality tenants (expats, retirees, digital nomads). |

| Cost of Living | 15-25% lower than other Western European hubs. | Makes the country attractive for long-term residents, supporting stable rental demand. |

| Economic Stability | Stable GDP growth and a secure political environment. | Reduces market volatility and provides a secure backdrop for capital appreciation. |

| Rental Yields | Gross yields average 4-7% in prime urban and coastal areas. | Offers solid returns compared to many mature European markets. |

| Tourism Sector | Over 25 million international tourists annually (pre-pandemic figures). | Fuels a strong and profitable short-term and holiday let market. |

| Expat Community | Growing rapidly, with a large presence from the UK, US, and EU. | Creates consistent, year-round demand for long-term rental properties. |

As the data shows, the appeal is built on more than sunshine. The numbers reveal a healthy, functioning market that rewards investors who conduct thorough due diligence.

To see how Portugal stacks up against other top-tier destinations, it’s worth checking our guide on the best countries to invest in property. This briefing sets the stage for a deeper dive into the practical realities of investing here, from calculating returns to understanding local market dynamics.

The True Cost of Living in Portugal

A primary driver behind Portugal’s growing popularity is its affordability relative to other Western European nations. For a property investor, this is not merely a lifestyle perk; it is a core piece of market intelligence.

Understanding day-to-day expenses helps you gauge rental demand, forecast potential yields, and ultimately assess your return on investment. A lower cost of living makes a location more attractive to long-term tenants, which in turn creates a more stable and predictable income stream for your asset.

According to data from major economic bodies, the cost of living in Portugal is approximately 15-25% lower than in the United Kingdom. This differential is a significant draw for the growing expat community—a reliable tenant base of retirees, digital nomads, and young professionals. While major cities are more expensive, the value proposition remains strong across the country.

A Tale of Two Budgets: Lisbon vs Porto

As an investor, it is crucial to look beyond national averages and analyse specific city markets. Lisbon, as the capital and economic hub, naturally carries the highest cost of living. A couple can expect to live comfortably on around €2,500–€3,000 per month, excluding rent.

Housing is the largest variable, with apartments in the city centre commanding premium rental rates.

In contrast, Porto offers a more accessible entry point. Portugal's second city provides an excellent quality of life but with significantly lower overheads. Here, a similar couple might budget in the region of €1,800–€2,200 per month. This affordability is a powerful magnet for creatives and professionals, fuelling strong rental demand in a city rapidly gaining a reputation as a major tech and tourism hub.

Investor Takeaway: This cost differential is a strategic insight. While Lisbon offers prestige and high demand, Porto presents an opportunity for potentially stronger net rental yields, as acquisition costs and tenant living expenses are more manageable.

Breaking Down Monthly Expenditures

To build a realistic financial model for a potential buy-to-let, you must understand a typical tenant’s monthly outgoings. These costs directly determine their disposable income available for rent.

Here is a practical breakdown of estimated monthly costs for a single person living just outside the prime city centres:

- Groceries: A weekly shop at a major supermarket like Continente or Pingo Doce will typically run between €200 and €300 per month. Local markets can offer better value.

- Utilities: This covers electricity, water, gas, and high-speed internet. A budget of €100 to €150 per month is advisable, though this can increase in winter with heating costs.

- Transport: A monthly public transport pass in Lisbon or Porto costs around €40, providing unlimited travel on the metro, buses, and trams.

- Healthcare: While the public SNS system is available to residents, many expats opt for private health insurance. Depending on age and cover, this can cost between €40 and €100 per month.

This data demonstrates that even in Portugal’s main cities, core living expenses are modest. This financial stability for residents is the bedrock of a healthy long-term rental market, helping to ensure tenants can consistently meet their obligations. This reality of everyday life makes an investment in Portuguese residential property a fundamentally sound decision.

Navigating the Portuguese Property Market in 2026

For any investor evaluating Portugal, it is the market's underlying strength that warrants a closer look. The market in 2026 is defined by a simple, powerful dynamic: a persistent housing shortage, unwavering demand, and new government policies designed to increase housing supply.

This combination creates a remarkably resilient environment for property values. The chronic lack of available housing, especially in key cities and along the coast, exerts steady upward pressure on prices and fuels strong rental demand. For investors, this is not a speculative bubble; it is a market where asset growth is driven by genuine, long-term need.

