A mortgage offer can arrive far faster than most investors expect. In the UK, the formal application can take two to six weeks, and some lenders' document reviews move in 1 day while others take 12 days for the same step, according to Uswitch's mortgage timing guide and reported lender turnaround examples from HousingUK user data. That gap matters more than most rate tables suggest.

For a global property investor, the mortgage approval timeline isn't just an administrative detail. It shapes exchange deadlines, foreign exchange planning, refurbishment scheduling, tenant onboarding, and cash drag across the portfolio. A lender that looks competitive on headline pricing can still cost you money if its underwriting team moves slowly or repeatedly asks for revised documents.

The practical mistake is treating “mortgage approval” and “property purchase” as the same clock. They aren't. One is a lending decision. The other is a transaction with legal, valuation, and chain risk layered on top.

Understanding the Full Property Purchase Timeline

Many buyers ask how long a mortgage takes, when the more useful question is how long the entire purchase takes.

In the UK, the average time from starting a property search to completion is about 6 months, while the formal mortgage approval itself may only take up to a couple of weeks in straightforward cases. After a formal offer arrives, the remaining legal and conveyancing process adds roughly 12 weeks, according to HSBC's home-buying timeline.

That distinction changes how an investor should plan capital. If you assume that a fast mortgage offer means fast completion, you can mistime deposit transfers, refurb contractors, furnishing orders, and letting instructions. In practice, the lender may be ready long before the lawyers are.

Why investors misread the timeline

International buyers often compress everything into one mental step: approval, exchange, completion, rental income. But each stage runs on different actors and different incentives.

- Lenders review affordability, credit profile, and the asset.

- Surveyors value the property.

- Solicitors investigate title, searches, and contract terms.

- Other buyers and sellers influence the chain.

- You still need to organise funds, certify documents, and answer queries quickly.

That's why a deal can feel “approved” while still being weeks away from legal completion.

Practical rule: Treat the mortgage offer as permission to proceed, not as proof the purchase is nearly finished.

The strategic implication for portfolio planning

For buy-to-let investors, timing affects return as much as price. A delayed completion pushes back renovation, listing, and rent commencement. That doesn't always change the long-term thesis, but it does affect short-term ROI and cash utilisation.

This is especially relevant if you're coordinating overseas acquisitions. A buyer managing currency exposure, travel, and local legal counsel should build the transaction around the full purchase cycle, not only the lender's approval window. That's one reason investors researching buying property overseas need to compare legal process as seriously as mortgage terms.

