Understanding the French property tax system is fundamental to securing a strong return on your investment. This guide breaks down the essential taxes you will encounter, from upfront acquisition costs to annual charges and the taxes levied upon sale.

Thinking of property taxes in France not as hurdles, but as fixed components of a financial model, allows you to build a robust investment strategy from the outset.

An Investor's Overview of French Property Taxes

A clear understanding of the French tax landscape ensures your financial projections are built on solid ground. For international investors, the system can seem complex initially, but it is structured around four main pillars, each impacting profitability at different stages of ownership. Factoring these costs in accurately is a non-negotiable step in any serious ROI analysis.

Unlike markets such as the UK where Stamp Duty Land Tax is a single, well-defined acquisition cost, France bundles its initial charges into the frais de notaire. This includes not just the notary's professional fee but also a significant transfer tax that varies by department. This distinction is critical for accurate budgeting and highlights the need for due diligence at a local level.

To provide a clear picture, here is a summary of the main taxes involved.

Key French Property Taxes at a Glance

| Tax Name | Description | When It is Paid |

|---|---|---|

| Frais de Notaire | A bundle of acquisition costs, primarily transfer tax and the notary's fee. | At the time of purchase. |

| Taxe Foncière | An annual local property tax paid by the owner, regardless of occupancy. | Annually, typically in autumn. |

| Taxe d'Habitation | A local residence tax, now applicable only to second homes and vacant properties. | Annually, typically in autumn. |

| Rental Income Tax | Tax on net income earned from letting property, plus social charges. | Annually, via a tax return. |

| Capital Gains Tax | Tax on the profit realised upon the sale of the property. | At the point of sale. |

| IFI (Wealth Tax) | An annual tax on net real estate assets valued over €1.3 million. | Annually, with your income tax return. |

Understanding these categories is the first step. Next, we will examine how they fit into the lifecycle of your investment.

The Four Pillars of Taxation

To build a robust financial model for a French property investment, it is essential to account for liabilities at every stage. The most effective method is to categorise them into four distinct phases:

- Acquisition Costs: These are the initial, one-off fees paid upon purchase, dominated by the notary fees (frais de notaire) and the transfer taxes bundled within them.

- Annual Local Taxes: These are recurring holding costs. The principal taxes are the taxe foncière (the property owner's tax) and, for second homes, the taxe d'habitation (the residence tax).

- Rental Income Taxation: If you let your property, the income generated will be subject to French income tax and social charges under one of two tax regimes.

- Capital Gains Tax: This is the tax paid on the profit you make upon disposal of the asset. The system offers significant reductions for long-term ownership.

For global investors, the key takeaway is that French property taxation rewards long-term commitment. The capital gains tax system, for example, offers tapering relief that provides a full exemption from the tax after 22 years of ownership and social charges after 30 years—a feature not commonly found in markets like the USA or Australia.

This structure provides a clear roadmap for accurate budgeting and informed decision-making. By understanding each component, you can strategically plan your entry, holding period, and eventual exit to maximise your returns. For more context on the broader challenges and rewards, you can learn more about investing in overseas property in our comprehensive guide. Each of these pillars requires careful consideration, as they collectively determine the net yield and overall success of your venture.

Calculating Your Initial Acquisition Costs

When entering the French property market, your first financial milestone is calculating the acquisition costs. These are known as the frais de notaire, or notary fees, and are a critical figure to establish accurately.

A common error among international buyers is to underestimate this figure, assuming it represents only the notary’s professional fee. In reality, the notary’s remuneration is a small component. The majority consists of taxes and administrative charges collected by the notary on behalf of the French state.

Consider the frais de notaire as a single payment bundling multiple costs. For an existing property, this typically amounts to between 7% and 8% of the purchase price. For new-build properties, it falls to approximately 2% to 3%. This significant difference is a fundamental consideration for investors comparing older properties with new developments.

The largest component of this bundle is the property transfer tax, known as droits de mutation or taxe de publicité foncière. This tax alone constitutes most of the acquisition cost, making it your largest upfront expense after the property's purchase price.

Breaking Down the Notary Fees

To truly understand your entry cost, you must know what is included within that 7-8% figure. While exact percentages vary slightly between French departments, the basic structure is consistent.

Here is what you are paying for:

- Transfer Tax (Droits de Mutation): This is the largest element, typically around 5.8% of the property price for older homes. These funds go directly to the local and departmental government.