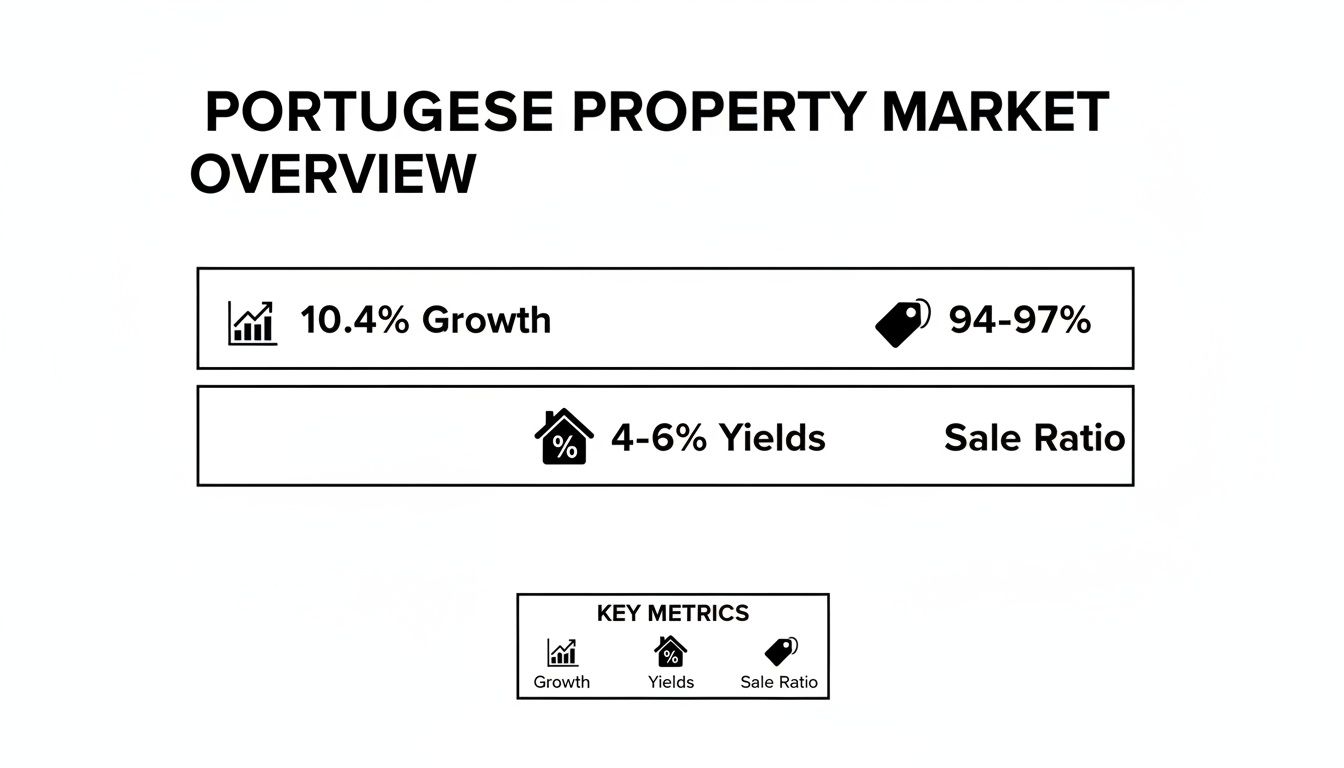

A clear indicator of market health is its rental yields. In major hubs like Lisbon and Porto, and across sought-after parts of the Algarve, gross rental yields are holding firm between 4-6%. This offers a reliable return that is becoming harder to find in many other established Western European markets.

Understanding Market Dynamics

When analysing opportunities, it is crucial to look beyond initial asking prices and understand on-the-ground negotiation realities. The average sale-to-asking price ratio across Portugal currently sits between 94% and 97%. This indicates that properties are, on average, selling very close to their list price, pointing to a competitive market.

However, a deeper dive into transaction data reveals that 70-80% of properties ultimately sell for below the initial asking price. This is not a contradiction. It signifies that while the market is competitive, there is still room for a skilled negotiator to secure a favourable deal. Inflated opening prices are common, creating an opportunity for well-informed buyers to acquire a property at a more realistic valuation.

This is a critical distinction for any investor. It means that while you must be prepared for competition, you should not be afraid to make a well-researched offer below the asking price. Working with a reputable local agent who understands regional nuances is key to navigating this successfully.

The Impact of Government Policy and Economic Stability

The Portuguese government is now actively tackling the housing deficit with its 'Build Portugal' package. This collection of policies aims to accelerate planning permissions, simplify the conversion of commercial properties into residential units, and incentivise new construction. While these changes will take time to fully impact supply, they signal a clear, long-term commitment to resolving the housing shortage, which should help stabilise the market for years to come.