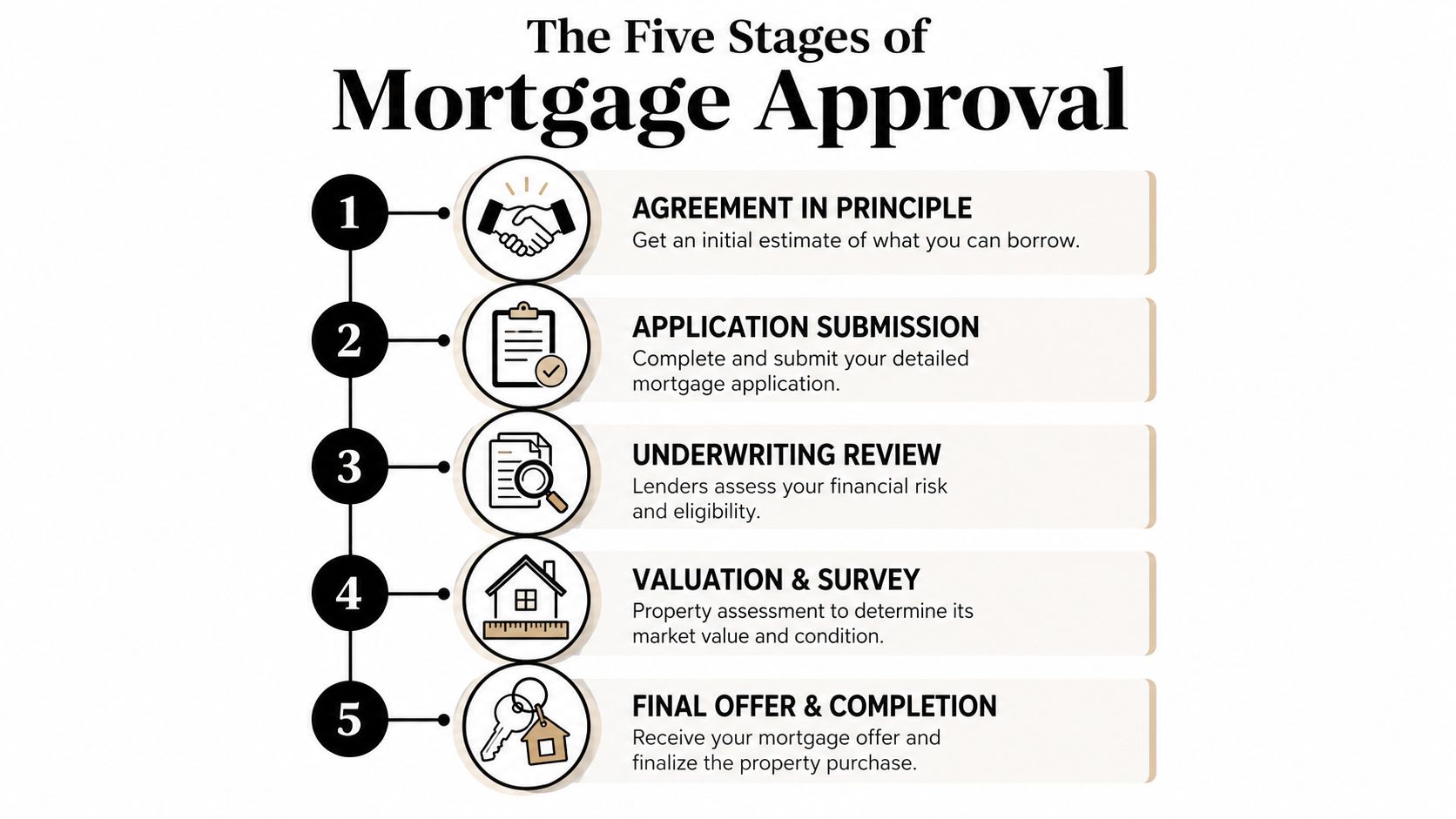

The Five Stages of the Mortgage Approval Process

A mortgage case can look straightforward on paper and still lose a property if it lands with a slow lender, a cautious valuer, or an underwriting team that does not handle overseas income well. The process matters, but the hand-off points matter more. That is where timing expands or contracts.

Stage one: Agreement in Principle

An Agreement in Principle gives an early indication of borrowing capacity based on headline financial details and a preliminary credit check. It helps set the search range, but for investors it does something more useful. It shows whether the lender is even plausible for your case.

That distinction matters. A lender that is fast for a local salaried applicant can become slow once the file includes foreign currency income, company dividends, trust structures, or several existing mortgages. If you plan to buy property abroad with a mortgage, lender fit at this stage often matters more than the headline rate.

Stage two: Full application submission

This is the point where the lender stops assessing a scenario and starts assessing your actual deal. The property, loan amount, deposit source, income evidence, and identity documents all need to line up.

Many delays begin here, not in underwriting. Small inconsistencies create avoidable queries. Different name formats across passports and bank statements, unexplained inbound transfers, gifted deposits without a paper trail, or translated documents that are not certified properly can all move a file into the slower queue.

Clean packaging saves time.

Stage three: Underwriting review

Underwriting is the lender's credit decision. The underwriter checks whether the income is acceptable, whether the existing debt load is manageable, whether the deposit is credible, and whether the overall case fits policy.

This is also where lender-specific speed differences become obvious. Some lenders issue simple queries quickly and keep momentum. Others review in batches, pause for manual sign-off, or ask for one document at a time. For an investor managing a chain, a rate lock, or a currency conversion window, that difference is not administrative detail. It can change whether the purchase remains viable on the original terms.

Stage four: Valuation and survey

The lender then tests the property as security. That usually starts with a basic valuation for mortgage purposes, and sometimes it escalates if the valuer raises concerns about condition, construction type, lease length, or marketability.

Investors should separate the lender's priorities from their own. A mortgage valuation is designed to protect the bank's position. It may confirm that the asset is acceptable security while telling you very little about refurbishment risk, future maintenance, or tenantability. If the property is unusual, tenanted, recently converted, or in a thinly traded market, this stage can slow sharply because the valuer may need more evidence or a second review.