- Notary's Remuneration (Émoluments): This is the notary's statutory fee for their legal work. It is regulated by the state and calculated on a sliding scale, usually averaging about 1% of the purchase price.

- Administrative Costs (Débours): These are minor, out-of-pocket expenses the notary pays to third parties for essential documents, such as land registry searches or urban planning certificates.

- Land Registry Contribution (Contribution de Sécurité Immobilière): A small fee of 0.10% of the property price is charged for the formality of registering the sale.

Example: Existing Property vs. New-Build

Let us apply this to a practical example. Imagine you are purchasing a property for €400,000. The difference in upfront costs between an existing home and a new-build is stark.

| Cost Component | Existing Property (Est. 7.5%) | New-Build Property (Est. 2.5%) |

|---|---|---|

| Purchase Price | €400,000 | €400,000 |

| Transfer Tax | ~€23,200 | ~€2,800 |

| Notary Remuneration | ~€3,800 | ~€3,800 |

| Other Fees | ~€3,000 | ~€3,400 (inc. VAT element) |

| Total Estimated Fees | €30,000 | €10,000 |

The table clearly shows that opting for a new-build could save an investor €20,000 in initial fees on a €400,000 purchase. New builds are subject to VAT (included in the sale price) instead of the much higher transfer tax.

This €20,000 saving is capital that can be immediately deployed elsewhere—for example, to furnish the property for the rental market or to be held as a larger cash reserve.

Budgeting for these fees from the outset is vital for a clear financial picture and forms the bedrock of your investment calculations. If you are considering how to cover these initial costs, you may find our guide on financing an investment property abroad useful for seeing how they fit into your overall funding strategy.

Understanding Annual Local Property Taxes

Once you have acquired your French property, attention shifts to the ongoing annual expenses that will shape your investment’s profitability. Two local taxes are critical for any international buyer to understand: the taxe foncière and the taxe d'habitation.

These are not minor administrative costs; they form a core part of your holding costs and must be factored into any calculation of your net rental yield. Levied by the local municipality (commune) to fund public services, their rates can vary significantly from one town to another, making pre-purchase research essential.

The Owner's Tax: Taxe Foncière

The taxe foncière is the fundamental property ownership tax. It is paid by the legal owner of the property as of 1st January each year. This tax is non-negotiable. It is irrelevant whether the property is your main home, a holiday home, a long-term rental, or vacant – if you own it, you pay it.

The calculation is based on two elements:

- The Cadastral Rental Value: This is a theoretical rental value, the valeur locative cadastrale. It should not be confused with actual market rent. It is an often-outdated figure set by tax authorities based on historical property assessments.

- The Local Tax Rate: Each local council sets its own tax rate, which is multiplied by the cadastral value to determine the final bill. This is why two similar properties in different locations can have vastly different tax liabilities.

For context, a house in a rural area might have a taxe foncière of around €800, whereas a similar-sized apartment in a prime Parisian arrondissement could easily result in a bill of €2,000 or more.

The Occupier's Tax: Taxe d'Habitation

The taxe d'habitation has undergone significant reform. While it has been abolished for all primary residences in France, it remains fully applicable to second homes (résidences secondaires). This makes it a crucial line item for international investors.

If your French property is not your main home, you are liable for this tax. It is technically paid by the person who has use of the property on 1st January. For a second home that is often vacant, that person is the owner.

A key consideration for investors: in high-demand areas officially designated as having housing shortages (zones tendues) – such as Paris, Lyon, or the Côte d'Azur – local councils can impose a surcharge of up to 60% on the taxe d'habitation for second homes. This is a deliberate policy to discourage properties being left empty and can significantly impact your annual outgoings.

This is a key departure from systems like the UK's council tax, where the charge applies regardless of how the property is used. You can explore these kinds of global differences as you understand property taxes for global investors.

Actions to Take Before You Buy

An unexpectedly high tax bill can disrupt your entire financial forecast. To avoid surprises after completion, undertaking due diligence is prudent.

Follow this simple checklist:

- Request Previous Tax Bills: This is the most reliable method. Ask the seller or estate agent for copies of the previous year's taxe foncière and taxe d'habitation notices (avis d'imposition). This provides a real-world figure to work with.

- Check with the Local Mairie: The local town hall (mairie) can provide the current tax rates for the area, which helps you understand the figures on the bills.

- Consult Your Notary: As part of the conveyancing process, your notary can obtain the official figures and flag any recent or planned changes to local tax policies.

By building these predictable annual costs into your financial model from day one, you ensure your investment is built on a solid foundation, ready for long-term success without unwelcome shocks.

