Norway has a reputation for high living costs, a factor often viewed with caution. For the discerning property investor, however, this high-cost environment reveals a far more compelling narrative. It is underpinned by exceptionally high local wages and formidable purchasing power—the very fundamentals that sustain a healthy and stable rental market.

The high prices are not a barrier; they are an indicator of a market populated by tenants who can comfortably afford premium rents. For an investor, this translates into stability, reduced vacancy risk, and the potential for reliable, long-term returns.

What Is the Real Cost of Living in Norway?

For those analysing Norway from a property investment perspective, the real cost of living is not merely the price of consumer goods. It is the fundamental relationship between everyday expenses and average incomes. Norway operates on a high-cost, high-wage economic model, and a firm grasp of this dynamic is key to understanding its investment appeal.

This structure is the bedrock of the property market. It creates a robust rental sector where tenant affordability is not a persistent concern. While a familiar market like the UK may offer a sense of security, Norway presents a compelling case for premium diversification. The critical insight is not just that goods and services are expensive, but that the economy is sufficiently powerful to support these costs, generating predictable demand for quality housing from well-paid professionals.

Norway Living Costs at a Glance (2026 Estimates)

To provide clear context, the following table offers a snapshot of estimated monthly expenses in Norway. It highlights the core costs an investor must understand when assessing market dynamics and tenant affordability. All figures are based on credible economic data.

| Metric | Single Person | Family of Four | Key Data Point |

|---|---|---|---|

| Monthly Costs (Excl. Rent) | £1,095 / 13,424 NOK | £3,950 / 48,390 NOK | Overall cost of living is 26.9% higher than the US. |

| Average Rent | Lower than US | Lower than US | Rent is, on average, 21.6% lower than in the US. |

| Local Purchasing Power | Strong | Strong | Oslo’s purchasing power index is a robust 120.2. |

These figures, sourced from major economic bodies, demonstrate that while daily expenses are high, the economic structure more than accommodates them. This financial capacity is what gives the rental market its impressive resilience.

Comparing Norway to Key Global Markets

To fully appreciate the investment landscape, it is useful to compare Norway with other major economies. Data from early 2026 indicates that Norway's overall cost of living is 26.9% higher than in the United States. However, the metric that should command an investor's attention is that rent is, on average, a surprising 21.6% lower than in the US. This suggests a potential for rental growth and provides the foundation for strong yields.

A single person’s monthly costs, excluding rent, are approximately £1,095 (or 13,424 NOK). A family of four faces estimated costs of around £3,950 (48,390 NOK).

The fundamental story here is purchasing power. Oslo’s local purchasing power index sits at a strong 120.2. This means that high average salaries—often exceeding 50,000 NOK per month after tax—do more than just cover high consumer prices. They create genuine financial capacity, which is precisely the desired quality in a tenant base.

This economic strength contrasts sharply with some emerging markets, where lower living costs can be negated by weaker tenant financials. For instance, our guide on the cost of living in Malta explores a different investment profile, driven more by tourism and EU business. In Norway, stability stems from its powerful domestic economy, presenting a more secure, albeit premium, proposition.

For a UK investor, this translates into a clear opportunity. You are investing in a market where tenants can comfortably absorb rental costs, which mitigates vacancy risks and supports long-term asset appreciation. The high cost of living is not a red flag; it is a sign of market strength.

Breaking Down Norwegian Housing and Utility Costs

For any UK property investor evaluating opportunities in Norway, housing is not merely another line item—it is the central component. It represents the single largest expense for tenants and, in turn, directly shapes potential rental income and the ultimate return on investment (ROI).

The Norwegian property market, particularly in its principal cities, is defined by intense demand from a well-paid professional workforce. This creates an exceptionally stable environment for buy-to-let investors.

Unlike some markets where tenant affordability is a constant risk, the high local wages in cities like Oslo, Bergen, and Trondheim ensure a deep pool of renters who can comfortably meet premium rental rates. That stability is the bedrock of the investment case for Norway, driving down vacancy risks and supporting the consistent cash flow that underpins a successful portfolio.

Rental Prices in Key Norwegian Cities

As one would expect, rental costs vary significantly between cities, a trend consistent across Europe. Oslo, as the country's economic and political centre, naturally commands the highest rents, making it a prime target for investors focused on maximising rental income.

