For any global investor investing in overseas property, mastering the local tax system is non-negotiable. It is the fundamental difference between a profitable, long-term asset and an investment that underperforms. The French system, while comprehensive, is both logical and, crucially, predictable.

Unlike markets where tax legislation is subject to frequent and often politically motivated changes, France provides a clear, linear framework. Tax obligations are tied directly to the three distinct phases of an investment: acquisition, ownership, and disposal.

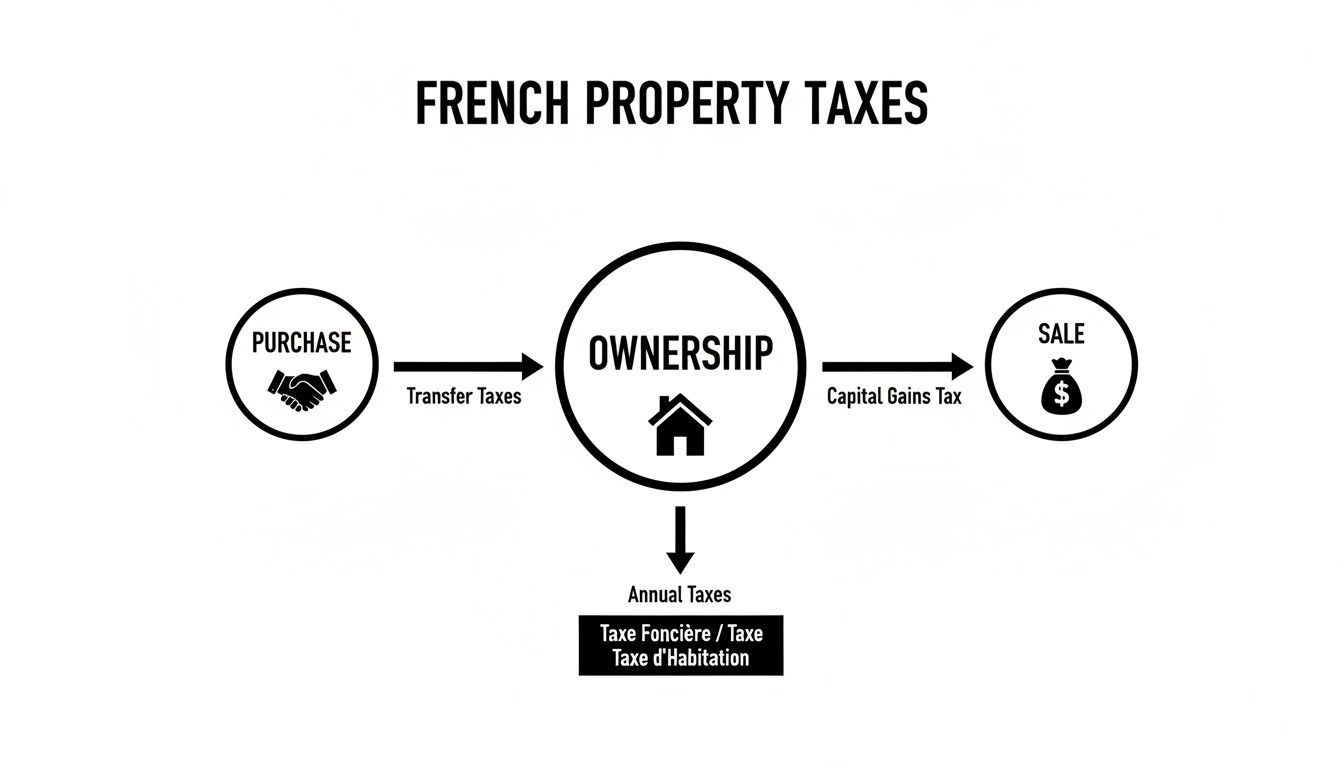

A Roadmap to French Property Taxes

An investor's timeline in France involves three key tax events: a one-off transactional cost at the point of purchase, modest annual contributions during ownership, and a final tax on any realised profit upon exit.