Simultaneously, the stabilisation of interest rates from the European Central Bank (ECB) is bringing much-needed predictability back to the mortgage market. After a volatile period, more stable borrowing costs are making it easier for both local and international buyers to plan their finances. For investors, this creates a more dependable framework for calculating long-term returns and leveraging capital.

The real estate sector's resilience is further highlighted by its performance within the broader economy. It is a cornerstone of foreign investment, providing a secure and profitable avenue for capital, even during periods of wider economic uncertainty.

The property sector’s performance continues to be a standout feature of the Portuguese economy. In 2025, real estate investment showed robust growth of 10.4% to €3.905 billion, a testament to its strength even as overall foreign direct investment (FDI) saw a decline. By the end of that year, Portugal’s total FDI stock reached €213.731 billion, equivalent to 70% of its GDP, with non-resident property income flows totalling €13.4 billion, underscoring the strong returns available to UK portfolios. Projections for 2026 suggest this momentum will continue, with the ongoing housing shortage expected to drive price growth of 2-5%. You can discover more about the UK's role as a major investor in Portugal in recent reports.

This solid economic footing, combined with a clear understanding of market specifics, provides a compelling case. For those new to buying abroad, our guide on investing in overseas property offers further foundational knowledge. The Portuguese market offers a mature, stable environment where data-driven decisions can yield impressive long-term results.

Where to Invest: A Regional Deep Dive into Portugal

Choosing the right location in Portugal is the most critical decision an investor will make. The country is not a uniform market; life in the Algarve, for instance, operates on a completely different economic rhythm than downtown Lisbon. A successful strategy depends on matching investment goals—whether steady rental income, long-term capital growth, or a hybrid of both—with the unique economic drivers of a specific region.

For international investors, the primary question is often whether to focus on proven, high-demand markets or explore emerging locations with higher growth potential. A granular, regional analysis is essential for making an informed decision.

The Portuguese property market has been defined by solid fundamentals, offering both reliable income and the potential for significant appreciation. The data tells a compelling story.

These figures point to a market with strong underlying health, rewarding investors who know precisely where to allocate capital.

Property Investment Comparison: Lisbon vs. Porto vs. Algarve

To gain a clearer picture, it is helpful to compare Portugal’s three most popular regions for foreign buyers head-to-head. Each offers a distinct investment profile.

| Metric | Lisbon | Porto | Algarve |

|---|---|---|---|

| Market Profile | Established, premium, stable | High-growth, dynamic, affordable | Resilient, tourism-driven, lifestyle |

| Average Price/m² | €6,059 | €4,060 | Varies widely (€2,500 – €4,500+) |

| Typical Yields | 4% – 6% (long-term let) | 5% – 7% (long-term let) | 5% – 8%+ (short-term holiday let) |

| Primary Driver | Corporate HQs, tech, finance | Tech, tourism, young professionals | Tourism, retirees, holiday homes |

| Best For | Capital preservation, reliable demand | Capital growth, high rental yields | Seasonal income, lifestyle investment |

| Risk Profile | Lower | Medium | Medium (seasonal dependency) |

This comparison highlights the trade-offs. Lisbon offers stability at a higher price point, Porto presents a compelling growth story with attractive yields, and the Algarve delivers a powerful lifestyle and holiday-let combination. The optimal choice depends entirely on your investment objectives.

Established Hubs: Lisbon and Porto

As Portugal’s undisputed economic and cultural capital, Lisbon continues to attract a steady stream of international companies, tech start-ups, and high-net-worth individuals. This constant influx fuels demand for premium property, supporting the city's high entry costs but also providing a level of stability and liquidity that is difficult to find elsewhere. It is a market suited to conservative investors focused on long-term wealth preservation.

Porto, on the other hand, offers a more dynamic growth story. Once the nation's industrial heart, it has reinvented itself as a vibrant hub for technology, tourism, and the creative arts. This transformation has ignited its property market, offering investors a much lower cost of entry than Lisbon but with significant potential for capital growth. The city’s affordability continues to attract young professionals and digital nomads, creating a deep and reliable tenant pool for buy-to-let properties. Gross rental yields for city-centre apartments can realistically be between 5% and 7%, often outperforming those in the capital.