- Oslo: A one-bedroom flat in the city centre can readily exceed 12,000 NOK per month. For a two-bedroom property aimed at a professional couple or small family, rents often climb past 21,000 NOK.

- Bergen & Trondheim: These strong secondary cities offer a more accessible entry point. A similar one-bedroom flat might rent for approximately 9,000–11,000 NOK, presenting a different balance between property acquisition cost and potential rental yield.

Demand in these cities is underpinned by robust local economies—from the world-leading maritime industries in Bergen to the technology and education sectors in Trondheim. This consistent demand from qualified tenants is what keeps vacancy rates low, a critical factor in any investor's financial model.

Understanding Utility Costs and Their Impact

Utilities represent a significant and highly variable component of living costs in Norway. For an investor, understanding these expenses is vital, as they directly affect a tenant's overall budget and their capacity to pay rent.

Unlike in the UK, where utility bills are more predictable, Norwegian costs are heavily influenced by the country's long, cold winters. Electricity is the primary source of heating, and consumption rises sharply between October and March.

While a standard utility bill for an 85m² flat might average 1,500–2,500 NOK in summer, this can easily surge to 4,000 NOK or more during winter. This seasonal fluctuation must be factored into any assessment of tenant affordability.

A key takeaway for investors is that Norwegian tenants are accustomed to these high, variable utility costs and budget accordingly. This means that well-insulated, energy-efficient properties are highly attractive and can command a rental premium, offering a clear opportunity to add value and enhance yield.

The Investor's Bottom Line

For those considering a permanent relocation or a serious investment, the financial framework in Norway is refreshingly straightforward. A comprehensive guide on buying a house in Norway can provide deep insight into the market, legal procedures, and financing.

From an investor's standpoint, the tax system is a significant advantage. Norway applies a flat 22% tax rate on net rental income, a simple and predictable model compared to the complex tiered systems in many other countries.

Crucially, foreign ownership is clear-cut, with no major restrictions preventing UK citizens from purchasing property. To explore financing options, our guide on second home mortgage requirements for international buyers is an excellent starting point. This combination of strong tenant demand, simple taxation, and open foreign ownership solidifies Norway’s position as a premium, stable market for property investment.

Understanding the Real Cost of Living: Food, Transport, and Lifestyle

Beyond the headline costs of rent and utilities, it is the day-to-day expenditure that truly defines life in Norway. For a property investor, understanding these expenses is a practical necessity. It directly shapes a tenant's disposable income, which in turn determines their ability to comfortably meet the requested rent. A clear understanding of the Norway living cost at this granular level reveals why certain property locations and features command a premium.

The high price of food is a reality for every Norwegian household. This is not incidental; it is a direct consequence of the country's reliance on imports, strong agricultural protectionism, and high labour costs. These factors combine to push grocery prices to be among the highest in Europe—a stark contrast to many emerging markets where daily costs are significantly lower.

Breaking Down Food and Grocery Bills

For tenants, the financial disparity between cooking at home and dining out is enormous. A weekly grocery shop for a single person typically falls between 700 and 1,200 NOK. For a family of four, that figure climbs to 2,500 to 4,000 NOK. These figures underscore the importance of a well-equipped kitchen in a rental property; home cooking is the primary strategy for managing household budgets.

- Dining Out: An inexpensive restaurant meal will cost 200-250 NOK per person.

- Mid-Range Restaurant: A three-course dinner for two at a reputable establishment will easily exceed 1,000 NOK.

- Cooking at Home: By contrast, a home-cooked meal costs a fraction of that, making it the default choice for most residents.

This cost differential directly influences tenant preferences. Properties within easy walking distance of affordable supermarkets like Rema 1000, Kiwi, or Coop Extra are highly sought-after. It is a subtle but powerful factor when evaluating a property’s practical appeal.

Navigating Transport Costs

Transport is another critical budget item with a significant impact on property demand. While Norway's cities boast excellent public transport, the financial trade-off between using it and owning a car is one every household must carefully consider.

The decision between public transport and car ownership is a major financial crossroads for Norwegian households. For an investor, this means properties with excellent public transport links are not just a convenience—they are a core financial asset for potential tenants, widening the pool of eligible renters.