This structure provides a significant advantage for financial forecasting. By understanding the key levies—such as the initial frais de notaire or the annual taxe foncière—investors can model their cost base and potential returns with a high degree of accuracy.

The Three Stages of Property Taxation

Every property investor in France will navigate these three stages, each with its own specific taxes.

-

The Purchase Stage: This stage involves the upfront, one-time acquisition costs. The most significant of these is the frais de notaire (notary fees), a consolidated charge covering transfer taxes, registration duties, and the notary's fee, typically amounting to 7-8% on resale properties.

-

The Ownership Stage: These are the recurring, annual taxes paid for holding the asset. The principal tax is the taxe foncière, a land tax paid by all property owners. For second homes, the taxe d'habitation (residence tax) is also applicable, though this has been abolished for primary residences.

-

The Sale or Transfer Stage: Upon the disposal of the property, any capital gain is subject to tax. France incentivises long-term investment through a generous taper relief system, which can significantly reduce or eliminate this tax depending on the holding period.

This flowchart provides a clear overview of how these taxes map onto the investment lifecycle.

The system is designed for clarity. By understanding which tax applies at which stage, an investor can budget effectively and mitigate the risk of unforeseen liabilities.

To further clarify, the table below summarises the primary taxes encountered by international investors in France.

Key French Property Taxes at a Glance

| Tax Name | When It Applies | Who Pays | Key Consideration |

|---|---|---|---|

| Frais de Notaire (Stamp Duty) | At the point of purchase | The Buyer | A significant one-off cost, circa 7-8% of the property value for older properties. |

| Taxe Foncière | Annually during ownership | The Property Owner | A mandatory local land tax; rates are set by the local authority (commune). |

| Taxe d'Habitation | Annually during ownership | The Occupant/Owner | Now only applies to second homes and investment properties. |

| Capital Gains Tax | Upon sale of the property | The Seller | Tax on profit, but significant taper relief is applied after 5 years. |

| Rental Income Tax | Annually on rental profits | The Landlord | Taxed on net rental income, with different calculation regimes available to optimise the liability. |

This table provides a robust framework. The following sections will analyse the specifics of each tax, exploring calculation methodologies and effective management strategies.

Calculating Your Upfront Acquisition Costs

The asking price of a French property is only the starting point. For a serious investor, the true initial outlay is only understood once mandatory upfront costs are factored in. Accurate calculation of these costs is non-negotiable for determining the total capital required and projecting realistic returns.

The largest component of this initial expense is a consolidated charge, the frais de notaire. This is not merely a professional fee but a package of transfer costs, collected by the state-appointed notary (notaire) and distributed to the relevant government departments. Failing to budget for this can create a significant financial shortfall.

Deconstructing the Frais de Notaire

The frais de notaire is not a single tax but a combination of several distinct charges. Understanding its components provides clarity on where capital is allocated.

- Registration Taxes (Droits d'Enregistrement): This constitutes the majority of the cost and is the French equivalent of UK Stamp Duty Land Tax (SDLT), paid directly to the French Treasury. It is calculated as a percentage of the property price.

- Notary's Official Fee (Émoluments): This is the regulated payment for the notary’s professional services, including drafting the deed of sale, verifying title, and ensuring the legal compliance of the transaction. The fee is set by the state on a sliding scale based on the property's value.

- Administrative Disbursements (Débours): These are minor, out-of-pocket costs the notary incurs on the buyer's behalf, such as land registry search fees and town planning certificate costs.

Key Takeaway for Investors: The frais de notaire is a legally mandated bundle of taxes and duties, not a negotiable service fee. Accurate forecasting of this cost is a fundamental step in pre-acquisition due diligence.

Old vs New Build Properties: A Critical Distinction

A key variable determining the scale of your upfront costs is the property's age. The cost differential between an existing home and a new-build property is substantial and will directly impact your initial capital requirement.