Recent market data from Portugal's National Statistics Institute (INE) supports this. Median asking prices recently hit a record €3,076/m², a 12.2% year-on-year increase. Lisbon led the prime markets at €6,059/m², with Porto following at €4,060/m². For a full breakdown, you can learn more about Portugal's 2026 real estate market predictions in recent detailed analyses.

The Resilient Algarve Market

The Algarve's economy operates on a different rhythm, powered almost entirely by tourism and its large, affluent retiree community. Its property market is famously resilient, supported by a high number of international cash buyers, which helps insulate it from the fluctuations of domestic mortgage rates. The region’s primary draw is its powerful holiday-let market, which can generate excellent short-term rental income, especially during high season.

Investor Takeaway: The Algarve represents a dual opportunity. It is a world-class lifestyle destination that also functions as a high-performance asset class, with market projections showing steady growth of 3-6% underpinned by relentless international demand.

While prime coastal locations like Vilamoura and Lagos will always command premium prices, astute investors are increasingly looking at towns slightly further inland. These areas offer more attractive entry prices while still being close enough to the coast to benefit from the tourism boom.

High-Growth Emerging Markets

Beyond the well-trodden paths of Lisbon, Porto, and the Algarve lie Portugal’s emerging markets. These are often quieter areas experiencing rapid price growth, typically due to new infrastructure projects, a search for affordability, or shifting demographic trends. Santarém, for example, is one such region that has seen property prices increase by over 25% in a single year, according to local housing authority data.

These markets are better suited to investors with a higher risk tolerance and a sharp focus on capital appreciation. While rental demand may not be as deep or proven as in the major cities, the potential for significant value growth is substantial. For those looking to diversify, our guide on the best buy-to-let locations offers a broader look at identifying these opportunities. Investing here demands more rigorous due diligence but can deliver exceptional returns for those who enter ahead of the curve.

Understanding Residency Visas and Tax Rules

Before entering the property market, it is essential to understand Portugal’s legal and financial regulations. The system is transparent, and there are no fundamental barriers preventing foreign nationals from owning property. The key is to understand the residency options and tax obligations, as both will directly impact your long-term returns.

While the residency landscape has shifted, excellent routes remain for non-EU citizens. The well-known Golden Visa programme no longer includes real estate, but other pathways like the D7 Passive Income Visa have become the preferred option for many investors.

This visa is designed for individuals who can demonstrate a steady passive income from sources outside Portugal, such as pensions, dividends, or existing rental properties. A minimum income of just over €820 per month is required for a single applicant. The D7 provides a clear path to temporary residency, convertible to permanent residency after five years, making it an excellent choice for those planning a long-term presence in Portugal.

Getting to Grips With Property Taxes

Once your residency strategy is clear, your main financial focus will be property taxes. These are straightforward and can be factored into your investment calculations from the outset. You will encounter two main taxes when buying and owning property.

The first is the Imposto Municipal sobre as Transmissões Onerosas de Imóveis (IMT), or Property Transfer Tax. This is a one-off tax paid upon completion of the purchase. The rate is progressive, increasing with the property’s value.

- For a primary residence valued at €300,000, your IMT liability would be approximately €8,165.

- For a second home or investment property at the same price, the tax is higher at roughly €12,565, as different rates apply.

The second tax is the Imposto Municipal sobre Imóveis (IMI), which is the equivalent of an annual council tax. It is calculated on the property’s registered tax value (VPT), which is typically lower than its market price. IMI rates are set by each municipality but usually fall between 0.3% and 0.45% of the VPT each year. On a property with a tax value of €200,000, you would expect to pay between €600 and €900 annually.

Investor Takeaway: A clear understanding of these tax obligations is essential for accurate financial forecasting. When calculating your net rental yield, these costs must be deducted from your gross rental income alongside other expenses like insurance and maintenance.

The Non-Habitual Resident (NHR) Scheme and its Successor

For many years, the Non-Habitual Resident (NHR) scheme was a major attraction for new residents, offering a flat 20% tax rate on certain Portuguese income and a full exemption on most foreign-sourced income. The original NHR scheme closed to new applicants in 2024.

However, the government introduced a successor programme to attract specific high-value professionals. This new scheme, often dubbed 'NHR 2.0', offers similar tax incentives but is targeted at a narrower group, including those in scientific research, technology, and higher education. For property investors who do not fall into these categories, Portugal’s standard tax rates will apply.

It is vital to obtain qualified local advice. Double-taxation treaties between Portugal and other countries, such as the UK, exist to prevent you from being taxed twice on the same income. You can take a deeper look into these rules if you want to understand property taxes for investors in greater detail.