A monthly public transport pass in a major city like Oslo costs around 850 NOK and provides unlimited travel on buses, trams, and ferries. It is a predictable, manageable expense.

Car ownership, however, presents an entirely different financial picture. The initial purchase price of a vehicle is exceptionally high, due to steep import taxes. Furthermore, fuel prices are consistently among the most expensive in Europe, often exceeding 22 NOK per litre. When insurance, road tax, and potential toll roads are added, the monthly cost of running a car can easily surpass 4,000-5,000 NOK—before accounting for depreciation.

This reality makes properties in walkable city centres or near major transport hubs exceptionally valuable. In contrast, markets with lower vehicle costs, such as those detailed in our analysis of the cost of living in Turkey, present a different set of mobility-related investment considerations. For Norway, proximity to transport is paramount.

Comparing Regional Costs: Oslo Versus Emerging Cities

For any astute property investor, it is a fundamental principle that a national market is never a single entity. While Oslo is undeniably Norway's economic engine, a deeper analysis of the Norway living cost reveals a different story—and compelling opportunities—in its other major cities. An effective strategy should not simply chase the highest rents in the capital; it must identify the optimal balance between property acquisition cost and the rental income it can generate.

Experienced investors understand that the largest rent cheque does not always equate to the best return on investment (ROI). Emerging hubs like Bergen, Trondheim, and Stavanger offer a different calculation entirely. Here, property prices are typically lower than in Oslo, meaning the initial capital outlay is smaller. This can lead to healthier rental yields, even if the monthly rent is less than what a prime Oslo apartment might command.

Oslo: The High-Cost Anchor

Oslo operates in a league of its own. It has the highest property values and rental rates in the country, a direct result of being the national centre for government, finance, and major corporate headquarters. For an investor, this creates a deep and reliable pool of high-earning tenants, which is a significant advantage for minimising vacancies.

The trade-off is the substantial cost of entry. The high purchase prices mean that even with premium rents, rental yields can be compressed. Investing in Oslo is often a strategy focused on long-term capital growth rather than immediate, high-percentage cash flow. It is a mature, stable market, so investors should not expect the rapid yield growth that might be found in up-and-coming areas.

Emerging Cities: A Focus on Yield

In contrast, cities like Trondheim and Bergen present a more balanced investment case. They are not merely smaller, cheaper versions of Oslo; each has a powerful economic engine that fuels its local property market.

Trondheim: As Norway’s undisputed hub for technology, research, and higher education, it has a constant influx of students, academics, and tech professionals seeking accommodation. This creates strong demand for smaller, centrally located flats, which can be acquired for a fraction of their Oslo equivalents. A lower entry price combined with strong, steady rental demand is a classic formula for an attractive rental yield.

Stavanger: Traditionally the heart of Norway's oil and gas industry, Stavanger's property market can be more cyclical, tracking the global energy sector. While this introduces a higher risk profile, it can also deliver outsized returns during economic booms for investors who time their market entry effectively.

Bergen: With its diverse economy built on the maritime, aquaculture, and tourism sectors, Bergen’s rental market is remarkably stable. It offers a solid middle ground between the extreme costs of Oslo and the more specialised economies of other cities.

To gain a clearer picture of how these cities compare for both tenants and investors, it is helpful to examine the data side-by-side. The table below compares the cost of living indices across Norway’s three largest cities.

Cost of Living Comparison Across Major Norwegian Cities (2026)

| City | Overall Cost Index | Rent Index | Groceries Index | Local Purchasing Power Index |

|---|---|---|---|---|

| Oslo | 88.5 | 38.2 | 87.1 | 95.4 |

| Bergen | 81.2 | 29.5 | 79.8 | 98.6 |

| Trondheim | 79.5 | 27.8 | 78.5 | 104.2 |

As the data from credible economic bodies shows, while Oslo has the highest overall costs and rent, its local purchasing power is actually lower than in Bergen and Trondheim. This suggests that tenants in these emerging cities may have more disposable income, making them reliable renters even if the headline rent figure is lower than in the capital. For an investor, Trondheim's combination of the lowest rent index and the highest purchasing power is particularly noteworthy.