A lender valuation confirms whether the property supports the loan. It does not tell you whether the deal suits your investment plan.

Stage five: Formal offer, legal work, and completion

Once the underwriter is satisfied and the valuation is acceptable, the lender can issue the formal mortgage offer. That is a major milestone, but it is still not the finish line.

The legal process still has to clear title checks, searches, contract review, lender conditions, and completion logistics. For international buyers, this final stretch often carries extra friction. Certified ID, cross-border fund movements, anti-money-laundering checks, and signing requirements can all add time even after the credit decision is done.

The sequence is straightforward:

- Agreement in Principle sets the initial borrowing range.

- Full application turns the enquiry into a live case.

- Underwriting assesses you as a borrower.

- Valuation assesses the property as security.

- Formal offer and completion convert approval into an acquired asset.

Investors who understand these stages ask better questions and pressure the right party. If the valuation is complete but the file is still waiting for an underwriter, the valuer is not the bottleneck. If the offer is out but exchange keeps slipping, the delay has usually moved to the legal side or the chain.

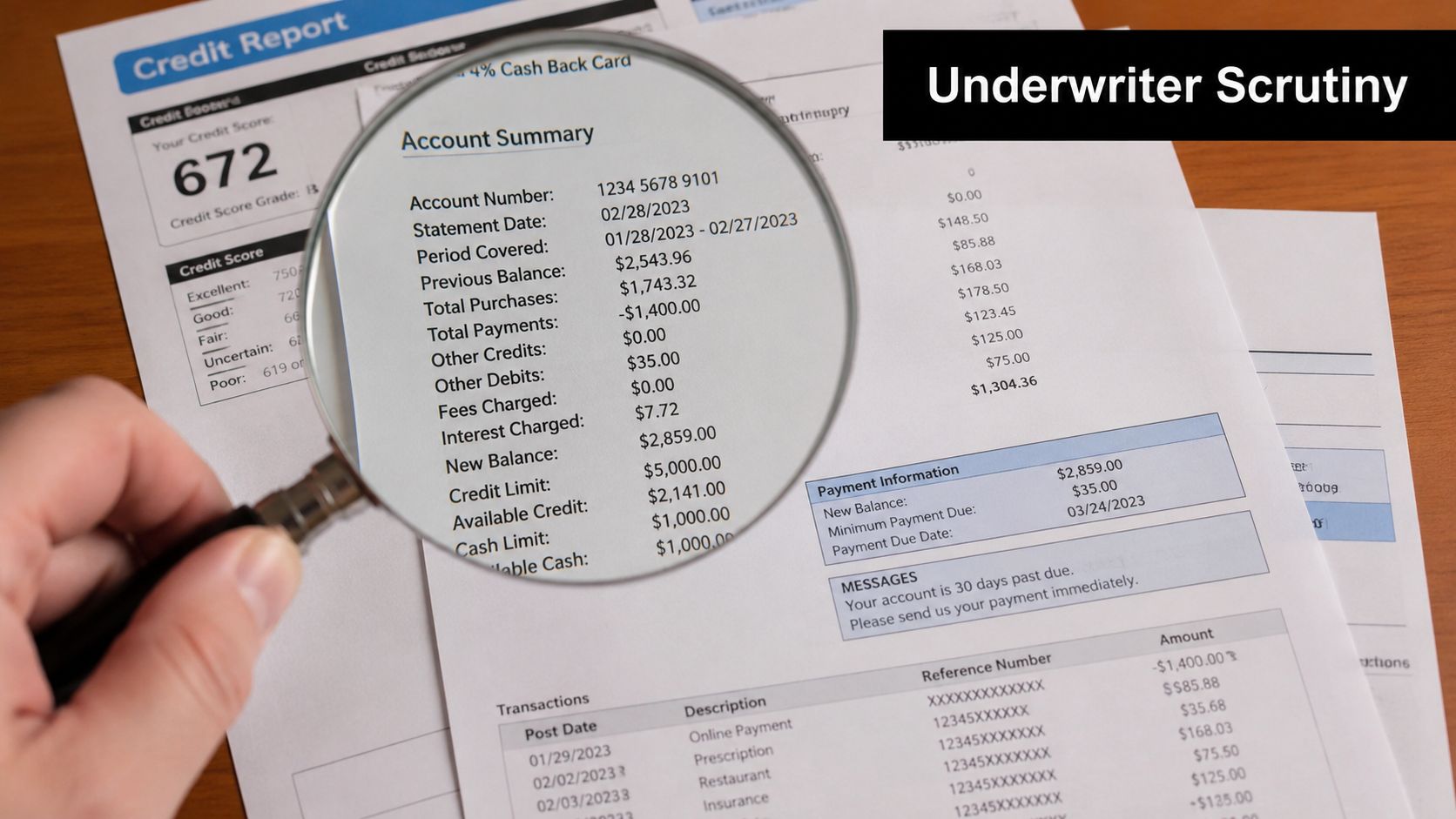

What Mortgage Underwriters Actually Scrutinise

Underwriters don't approve enthusiasm. They approve evidence.

From an investor's perspective, they're checking three things. Can you repay the loan, have you managed credit responsibly, and is the property acceptable security? Everything else is detail around those questions.

Creditworthiness and conduct

The credit check is less about a single score and more about behaviour. Underwriters look for missed payments, heavy unsecured borrowing, recent new credit, and signs that your liabilities are rising faster than your income base.