For resale properties (defined as over five years old or having been previously sold), investors should budget for frais de notaire of approximately 7% to 8% of the purchase price. The full rate of registration tax drives this figure.

Conversely, new-build properties benefit from a significantly lower rate, typically between 2% and 3%. This is because the substantial registration tax is replaced by Value Added Tax (VAT), or Taxe sur la Valeur Ajoutée (TVA), which is already included in the developer's purchase price.

The Role of VAT in New Developments

The advertised price of a new-build property already includes a 20% VAT charge. While the reduced frais de notaire provides an immediate capital saving, astute investors may also be able to reclaim this VAT, transforming a major cost into a significant cash injection.

VAT reclamation is most commonly available through French leaseback schemes (résidences de services). If an investor purchases a new, furnished property and commits to letting it out for a specified period while providing hotel-style services (e.g., cleaning, reception), they may be eligible for a full refund of the 20% VAT from the tax authorities post-completion.

This mechanism makes new-builds a particularly compelling proposition for buy-to-let investors focused on maximising capital efficiency. For further insights on funding, our guide on financing an investment property provides practical advice.

Understanding Annual Ownership Taxes

Once the property is acquired, the focus shifts from one-off transaction costs to the annual taxes that directly impact the asset's net operating income. These are fixed, non-negotiable running costs that form the foundation of any credible annual budget.

For an international investor building a financial forecast, two main levies must be understood. Accurately projecting these costs is fundamental to ensuring the property performs in line with long-term expectations.

The Taxe Foncière: The Universal Property Owners Tax

The cornerstone of annual property taxation in France is the taxe foncière. This is a land tax that every property owner must pay, irrespective of whether the property is a primary residence, a holiday home, or a rental investment. If you own a property on the 1st of January, you are liable for the entire year's tax bill.

The calculation is based on a theoretical annual rental value assigned by the French land registry (cadastre), known as the valeur locative cadastrale. This figure is then multiplied by a percentage rate set by the local authority (commune), determining the final liability.

This local control means rates vary significantly between regions. An apartment in a major city such as Paris will likely have a different tax burden from a rural property in the Dordogne, even with similar market values. This contrasts with the UK's council tax system, where property valuations can remain static for decades, as noted by the Office for National Statistics (ONS). You can learn more about how different tax systems evolved, but the key takeaway is that French valuations are responsive to local economic conditions.

The Taxe d'Habitation: A Key Cost for Second Homes

The second major annual tax is the taxe d'habitation, or residence tax. This tax was recently abolished for all primary residences in France, which has caused some confusion. For international investors, however, it remains a critical and very real expense.

As most overseas buyers purchase property as a second home or holiday let, they are almost always liable for the taxe d'habitation. The tax is levied on the individual who has use of a furnished property on the 1st of January. For a second home, this is the owner.

Investor Insight: A common error for new investors is to assume the abolition of taxe d'habitation applies to them. It does not. This is a mandatory annual cost that will impact your net yield and must be included in all financial projections.

How to Forecast Your Annual Tax Bill

A significant strength of the French system is its transparency. It is possible—and highly advisable—to ascertain the exact annual tax costs for a property before making an offer. This removes guesswork and facilitates data-driven decision-making.

Here is how to obtain the figures:

- Request Previous Tax Bills: The simplest method is to ask the estate agent for copies of the previous year’s taxe foncière and taxe d'habitation bills (avis d'imposition) from the seller. A reputable agent will have these available.

- Account for Surcharges: In designated areas with housing shortages (zones tendues), local authorities can apply a surcharge of up to 60% on the taxe d'habitation for second homes. This can be a substantial unforeseen cost if not budgeted for.

- Integrate into Financial Models: Once you have these figures, they can be entered directly into your annual cash flow analysis, providing a clear picture of the property's true holding costs.

Understanding these annual taxes is fundamental for any serious global investor. By researching these fixed costs upfront, you can build financial forecasts on a foundation of certainty, ensuring a robust investment strategy from day one.

