Slovenia’s residential market delivered one of the more revealing signals in Europe recently. Residential sales fell to 8,124 dwellings in 2024, down 21.13% year on year, yet prices didn’t break according to Global Property Guide’s Slovenia market data. For investors, that matters more than the usual lifestyle pitch about lakes, ski towns and Adriatic views.

A market where activity falls but pricing holds is rarely simple. It usually means supply is constrained, sellers are not under broad distress, and buyers still want access even if affordability has worsened. That combination makes property for sale in Slovenia interesting for capital preservation investors, selective income buyers, and foreign purchasers who want a foothold in a smaller Eurozone market that sits between the pricing intensity of Austria and the patchiness often found in looser emerging markets.

Slovenia also rewards discipline. You can’t analyse it as a pure yield market, and you can’t approach it with a short-term speculative mindset. Foreign buyers, especially from the UK, need to think about tax structure, financing friction, liquidity by micro-location, and whether a property works as a long-term rental, a holiday let, or a future personal-use asset. Investors comparing options across the continent often start with broader European property buying opportunities and then narrow down to places where legal certainty and scarcity support values. Slovenia deserves to be in that narrower list.

An Introduction to the Slovenian Property Market

Slovenia isn’t a bargain-bin frontier market, and that’s precisely why it deserves attention. It’s better understood as a small, mature, supply-constrained Eurozone market where location quality matters far more than headline volume.

The key signal from recent data is not merely that sales dropped. It’s that lower turnover did not force widespread repricing. In many countries, a sharp fall in transactions would trigger inventory build-up and price cuts. In Slovenia, the pattern looks different because sellers appear able to wait, especially in prime urban and lifestyle locations.

Why serious investors look beyond the postcard image

Foreign buyers often arrive through the tourism narrative first. Lake Bled, Piran, the Julian Alps and Ljubljana all market themselves naturally. But investment logic starts elsewhere.

Slovenia offers three features that discerning buyers tend to value:

- Eurozone stability: Currency risk is lower for euro-based investors and more manageable for sterling-based buyers than in non-euro European markets.

- Compact geography: The capital, coast, alpine zones and secondary cities are accessible enough to create a diversified domestic demand base.

- Quality over scale: The market is small, which limits liquidity in weaker locations, but scarcity can support better assets over a long hold period.

Investor lens: In Slovenia, the asset matters more than the story. A mediocre unit in a weak submarket won’t be rescued by the country’s overall appeal.

That creates a market with a narrow margin for error. If you buy well, Slovenia can function as a defensive real asset with lifestyle optionality. If you buy badly, low turnover can trap you in a thin resale market.

What actually makes Slovenia different

Compared with larger Western European markets, Slovenia is less liquid and less institutionally crowded. Compared with more promotional emerging markets, it’s more grounded in real local demand and EU legal infrastructure. That middle ground is attractive for buyers who want steady long-term positioning rather than high-risk financial strategies and rapid resale.

For UK investors in particular, the opportunity is real but the execution risk is underappreciated. The tax and financing issues are not side notes. They sit at the centre of whether a Slovenian purchase performs well after costs.

Understanding Slovenia's Market Fundamentals in 2026

The Slovenian market’s resilience comes down to one word. Scarcity.

In 2024, prices for newly built dwellings rose by 9.46% year on year, while only 5,165 dwellings were completed, according to TheGlobalEconomy’s Slovenia house price index data. The same source notes a stable price corridor of roughly €3,000 to €3,500 per square metre in regional and secondary locations, and €5,000+ per square metre in Ljubljana and prime segments. For investors, that’s the anchor around which underwriting should be built.

Supply is the real market driver

Many investors spend too much time asking whether Slovenia is “hot” and too little time asking whether supply can respond. At present, it doesn’t appear able to respond quickly.

That matters because in a rising-rate or affordability-constrained environment, markets usually correct through one of two channels. Prices fall, or supply remains too tight for meaningful repricing. Slovenia increasingly looks like the second case.

Three structural forces stand out:

- Limited completions: The national completion figure remains modest relative to what prime areas need.

- Prime-location scarcity: Ljubljana and the strongest tourism zones don’t have abundant easy-to-develop stock.

- Owner reluctance to sell: Existing owners with favourable historic mortgage rates often have little incentive to move.

Why falling turnover hasn’t broken values

Slovenia stands apart from more speculative markets. When sales slow in a debt-fueled, oversupplied market, prices can unravel quickly. In Slovenia, the available evidence suggests the transaction slowdown reflects affordability pressure and selective buyers more than broad forced selling.

The result is a market that can feel weak on activity and firm on pricing at the same time.

Buyers now have more room to negotiate than they did at the peak, but they shouldn’t mistake that for a distressed market.

That distinction is important for valuation. Investors seeking a deep-discount strategy may struggle. Investors seeking risk-adjusted entry into constrained stock may find the current phase more attractive.