Your Step-by-Step Guide to Buying Property

With a clear strategy, you will find navigating the Portuguese property market to be a remarkably straightforward process. The system is well-defined and secure, designed to protect both buyer and seller at every stage.

This is your practical checklist, breaking down the essential steps from arranging finance to completing the acquisition of your new property.

Your first move must be to obtain a Número de Identificação Fiscal (NIF), your personal Portuguese tax number. This is non-negotiable. Without a NIF, you cannot open a bank account, sign contracts, or complete a property purchase. A local solicitor or a specialist agency can typically procure this for you within a few days.

Assembling Your Professional Team

Once you have your NIF, the next step is to open a Portuguese bank account. This is crucial for transferring funds for your deposit and the final purchase, and it will simplify payment of future bills such as utilities and the annual IMI property tax.

With your finances prepared, the single most important decision is hiring a reliable, independent solicitor (advogado). It is critical that you do not use the seller's or estate agent's recommendation. Your solicitor's sole duty is to protect your interests. They will conduct thorough due diligence, checking for any debts on the property, verifying legal ownership, and ensuring all planning permissions are legitimate. This step alone mitigates the vast majority of potential issues.

Investor Takeaway: The role of the solicitor in Portugal is fundamentally different from that in the UK. They act as your legal safeguard, responsible for verifying every detail of the transaction before you make any binding financial commitments.

From Offer to Ownership

After identifying a suitable property, you will make a formal offer. If the seller accepts, your solicitor will draft the Contrato de Promessa de Compra e Venda (CPCV). This is a promissory contract that legally binds both you and the seller to complete the sale.

Upon signing the CPCV, you will be required to pay a deposit, typically between 10% and 30% of the purchase price. This contract has significant legal standing; if the seller withdraws after signing, they are legally obligated to repay you double your deposit. If you withdraw, you will forfeit the deposit.

The final stage is the Escritura, or the final deed of sale. This takes place at the office of a public notary (notário). The notary’s role is to witness the signing, confirm all legal paperwork is in order, and officially register the change of ownership. Once the Escritura is signed and the final payment is made, you become the new legal owner.

Your solicitor will then handle the final administrative tasks, ensuring the property is registered in your name at the Land Registry (Conservatória do Registo Predial) and the local tax office. For more on this topic, our guide to financing an investment property offers excellent additional insights.

Your Portugal Questions, Answered

Acquiring property in another country always raises practical, real-world questions. Here, we provide clear, straightforward answers to common queries from investors considering the day-to-day realities of owning property in Portugal.

What Are the Real Costs of Managing a Property From Abroad?

If you are managing a property from the UK or elsewhere, a reputable property management company is an essential operational partner. Their fees are a core running cost that must be factored into your return on investment calculations.

Typically, management companies charge a percentage of the monthly rent, usually between 8% and 12%. For this fee, they handle critical tasks: finding and vetting tenants, collecting rent, and managing minor maintenance issues. This expense provides peace of mind, ensuring your asset is maintained and rental income remains consistent.

It is also prudent to set aside an additional 1-2% of the property’s value annually as a contingency fund for larger repairs or unforeseen issues.

How Does Healthcare Work for Non-Resident Investors?

Even if you do not plan to live in Portugal full-time, access to healthcare is a sensible consideration, especially for longer stays. As a non-EU citizen who is not an official resident, you will need to rely on private health insurance.

Investor Takeaway: For any non-resident investor, comprehensive private health insurance is non-negotiable. A good policy for a healthy individual can run from €40 to €100 per month. This provides access to Portugal’s excellent private clinics and hospitals, where English is widely spoken and wait times are minimal.

Once you become a legal resident, you gain the right to register with the public healthcare system (the SNS). However, most international investors and expats find the convenience and broader access of the private system well worth maintaining.

Are There Financing Options for UK Buyers?

Yes, obtaining a mortgage in Portugal as a non-resident UK buyer is achievable, but the terms will differ from those offered to a local resident. Portuguese banks are generally open to lending to foreign buyers, but their requirements are stricter.

Most lenders will offer a loan-to-value (LTV) ratio of around 60-70%. This means you will need a cash deposit of at least 30-40% of the purchase price.

The bank will also conduct a thorough affordability assessment, examining your global income and liabilities. To streamline the application process, it is vital to have all your financial documents in order—including tax returns, bank statements, and proof of income. Engaging a specialist mortgage broker who deals with non-resident applications can be highly beneficial.