How Rental Income Is Taxed in France

Generating a consistent rental income is the primary objective for most property investors, but gross revenue is only half of the equation. The tax treatment of that income in France will ultimately determine your net yield and the overall success of the investment.

For non-resident landlords, a thorough understanding of this part of the tax system is essential. France offers a structured and transparent system, but the choices made within it can significantly alter an investor's annual tax liability.

Choosing Your Tax Regime For Furnished Rentals

For investors letting a furnished property—which typically offers the most favourable tax advantages—the system provides two main options: the simplified ‘régime micro-BIC’ or the more detailed ‘régime réel’. Understanding the mechanics of each is key to optimising rental profit.

The régime micro-BIC (Bénéfices Industriels et Commerciaux) is the default, simplified option, available as long as gross annual rental income remains below a specific threshold. Its main advantage is simplicity.

Investor Takeaway: Under the micro-BIC regime, the French tax authorities apply a 50% flat-rate allowance against gross rental income. This allowance is intended to cover all operating expenses, without the need to provide receipts. Tax is then levied on the remaining 50%.

This regime is ideal for landlords with low overheads. If actual expenses are significantly less than half of the rental income, this regime provides a straightforward tax saving with minimal administrative burden.

When The Régime Réel Makes More Sense

The alternative is the régime réel, or 'actual costs' regime. This is mandatory if rental income exceeds the micro-BIC threshold, but it can also be chosen voluntarily. For investors with higher costs, this is often the most financially advantageous option.

Under this system, instead of a flat allowance, you deduct all genuine, verifiable business expenses from your gross rental income. The list of deductible expenses is comprehensive, providing powerful tools to reduce taxable profit.

Common deductible expenses include:

- Mortgage interest payments.

- Property management and letting agency fees.

- Repair, maintenance, and improvement costs.

- Local property taxes (e.g., taxe foncière).

- Building insurance premiums.

- Depreciation of the property’s value and its furnishings.

The ability to deduct depreciation is a significant advantage. It allows for the amortisation of the building's and its contents' value over time, creating a substantial 'on-paper' expense. This can drastically reduce—or even eliminate—taxable income for several years, which is why experienced investors almost invariably opt for the régime réel.

While it requires diligent record-keeping, it offers far greater control over tax liability. Properly accounting for these deductions is fundamental when you calculate the return on investment (ROI) for a real estate asset, as they directly enhance net cash flow.

Comparison of French Rental Income Tax Regimes (Micro-BIC vs Réel)

Choosing between the simplified Micro-BIC and the detailed Régime Réel is a critical financial decision for a landlord in France. The optimal choice depends entirely on the property's specific cost structure and the investor's long-term strategy.

| Feature | Régime Micro-BIC (Simplified) | Régime Réel (Actual Costs) |

|---|---|---|

| Expense Allowance | A fixed 50% flat-rate allowance on gross rental income. | Deduction of all actual, verifiable expenses, including mortgage interest, repairs, fees, and depreciation. |

| Record-Keeping | Minimal. Requires only a declaration of gross rental income. | Meticulous. Requires detailed records and receipts for all claimed expenses, often necessitating an accountant. |

| Best Suited For | Landlords with low operating costs (well below 50% of income). | Investors with higher costs, particularly those with a mortgage or significant maintenance, or those wishing to claim depreciation. |

| Complexity | Very simple. Ideal for new investors or a single, low-maintenance property. | More complex. Involves detailed accounting but offers far greater potential for tax reduction. |

| Depreciation | Not applicable. The 50% allowance covers all deemed expenses. | A key benefit. Allows the write-off of the value of the building and furnishings over time, creating a significant tax shield. |

| Opting-In | Default regime if income is below the threshold. | Can be chosen voluntarily. Mandatory if income exceeds the threshold. |

The Micro-BIC is a suitable entry point for passive investors. However, as soon as actual costs (particularly mortgage interest) approach the 50% level, the Régime Réel becomes the far more profitable option.