For international applicants, this can get awkward. A strong financial profile in one country may not map neatly into another lender's systems. Some lenders are comfortable with that. Others respond by asking for more documents and more explanation.

Affordability and income quality

Income isn't judged only by amount. It's judged by stability, provability, and the lender's confidence that it will continue.

Salaried PAYE income is usually easiest. Self-employed income, variable bonus income, foreign-currency earnings, freelance contracts, and portfolio income often need more interpretation. The more moving parts in the income picture, the more likely the underwriter will ask follow-up questions.

That's where many investors lose time. They answer the literal request, but not the underlying concern. If the lender asks for bank statements, it may really be asking whether your declared income lands where and when you say it does. If it asks about an overseas account, it may be testing source of funds, tax clarity, or transferability.

The property as security

Lenders are not buying your investment thesis. They're assessing whether the property is saleable if they ever need to repossess.

That means they care about condition, location, title issues, construction type, lease terms where relevant, and whether the valuation supports the agreed price. A property with strong rental potential can still be poor lending security if legal or physical issues reduce marketability.

For investors using financing across several assets, this is why one unusual property can slow an otherwise straightforward portfolio expansion.

Investor's lens: The lender underwrites both borrower risk and asset risk. If either side looks unclear, the mortgage approval timeline stretches.

A practical way to prepare is to review your finances the way a lender would. Keep a clean explanation for debts, document all income sources, and calculate obligations before you apply. If you need a framework for analysing affordability, this guide on how to calculate debt-to-income is a useful starting point.