How Rental Income Is Taxed for Non-Residents

If you are investing in a French buy-to-let property, understanding how rental income is taxed is non-negotiable. As a non-resident, any rent earned in France is subject to French tax and social charges, regardless of where you reside globally. The system is structured and predictable once you understand the rules.

For unfurnished properties, France offers two main tax regimes. The choice is between simplicity and precision: a straightforward flat-rate deduction versus meticulously tracking and deducting every expense to potentially lower your tax liability.

Choosing Your Tax Regime: Régime Micro-Foncier vs Régime Réel

The two systems are the régime micro-foncier and the régime réel.

The régime micro-foncier is the default option if your gross annual rental income is below €15,000. It is administratively simple. The tax office applies a flat 30% allowance for your running costs, meaning you are taxed on only 70% of the rent received. There is no need to keep receipts for minor repairs.

The alternative is the régime réel, which allows you to deduct your actual, provable expenses. This regime is mandatory if your rental income exceeds €15,000 per annum, but you can also opt for it even if you are below that threshold. For most investors with a mortgage, this is almost always the more financially astute choice.

Common deductible expenses under the régime réel include:

- Mortgage Interest: The interest portion of your loan repayments is fully deductible.

- Repairs and Maintenance: Costs from minor repairs to major redecoration.

- Local Taxes: The taxe foncière you pay each year can be deducted.

- Insurance Premiums: Landlord and building insurance costs are allowable.

- Management Fees: Fees paid to a letting agent or property manager.

For most leveraged investors, the régime réel is the clear winner. If your combined mortgage interest, taxes, and running costs exceed 30% of your gross rental income—which they almost certainly will—opting for this regime will reduce your taxable base and improve your net yield. Be aware that once you choose the régime réel, you are committed to it for a minimum of three years.

Understanding Tax Rates and Social Charges

Once your net taxable income is calculated, it is taxed using France’s progressive income tax bands. However, for non-residents, a minimum tax rate of 20% applies on income up to €29,315. For income above that, the rate increases to 30% (for the 2025 tax year).

Additionally, you must pay social charges, or prélèvements sociaux, currently set at 17.2%. This is a significant extra cost that must be factored into your return on investment calculations. It differs from systems like the UK's National Insurance, which is linked to employment rather than investment income. To see how these costs compare with other popular destinations, see our guide to the best countries to invest in property.