What that means for portfolio strategy

Slovenia sits in an interesting position between saturated and volatile markets. In heavily traded Western cities, yields can be compressed by institutional demand. In looser emerging markets, pricing can move quickly but legal, financing or political risk is often higher.

Slovenia offers a different profile:

| Market type | Typical investor challenge | Slovenia’s relative position |

|---|---|---|

| Established Western Europe | High entry pricing and compressed returns | More selective and less crowded |

| Volatile emerging markets | Weaker legal certainty and sharper cycles | More stable and defensive |

| Small supply-led markets | Liquidity can be patchy | This is Slovenia’s main trade-off |

For investors scanning a wider property market forecast for 2025 and beyond, Slovenia fits best as a medium-liquidity, long-hold market. It isn’t the place for rapid turnover. It is a market where scarcity can preserve value if you stay disciplined on location, building quality and tenant demand.

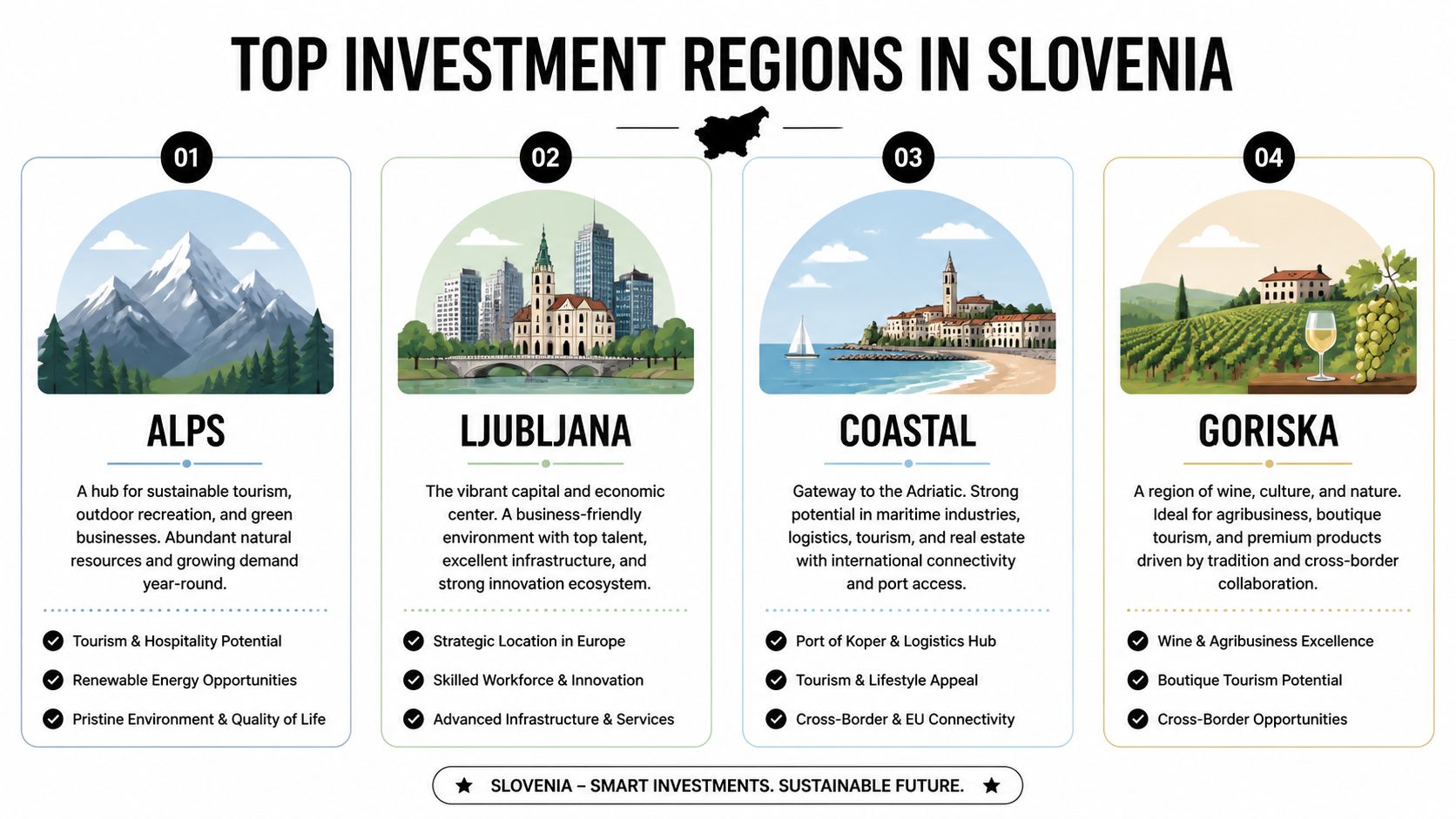

Where to Buy Property in Slovenia Top Investment Regions

Location choice in Slovenia is not just about taste. It’s about matching the asset to the income stream you want. A flat in Ljubljana serves a different purpose from a holiday unit on the coast or an alpine apartment aimed at seasonal tourism.