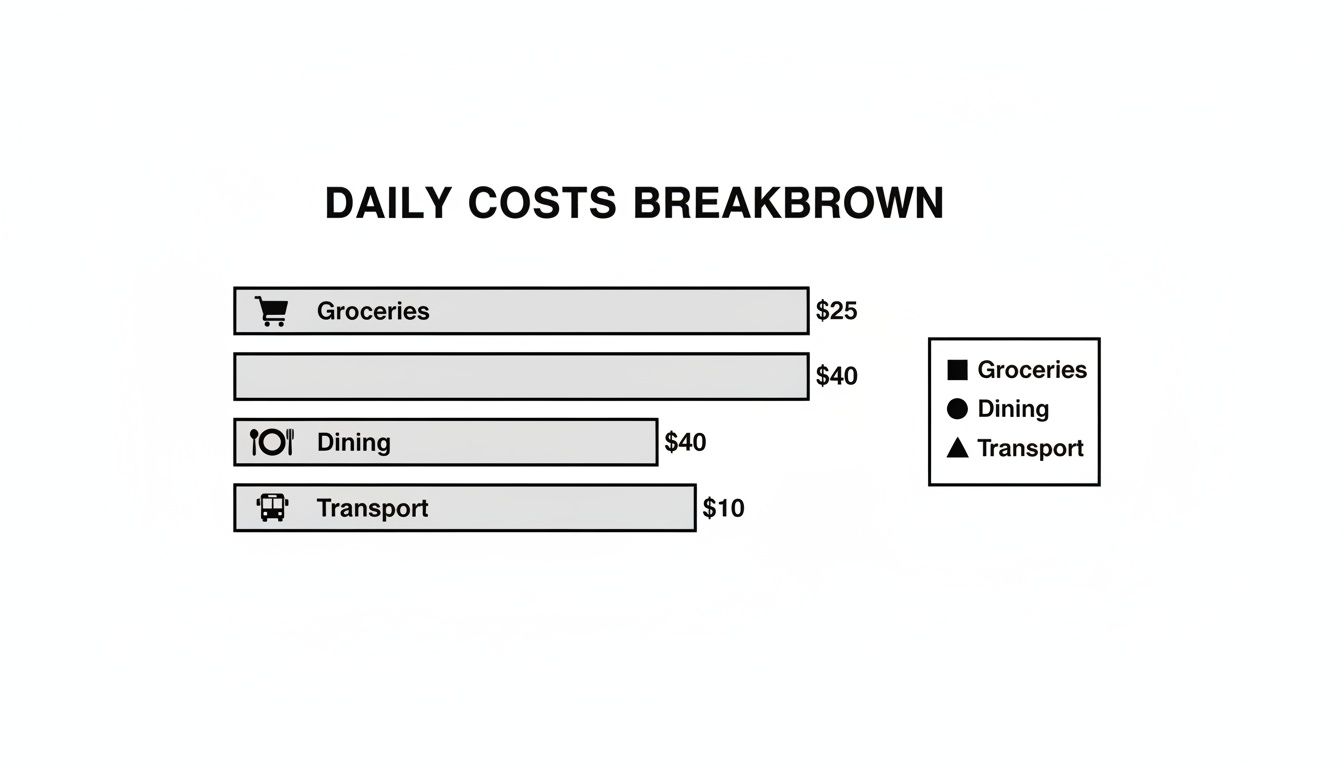

A major variable in any tenant's budget is the cost of daily essentials. Monitoring the outlook for food and energy prices can help forecast how household expenses might evolve, affecting rental affordability across all Norwegian cities.

The chart below provides a snapshot of what these daily costs can look like. While there are slight regional differences, these expenses form a significant part of any tenant's monthly budget, regardless of location.

These figures confirm that while Norway is an expensive country across the board, minor variations from city to city can make a tangible difference to a tenant's disposable income and their rental capacity.

Investor Takeaway: Diversifying a portfolio within Norway can be a powerful strategy. Consider a balanced approach: a blue-chip asset in Oslo for long-term capital growth, combined with higher-yielding properties in a city like Trondheim or Bergen for stronger monthly cash flow. This allows you to capture both stability and growth potential, creating a more resilient portfolio.

Understanding Taxes, Social Security and Hidden Costs

For any UK property investor assessing opportunities in Norway, a full picture of returns requires looking far beyond rent and utility bills. True net profit is ultimately determined by taxes, the social security system, and other costs that may not be immediately obvious. Mastering these details is what separates accurate financial forecasting from unwelcome surprises that can erode your bottom line.