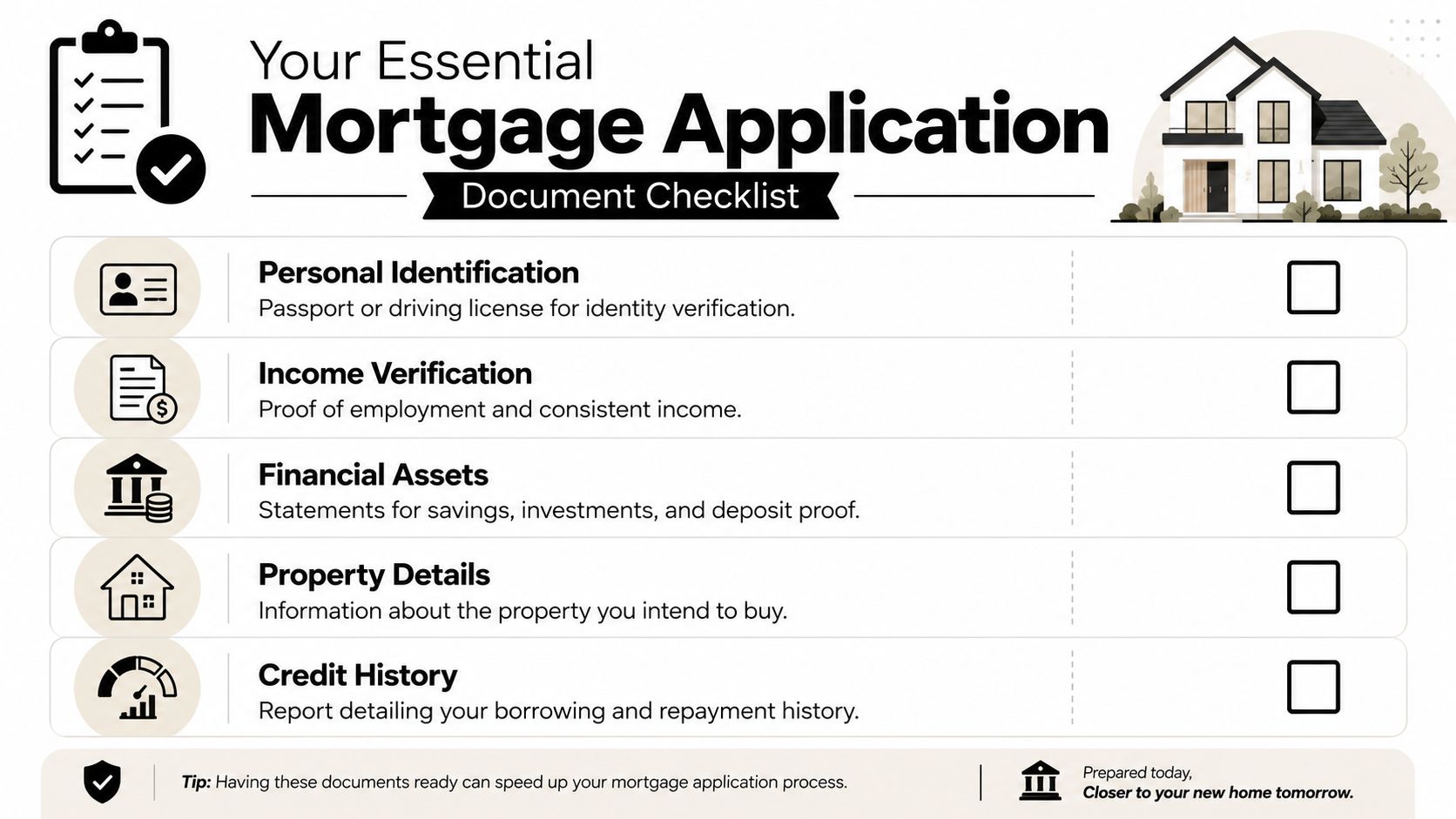

Your Essential Mortgage Application Document Checklist

Paperwork quality changes the timeline more than many borrowers expect. A lender can price a case in minutes and still spend days chasing missing pages, unexplained transfers, or ID records that do not line up across jurisdictions. For international investors, those gaps also raise source-of-funds and compliance questions that can stall a deal at the worst possible point.

A strong submission pack does two jobs. It proves the facts, and it removes obvious reasons for the underwriter to come back with follow-up queries.

Identity and residency records

Start with documents that establish who you are and where you live now.

- Primary ID: Passport is standard. Some lenders also ask for a driving licence or national ID card.

- Proof of address: Utility bills, bank statements, or tax letters that match the address entered on the application.

- Visa or residency evidence: Foreign nationals should have the current right-to-reside documents ready if the lender or country requires them.

Consistency matters more than applicants assume. If your passport includes multiple given names but your bank statements do not, explain it in the initial pack instead of waiting for the lender to flag it.

Income and affordability evidence

Lender-specific differences begin to show. One bank may accept standard salary credits and recent payslips. Another may want employer confirmation, bonus history, or translated income records if earnings are generated abroad.

- Salaried applicants: Payslips, employment confirmation, and bank statements showing salary receipt.

- Self-employed applicants: Filed accounts, tax returns, accountant certificates, and business bank statements where requested.

- Landlords and portfolio investors: Tenancy agreements, rental schedules, mortgage statements, and in some cases a full asset and liability summary.

- International earners: Foreign payslips, tax records, translations where needed, and statements showing money arriving into traceable accounts.

I often advise investors to add a short covering note where the income picture is split across countries, companies, or currencies. That single page can prevent the file being parked while the underwriter tries to reconstruct the story.