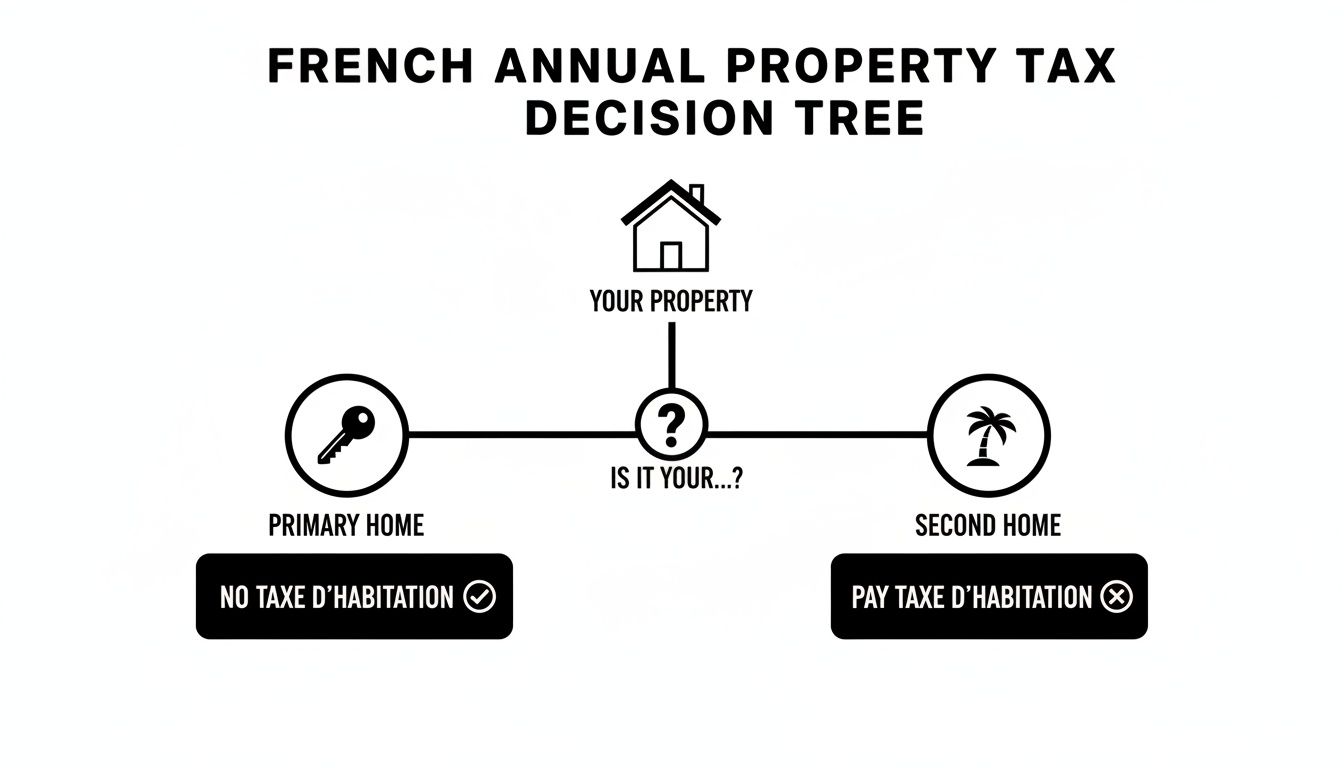

The decision tree below clarifies your liability for the annual taxe d'habitation, a key local tax that second-home owners are required to pay.

As shown, while this tax has been abolished for main residences, it remains a mandatory annual bill for international investors who own a second home in France.

Navigating French Capital Gains Tax on Property Sales

When you sell your French property, your exit strategy will be significantly shaped by the capital gains tax, known as the impôt sur la plus-value immobilière. This tax is levied on the profit from the sale, so understanding its structure is essential for calculating your true return on investment.

The tax comprises two parts. First is the base income tax on your gain, charged at a flat rate of 19%. On top of that, you must pay social charges (prélèvements sociaux) of 17.2%. Together, this creates a headline rate of 36.2% on your net profit—a significant figure if unplanned for.

However, the French system rewards long-term property ownership through a generous tapering relief scheme. For any serious investor, understanding this mechanism is crucial, as it can dramatically reduce, or even eliminate, your final tax bill.

Tapering Relief for Long-Term Investors

Tapering relief operates on a simple principle: the longer you have owned the property, the less tax you pay. The system gradually reduces the taxable portion of your gain each year. Crucially, the relief is applied on two different timelines—one for the 19% income tax and a longer one for the 17.2% social charges.

Here is how the relief on the 19% capital gains tax is structured:

- Years 1 to 5: No relief is available.

- Years 6 to 21: You receive a 6% reduction for each year of ownership.

- Year 22: A final 4% reduction is applied for the last year.

Following this timeline, you achieve a full 100% exemption from the 19% capital gains tax after holding the property for 22 years.

The relief for the 17.2% social charges follows a slower schedule. This means you will still have a social charges liability long after your main capital gains tax has been eliminated.

After 22 years of ownership, you are completely exempt from the main capital gains tax. However, full exemption from the associated social charges only comes after holding the property for 30 years. This distinction is vital for accurate financial planning.

This long-term incentive system is a defining feature of the French market, rewarding patient, buy-and-hold investors.

Calculating Your Taxable Gain

Before applying any relief, you must first calculate your net capital gain. It is not as simple as subtracting the purchase price from the sale price. The French tax authorities permit several important deductions to lower your taxable profit.

You can increase your original purchase cost (your "cost basis") by including:

- Acquisition Costs: You can either add a standard 7.5% of the purchase price to cover notary fees and other costs, or you can use the actual documented costs if they were higher.

- Major Works and Improvements: The cost of significant building work, extensions, or major improvements can be added, provided you have invoices from registered builders. If you have owned the property for more than five years, you can opt for a flat 15% allowance on the purchase price instead.

By correctly applying these deductions and timing your sale to maximise the tapering relief, you can plan a highly tax-efficient exit. For more insights into different approaches, you can explore our broader articles on global property investment strategies.

Wealth Tax and Inheritance Planning for Investors

Beyond the taxes on acquisition and ownership, two other major financial considerations exist for high-net-worth investors in France: the real estate wealth tax and the country's strict inheritance laws.

For serious international investors, understanding these is essential. Both can have a significant impact on your portfolio’s long-term value, and ignoring them can lead to costly surprises.