A significant driver of Norway's high living costs is its comprehensive social contract, funded by a progressive tax system. While this can mean high income tax for residents, the tax rules for property investors are refreshingly simple—a key reason why foreign capital is drawn to the country.

The Tax Framework for Property Investors

As a buy-to-let investor, the primary concern is the tax on rental income. Fortunately, Norway's approach is remarkably straightforward. A flat tax rate of 22% is applied to your net rental income.

This figure is calculated after deducting all allowable running costs, such as property maintenance, insurance, and municipal fees. This makes financial modelling highly predictable.

The same flat 22% rate also generally applies to capital gains upon the eventual sale of the property. This simple, one-rate system is a world away from the complex, tiered tax regimes found in many other European countries, offering a level of clarity that international investors value.

For a UK investor, this means you have a clear picture of your tax liabilities on both rental cash flow and future capital appreciation from day one. This predictability simplifies ROI calculations and removes much of the uncertainty associated with foreign property investment.

Of course, it is also important to understand how this fits into your wider portfolio. For more on this, our guide on capital gains tax on foreign property explains how gains from your Norwegian assets might be treated back in the UK.

Social Security and Hidden Property Costs

As a non-resident landlord, you will not be paying Norwegian income tax or social security contributions yourself. However, it is vital to understand what those contributions fund. Your tenants will pay National Insurance Contributions that support a world-class public healthcare system, generous pensions, and other social benefits.

This robust safety net is a huge part of what makes Norway such a stable and attractive place to live and work. For an investor, it directly contributes to the high-quality, reliable tenant pool.

Beyond income tax, there are a few other 'hidden' costs to incorporate into your budget:

- Municipal Property Tax ('Eiendomsskatt'): This is a local tax set by the municipality where the property is located. Rates vary significantly from one city to another, so researching the specific rate for your target area is essential.

- One-Off Purchase Costs: Acquiring property in Norway involves significant one-off transaction fees. The stamp duty ('dokumentavgift') is a substantial 2.5% of the property’s market value, a major expense to factor into your initial investment calculation.

- Annual Fees: If you own an apartment, you will almost certainly pay into a homeowners' association ('sameie'). These fees cover the upkeep of communal areas, building insurance, and sometimes even heating or internet, so they must be included in your operating cost analysis.

Sample Budgets and Key Investor Takeaways

To truly understand the market, it is fundamental to understand your tenants’ finances. This is essential for setting appropriate rent levels and judging affordability.

Let's break down the numbers for common tenant profiles in a major city like Oslo. While these are benchmarks—individual spending habits differ—they paint a clear picture of typical household budgets.

Sample Monthly Budget for a Single Professional

A single professional in a centrally located one-bedroom flat represents a core tenant for any buy-to-let investor in Norway. Their budget is a classic balance between a strong salary and high essential costs.

| Category | Estimated Monthly Cost (NOK) | Notes |

|---|---|---|

| Rent (1-Bed City Centre) | 14,000 | Premium for a modern, well-located flat. |

| Utilities (incl. Winter Avg.) | 2,500 | Higher due to electricity for heating; includes internet. |

| Groceries | 4,000 | Assumes mostly home-cooking with occasional splurges. |

| Transport Pass | 850 | Relies on Oslo's efficient public transport system. |

| Leisure & Social | 3,500 | Dining out, gym membership, and other activities. |

| Total Estimated Outgoings | 24,850 | Leaves room for savings from a typical professional salary. |

Sample Monthly Budget for a Young Couple

Young professional couples often seek more space, typically a two-bedroom apartment. With a combined income, they have greater flexibility, but their overall expenditure is naturally higher.

| Category | Estimated Monthly Cost (NOK) | Notes |

|---|---|---|

| Rent (2-Bed Apartment) | 19,000 | Located in a desirable neighbourhood, not prime city centre. |

| Utilities (incl. Winter Avg.) | 3,500 | Higher consumption for a larger space and two people. |

| Groceries | 7,000 | Reflects food costs for two adults. |

| Transport Passes (x2) | 1,700 | Two monthly passes for commuting and leisure. |

| Leisure & Social | 5,000 | More frequent dining out and social activities. |

| Total Estimated Outgoings | 36,200 | Comfortably managed with dual professional incomes. |

Key Investor Takeaways

These budgets reveal critical insights for UK investors. Far from being a negative indicator, Norway's high cost of living is a key ingredient in what makes its property market so stable and lucrative.