Understanding Social Charges and Final Tax Rates

After calculating net rental profit, a further layer of tax applies: social charges, or ‘prélèvements sociaux’. These are a crucial component of property taxes in France and must be factored into yield calculations.

The standard rate for these charges is 17.2%. However, a significant reduction applies to residents of the EU, EEA, or Switzerland. If you are covered by the social security system in one of those countries, the rate is reduced to 7.5%. This makes a material difference to the final net return.

Finally, the remaining net profit is taxed at France's progressive income tax rates. For non-residents, a minimum flat rate of 20% applies to income up to approximately €29,000 (for 2025), rising to 30% for income above that threshold.

Navigating Capital Gains and Wealth Tax in France

An investment cycle concludes upon the sale of the asset. This is the point at which profits are realised and the French capital gains tax system, plus-values immobilières, becomes relevant.

Understanding this tax is vital for timing an exit strategy. Unlike markets in some emerging economies where tax rules can be unpredictable, the French system is structured to reward long-term investors. Its predictable, tiered approach provides the clarity required for multi-year financial planning.

Unpacking French Capital Gains Tax

When a property is sold for more than its acquisition price, the resulting profit is taxable. For non-residents, the headline rate is 19%. In addition, social charges (prélèvements sociaux) of 17.2% are applied, bringing the total initial tax rate to 36.2%.

However, very few long-term investors pay this full rate. The system’s most powerful feature is its taper relief mechanism, which progressively reduces the taxable gain based on the length of ownership. This is a deliberate policy designed to encourage stable, long-term ownership over short-term speculation.

This stability contrasts with the approach in other established markets. The UK's Stamp Duty Land Tax (SDLT), for instance, has seen significant volatility. On 23 September 2022, the UK government raised the nil-rate band, only for the subsequent Autumn Statement 2022 to schedule a reversal by March 2025. You can read more about these policy shifts and their impact on the UK market, but such changes highlight the relative predictability of the French system for long-term strategic planning.

How Taper Relief Slashes Your Tax Bill

The taper relief system operates on two separate schedules—one for the capital gains tax and another for the social charges. This distinction is crucial as it directly impacts the net proceeds from a sale.

Here is a breakdown of how the relief is applied over time:

-

For Capital Gains Tax (19% rate):

- Years 1-5: No relief.

- Years 6-21: A 6% reduction for each year of ownership.

- Year 22: A final 4% reduction.

- Result: After 22 years of ownership, the capital gain is completely exempt from the 19% capital gains tax.

-

For Social Charges (17.2% rate):

- Years 1-5: No relief.

- Years 6-22: A 1.65% reduction for each year.

- Years 23-30: An annual reduction of 9%.

- Result: After 30 years of ownership, the capital gain is fully exempt from all social charges.

Key Investor Takeaway: The French system is heavily weighted in favour of long-term property ownership. A full tax exemption on realised gains is not merely possible but a planned feature of the tax code, making a buy-and-hold strategy highly effective in this market.

Demystifying The French Wealth Tax

For investors with a substantial portfolio, one further tax must be considered: the Impôt sur la Fortune Immobilière (IFI), France’s real estate wealth tax. This is an annual tax levied on the net value of an individual's property assets, not on income or transactions.

The IFI applies only if the total net value of an investor's French real estate portfolio exceeds €1.3 million. For those who meet this threshold, it is a progressive tax, starting at 0.5% on the taxable value above €800,000.

Crucially, the tax is based on net assets. This allows for the deduction of outstanding mortgage debt from the property's market value. For many investors, this single deduction is sufficient to significantly reduce or even eliminate their IFI liability, underscoring the importance of strategic financing in portfolio management.

Planning For Inheritance And Double Taxation

Sophisticated investors plan beyond immediate yields and consider the long-term performance and eventual transfer of their assets. Estate planning is therefore a critical component for any international property owner.

Understanding French succession law and double taxation rules is fundamental to protecting wealth and ensuring a smooth transfer of assets to heirs without punitive tax liabilities.