Deposit and source-of-funds proof

Deposit evidence causes a disproportionate share of delays. The lender and the solicitor both need a clean trail, and their questions are not always identical.

- Savings: Statements showing funds building up over time.

- Sale proceeds: Completion statements or contract notes if the money came from selling property, shares, or another asset.

- Gifted deposits: Gift letter, donor ID, and evidence of how the donor accumulated the funds if requested.

- Cross-border transfers: Statements from both sending and receiving accounts, plus FX confirmations where relevant.

Buyers who want a broader reference point can review loan documentation requirements to see how lenders typically organise evidence requests. For property purchases involving overseas assets, trusts, family gifts, or title issues across borders, bring your solicitor in early. A well-briefed international real estate lawyer can help align the legal file with the lender's compliance questions before they become a delay.

A good file does not just contain documents. It answers the next two questions before the lender asks them.

Why Mortgage Timelines Vary So Dramatically by Lender and Country

A mortgage that clears in three weeks in one market can take twice as long in another, even with a strong borrower and a straightforward property. That gap is not random. It usually comes from lender workflow, local legal process, and how cross-border income or funds are treated once the file reaches underwriting.

The broad market average is a poor planning tool. For an investor managing a chain, a rate lock, or a pending currency conversion, lender speed is part of pricing. A cheaper loan that arrives too late can cost more than a slightly higher rate from a lender that issues decisions consistently.

The lender matters as much as the rate

Two banks can quote similar terms and deliver very different timelines. One may review new documents the same day. Another may place every update back into a queue behind fresh applications. On paper, the products look close. In a live transaction, they behave very differently.

That difference matters most in time-sensitive cases. Purchase chains, auction deadlines, bridge exits, developer completion dates, and foreign exchange exposure all punish delay. If sterling, euros, or dollars move against you while the mortgage file sits in review, the financing cost changes before completion does.

A slower lender can still be the right choice if the spread is meaningfully better and the seller can wait. The mistake is treating service speed as a minor operational detail rather than a deal variable that affects negotiating position and total cost.

Internal underwriting workflow often sets the pace

Valuation gets the blame because it is visible. Internal document handling causes many of the longer delays.

Files slow down when the lender uses manual case allocation, applies extra checks to foreign income, or sends each follow-up back to the end of a review queue. International borrowers feel this more sharply. A domestic salaried applicant with one employer and one currency is easier for a lender to process than an investor with dividend income, offshore entities, or rent flowing through several accounts.

This is why experienced advisers track lender behaviour by case type, not just by headline service level. A bank that is reasonably fast for a local employee borrower may be much slower for a non-resident applicant or for a property held through a company structure.

In a time-sensitive purchase, underwriting speed is part of risk management.

Country rules change the timetable before the lender even starts

Mortgage timing does not transfer neatly from one country to another. The legal and banking systems are different, and those differences show up in approval times.

Some markets rely on highly standardised credit files and automated income checks. Others still depend on manual review, certified translations, wet-ink documents, notarisation, or in-person identity verification. Title systems vary as well. So do foreign buyer rules, anti-money-laundering checks, and the level of comfort local banks have with overseas wealth.

For international investors, country variation often creates a second layer of timing risk. The lender may be ready, but the valuation format may not satisfy local practice, the solicitor or notary may need extra proof of funds, or the bank may ask for documents in a form your home country does not usually produce.

Indicative Mortgage Timelines for International Investors 2026

| Market | Typical Time from Application to Offer | Key Process Bottleneck | Notes for Foreign Investors |

|---|---|---|---|

| UK | Often measured in weeks rather than days | Underwriting review, valuation scheduling, lender document queues | Strong lender choice, but timelines vary sharply by lender and by case complexity |

| USA | Often shaped by underwriting documentation and appraisal coordination | Document verification and appraisal | Credit history, tax returns, and state-level process differences matter |

| Spain | Often slower where bank review and legal checks need tight coordination | Bank compliance and document translation | Foreign buyers should expect close scrutiny of income origin and tax records |

| Dubai | Can be efficient for well-prepared borrowers, but process varies by bank and property type | Bank approval plus developer and transfer coordination | Residency status, bank relationship, and property eligibility can change the experience |

| Emerging markets | Often less standardised | Manual review, title certainty, banking procedures | Local legal advice is necessary because timing can vary more than official guidance suggests |

The practical question is narrower and more useful than “How long does a mortgage take?” Ask how long this lender is taking for this borrower profile, this property type, and this jurisdiction. That is the version that protects a deal.