A detailed 2026 forecast confirms this, showing a wide range of expenses: a single person's annual costs are estimated at $43,752 USD, a couple's at $60,816 USD, and a family's at $85,062 USD. While energy prices have pushed living costs up by 12% since 2022, a 10% rise in wages has kept affordability in check. This comprehensive Norway budget guide breaks it down further, also noting the strong yields available in the short-term rental market.

High Living Costs Sustain Rental Demand: The combination of expensive property and substantial one-off purchase costs (like the 2.5% stamp duty) keeps a significant portion of the population renting for longer. This creates a deep and consistent pool of high-quality tenants, reducing vacancy risk for investors.

This financial pressure on residents reinforces the demand for good rental properties, especially in urban hubs where high-paying jobs are concentrated. For an investor, this dynamic provides a solid foundation for reliable, long-term rental income.

The data shows that even with Norway’s steep living expenses, tenants have the financial capacity to meet premium rents. That stability is exactly what an investor should seek. To understand how these costs and potential rental income translate into real profit, familiarise yourself with the essentials of how to calculate your return on an investment property.

Ultimately, the Norwegian market offers a compelling case for portfolio diversification. It combines a stable, high-income tenant base with clear tax laws and strong economic fundamentals, making it a premium destination for UK investors seeking reliable returns outside their domestic market.

Frequently Asked Questions for UK Investors

When exploring a new market, particularly one as unique as Norway, questions are inevitable. For UK investors weighing the high Norway living cost against potential returns, clarifying financial and legal details is the most critical step. Here are straightforward answers to the most common queries.

Is Buying Property in Norway a Good Investment for UK Investors?

Yes, for reasons directly linked to the country’s high-cost, high-salary economy. Because Norwegian salaries are strong, there is a deep pool of reliable, professional tenants who can comfortably afford premium rents. This creates a remarkably stable buy-to-let environment and significantly lowers the risk of rental arrears.

While day-to-day costs in Norway are steep, property prices in cities like Oslo can still be more accessible than in prime London postcodes, suggesting good potential for capital growth. For a UK investor, Norway offers a powerful combination of strong rental income and a valuable hedge against volatility in the UK market, making it an excellent candidate for portfolio diversification.

What Are the Main Taxes for a Foreign Property Investor in Norway?

The Norwegian tax system is refreshingly straightforward for property investors. Your primary liability will be a flat tax of 22% on your net rental income. This is calculated on your gross rent after deducting allowable costs like maintenance, insurance, and municipal fees.

When you eventually sell, any capital gain is also typically taxed at the same 22% rate. An annual wealth tax might apply if the net value of your Norwegian assets exceeds a certain threshold, but for a single property, this is often modest. As always, seeking personalised advice from a local tax specialist is a prudent step.

Which Norwegian City Offers the Best Rental Returns?

The optimal city depends on your investment objectives. Oslo delivers the highest absolute rents and has the most robust tenant demand. However, with the highest entry prices, your initial rental yield can be compressed.

For those hunting higher percentage yields, it is worth looking closely at emerging hubs like Bergen and Trondheim. These cities have strong local economies, top-tier universities, and a growing population of young professionals, but property remains more affordable than in the capital. Stavanger, with its dominant energy sector, can also offer high returns, though its market is naturally more tied to the global economic cycle.

Are There Restrictions on Foreigners Buying Property in Norway?

No, there are no meaningful restrictions that prevent foreign nationals, including UK citizens, from buying property in Norway. The entire process is transparent, secure, and well-regulated.

You will need to obtain a Norwegian national identity number (a D-number) to finalise the purchase, but this is a standard administrative step. Unlike some other European countries with complex rules for non-residents, the Norwegian system is designed to be open and welcoming to foreign investors.

At World Property Investor, we provide the in-depth analysis and data you need to explore global real estate opportunities with confidence. Discover market guides, investment strategies, and expert advice to build your international portfolio. Learn more at worldpropertyinvestor.com.