France's approach to inheritance is fundamentally different from that of common law jurisdictions like the UK or the US. The system is structured around the relationship between the deceased and the beneficiary. While spouses and direct descendants benefit from generous allowances, distant relatives or unmarried partners can face tax rates as high as 60%.

French Inheritance Tax At A Glance

The tax liability is determined not by the size of the estate, but by the beneficiary's relationship to the deceased.

- Spouses & Civil Partners: Completely exempt from inheritance tax.

- Children (Direct Descendants): Each child receives a €100,000 tax-free allowance. The excess is taxed on a progressive scale from 5% to 45%.

- Unrelated Beneficiaries: Face a flat tax rate of 60% with a negligible allowance of just €1,594.

This structure makes strategic property ownership essential. For many international investors, holding property in a personal name is not the most tax-efficient method.

Using An SCI For Smarter Estate Planning

One of the most effective tools for managing French property succession is the Société Civile Immobilière (SCI). This is a private property-holding company. Instead of owning the property directly, family members own shares in the company that holds the asset.

This structure offers significant flexibility. It allows for the gradual transfer of ownership by gifting shares to heirs over time, utilising gift tax allowances that reset every 15 years. This provides greater control and can help mitigate the high inheritance tax rates, particularly for non-direct heirs. It is a cornerstone of sophisticated portfolio planning in France.

The Role Of Double-Taxation Treaties

For any global investor, the risk of being taxed twice—once in France and again in their home country—is a key concern. Double-Taxation Treaties (DTTs) are designed to prevent this. France has comprehensive agreements with most major economies, including the UK, USA, Canada, and Australia.

These treaties are legal agreements that define which country has the primary right to tax income, gains, or inheritance.

Investor Takeaway: A double-taxation treaty does not grant tax exemption. It ensures that tax is not paid in full twice. Typically, tax is paid in France first on French-source income (e.g., rental income or a capital gain). The investor's home country will then provide a credit for the tax already paid in France, which offsets the domestic tax liability.

This mechanism provides the certainty and predictability required for cross-border investment. Understanding how these treaties function is a key part of due diligence. For broader context, our analysis of the best countries to invest in property offers valuable global comparisons.

Your Questions Answered

When investing in French property from overseas, several practical questions consistently arise. Here are straightforward answers to the most common queries.

Do I Really Need a French Bank Account to Pay My Property Taxes?

Yes, for a serious investor, a French bank account is essential. While it is technically possible to pay from an overseas account, the process is often complex and unreliable.

The most efficient method for settling annual bills like the taxe foncière is by direct debit, which requires a French bank account. It also simplifies payment for utilities and other local services. Most major French banks are experienced in opening non-resident accounts, and the process is generally straightforward.

What Happens With Annual Taxes if I Sell the Property Mid-Year?

From the perspective of the French tax authorities, the individual who owns the property on 1st January is liable for the entire year's taxe foncière.

In practice, this is addressed during the conveyancing process. The notary will calculate the tax on a pro-rata basis and apportion the cost between the seller and the buyer. The buyer reimburses the seller for the portion of the year they will own the property, ensuring an equitable settlement.

Investor Tip: Always ensure that this tax apportionment is clearly itemised in the final deed of sale (acte de vente). While standard practice, explicit confirmation protects both parties and prevents post-completion disputes.

What Are the Penalties for Missing a Tax Deadline?

The French tax authorities enforce payment deadlines strictly. A missed deadline results in an immediate penalty, typically a 10% surcharge (majoration) on the amount owed.

Furthermore, late payment interest (intérêts de retard) can be added, which accrues on the outstanding balance. The authorities are efficient at pursuing unpaid taxes from both residents and non-residents, making timely payment essential to avoid unnecessary costs that erode investment returns.

At World Property Investor, we provide the in-depth analysis and practical guides you need to make informed decisions in global real estate. Explore our resources to invest with confidence. Find out more at https://www.worldpropertyinvestor.com.