Common Delays and How to Proactively Avoid Them

Most mortgage delays are foreseeable. They aren't always preventable, but they're rarely random.

The overlooked risk is repeated document chasing after valuation. Reported user data indicates that with a lender such as Nationwide, each update review can take 13 days, and repeated queries can turn a simple follow-up into a multi-week delay, as noted in this user-reported timeline discussion. Investors often focus on getting the valuation booked, when the bigger threat is what happens after the file returns to underwriting.

Repeated lender queries

This is the most common avoidable slowdown. A lender asks for one clarification. You answer partially. It comes back again.

To reduce that risk:

- Answer the issue, not just the request: If the lender queries a bank statement entry, explain the transaction and provide supporting evidence at the same time.

- Submit a complete revision pack: Don't drip-feed one page today and another next week.

- Use one point of coordination: Broker, adviser, or lead solicitor. Too many voices create inconsistent explanations.

Valuation and property issues

A valuation can trigger trouble if the surveyor questions the agreed price, flags condition issues, or identifies unusual property characteristics. Investors buying for yield sometimes accept stock that lenders view more cautiously than buyers do.

Useful safeguards include:

- Commissioning your own inspection where sensible: The lender's valuation won't replace your investment due diligence.

- Checking property type early: Unusual construction, short lease terms, or title quirks should be raised before application.

- Stress-testing the deal: If the valuation comes in lower than expected, know whether you'll inject more equity or renegotiate.

A short explainer can help if you want a visual overview of where files typically stall:

Legal and chain friction

Some delays have little to do with the mortgage itself. Solicitor response times, unresolved title issues, local searches, or another party in the chain can all hold up completion.

What works in practice:

- Instructing the solicitor early: Don't wait for the formal offer to start legal preparation.

- Checking chain dependency upfront: A vacant property and a long chain carry very different timing risk.

- Preparing source-of-funds evidence for legal review as well as lender review: Those are separate checks.

The fastest lender in the market can't rescue a deal if the legal side is underprepared.

Actionable Steps to Accelerate Your Mortgage Approval

Speed comes from preparation, lender selection, and disciplined communication. Most investors can improve all three.

Choose for execution, not just pricing

A cheap mortgage that arrives too late can be more expensive than a slightly dearer one that protects the deal. Ask your broker about current service levels for your borrower profile, not only the headline rate. If you're buying a second residence or mixed-use investment, lender appetite can narrow quickly, so it helps to understand second home mortgage requirements before you choose a bank.

Build a lender-ready deal room

Keep a single organised folder with ID, income evidence, bank statements, deposit trail, portfolio schedule, and any explanatory notes. Use consistent file names and current documents. If certification or translation is likely, arrange it before the lender asks.

This is especially useful for international buyers. Cross-border income and multi-account banking are manageable if presented clearly. They become a problem when documents arrive piecemeal and out of sequence.

Secure a robust Agreement in Principle early

A serious AIP does more than indicate budget. It surfaces likely policy issues before you spend money on valuation, legal work, or travel. If a lender is uneasy about foreign income, bonus reliance, or portfolio exposure, it's better to learn that before your offer is accepted.

Respond once, thoroughly, and fast

When the underwriter asks a question, send a complete answer pack. Include context, supporting documents, and a brief written explanation. Don't rely on the lender to infer what happened from raw statements.

A concise response often beats a long one. The underwriter needs clarity, not storytelling.

Align the lender, broker, and solicitor

Many delays come from sequencing errors. The lender waits for a document the solicitor has. The solicitor waits for funds evidence the buyer hasn't packaged. The broker assumes the client already sent an explanation that never arrived.

The strongest applications have one characteristic in common. Every adviser works from the same facts, in the same order, with the same deadlines. That's how you shorten the mortgage approval timeline without taking reckless shortcuts.

World Property Investor helps international buyers compare markets, buying rules, financing routes, and on-the-ground risks before they commit capital. If you're weighing where to invest next, explore the in-depth country guides, market analysis, and practical buying resources at World Property Investor.