For those with substantial property holdings, France has a specific tax on real estate wealth known as the Impôt sur la Fortune Immobilière (IFI). This tax is focused specifically on the net value of real estate you own in France.

The IFI applies only when the net value of your French property assets exceeds a threshold of €1.3 million. It is a progressive tax, with rates starting at 0.5% on the value above €800,000 and rising to 1.5% for assets worth over €10 million.

For non-residents, the calculation is straightforward as it only includes French real estate. Furthermore, you can deduct outstanding mortgage debt and other property-related loans from the asset value, a strategy that can significantly reduce or even eliminate your IFI liability.

Inheritance Tax and Estate Planning

The other significant consideration is French inheritance tax, the droits de succession. This is a critical area for non-resident owners because French law applies to any real estate located on its soil, regardless of the owner’s nationality or residence. Your French property will be subject to French succession rules.

These rules can be punitive. French inheritance tax rates can be extremely high, especially for distant relatives or non-family members, where they can reach as high as 60%. This is a marked contrast to systems like the UK's, where Inheritance Tax is generally a flat rate above a certain threshold. Proactive estate planning is therefore non-negotiable.

Practical steps to mitigate this tax include:

- Double-Taxation Treaties: First, check the specifics of the treaty between France and your home country. These agreements exist to prevent your estate from being taxed twice on the same assets, but the details vary significantly.

- Gifting Allowances: France allows for tax-free gifts to be made to children and other relatives. Over time, this is a simple but effective way to reduce the overall value of your estate.

- Using a Property Holding Company (SCI): A Société Civile Immobilière (SCI) is a popular structure for international investors. Owning the property through an SCI means your heirs inherit shares in a company, not the physical building. This can offer greater flexibility and a potentially lower inheritance tax liability.

Intelligent, early planning around wealth and inheritance tax is a cornerstone of any successful long-term investment strategy in France. Consulting a legal and tax specialist with expertise in Franco-international property law is a crucial step to protect your assets for future generations.

Your Questions Answered

Acquiring property in France often raises several common questions, particularly for international investors. Here we address the most frequent queries to help you plan with greater clarity.

Do I Need a French Bank Account to Pay My Taxes?

In short, yes. While it may seem an additional administrative task, having a French bank account is practically essential. The local tax offices, the centre des finances publiques, strongly prefer payments by direct debit (prélèvement à l'échéance), which functions most reliably with a French account.

Attempting to pay from an overseas account can be problematic and risks missed deadlines, leading to penalties. A local bank account simplifies all financial matters, including utility bills, social charges, and receiving rental income. Consider it a core component of your investment infrastructure.

How Do Taxes Differ Between a New-Build and an Older Property?

The differences are most pronounced at the beginning of your investment.

- At purchase: New-build properties have much lower upfront costs. The notary fees (frais de notaire) are only around 2-3%, a substantial saving compared to the 7-8% on an existing home. This is because the main transfer tax is replaced by VAT, which is already included in the sale price.

- During the first two years: If you buy a new property, you can often obtain a two-year exemption from the taxe foncière. This is not automatic and depends on the local council, but it is a significant financial benefit.

To put this in perspective, on a €300,000 property, choosing a new-build could save you approximately €15,000 in acquisition costs alone. This is capital you can deploy elsewhere in your portfolio from day one.

What is an SCI, and Should I Use One?

An SCI (Société Civile Immobilière) is a private company established to own and manage property in France. They are popular for co-ownership, but for international investors, their main advantage lies in estate planning.

Under France's strict inheritance laws, transferring a physical property can be complex. With an SCI, you transfer shares in the company rather than the property itself. This can be a simpler and more tax-efficient method of succession.

However, establishing and running an SCI involves legal and annual administrative costs. Whether it is the right choice depends on your long-term plans and family circumstances. It is vital to seek professional legal advice before pursuing this option.

Can I Deduct My Mortgage Interest From My Rental Income?

Yes, provided you select the appropriate tax regime for your rental income. You will need to opt for the régime réel.

This system allows you to deduct all your actual expenses from your rental income before tax is calculated. This includes mortgage interest payments, insurance premiums, agency fees, and repair costs.

For most investors, especially those with a mortgage, the régime réel is a more advantageous choice than the alternative micro-foncier system, which offers a flat 30% deduction. Making the correct choice here can dramatically lower your tax bill and increase your net return each year.

At World Property Investor, we provide the in-depth analysis and practical guidance you need to make smart decisions in global real estate. Explore our comprehensive guides to uncover your next investment opportunity at https://www.worldpropertyinvestor.com.