Ljubljana for resilience and exit liquidity

Ljubljana is the most institutional part of the Slovenian residential market. It attracts professionals, students, international staff and domestic buyers seeking the deepest employment base in the country.

For investors, the city’s main strengths are usually:

- Better resale depth: More buyer profiles support eventual exit.

- Long-term rental demand: Professionals and students underpin occupancy.

- Capital preservation logic: Prime stock tends to defend value better than peripheral regional assets.

The trade-off is straightforward. Entry pricing is higher, so your initial yield is usually tighter. Ljubljana works best for buyers who prioritise quality, tenant depth and future liquidity over maximum headline income.

Coastal Slovenia for lifestyle-led yield plays

Piran and Portorož are the obvious names here. Coastal property tends to attract foreign lifestyle buyers, second-home demand and short-stay guests.

This region suits investors who accept that holiday-let income is operational, not passive. Performance depends on management quality, seasonality control, pricing discipline and regulatory awareness. The appeal is strong, but so is competition for the best-located stock.

The market logic is simple. Coastal units can outperform on gross income in good periods, but they also carry more volatility than core urban rentals.

A coastal purchase should be underwritten first as a business, second as a trophy asset.

Julian Alps for premium tourism with seasonality risk

Bled and Kranjska Gora sit in the premium alpine bracket. These areas appeal to buyers looking for dual-use property. Part investment, part personal enjoyment.

The attraction is year-round tourism potential. The risk is that revenues depend heavily on maintaining occupancy, service standards and online visibility. A well-located alpine property can command attention. A mediocre one can become expensive to carry.

This region tends to suit investors who want:

- A defensible lifestyle asset

- Potential short-term rental upside

- A longer holding period with personal-use flexibility

Maribor and emerging regional value markets

Maribor deserves attention from value-seeking investors, but it requires realism. It won’t behave like Ljubljana, and it shouldn’t be priced in your mind as if it will. The market can offer lower entry points and potentially better cash yield characteristics, but weaker liquidity and thinner tenant depth are part of the package.

The same is true of smaller regional and tourism-adjacent markets such as the Soča Valley. They can work well for specialised buyers who understand local demand patterns. They are less forgiving for remote investors buying on narrative alone.

Slovenian Property Investment Regions at a Glance (2026)

| Region | Avg. Price/m² (Apartment) | Gross Rental Yield (Est.) | Best For |

|---|---|---|---|

| Ljubljana | Higher end of the national market, especially in prime areas | Moderate | Long-term lets, capital preservation, easier resale |

| Coastal Slovenia | Premium pricing in top sea-facing and old-town areas | Moderate to strong gross potential, but variable | Holiday lets, lifestyle investors |

| Julian Alps | Premium in the best tourism micro-locations | Variable, dependent on occupancy and operations | Dual-use homes, premium short stays |

| Maribor and regional value markets | Lower than Ljubljana and prime coast | Potentially attractive on paper, but market-specific | Value buyers, higher-risk investors |

A practical way to compare them is to ask a single question. Are you buying cash flow, stability, or optionality?

Investors looking for broader best places to buy rental property internationally often focus too much on yield rankings. In Slovenia, that can be misleading. The best region isn’t the one with the highest projected gross return. It’s the one whose demand profile, liquidity and operating burden align with your actual holding plan.

Foreign Ownership Rules and Property Taxes

Foreign buyers can purchase in Slovenia, but the route and tax outcome depend heavily on nationality and ownership structure. Such intricacies are often overlooked by generic guides. They describe the purchase process in broad terms but don’t address the post-Brexit complications that can materially alter returns for UK investors.

Why UK buyers need to plan before they bid

For British investors, Slovenia is no longer a simple extension of an EU property search. Structuring matters from the outset.

According to Green-Acres’ Slovenia investor guidance, ownership via a UK limited company or another holding structure can improve after-tax yields by 15–25% by optimising the interaction between Slovenian acquisition and rental taxes and changing UK rules affecting non-doms and capital gains. That is a significant difference in net performance, especially in markets where gross yields are not exceptionally high.

The same source also notes that UK buyers are often dealing with a mix of Slovenian and UK tax considerations, including Slovenian acquisition tax in the 3% to 4% range and rental income tax in the 10% to 15% range, alongside UK-side changes. The headline lesson isn’t that one structure is always best. It’s that buying personally without modelling the tax outcome can be expensive.

Practical rule: If you’re a UK buyer, speak to both a Slovenian property tax adviser and a UK cross-border tax specialist before signing anything. Not after.

The real issue is tax interaction, not just tax rates

A discerning investor doesn’t only ask, “What tax will I pay in Slovenia?” The more useful question is, “How does Slovenian taxation interact with my home-country position, financing, income extraction and eventual disposal?”

That’s especially relevant if you fall into one of these groups:

- UK resident investor: You need to understand how rental income and disposal proceeds are treated across both systems.

- Buyer using borrowed capital from outside Slovenia: Interest costs and ownership form can alter the economics materially.

- Family office or legacy buyer: Succession planning may matter as much as current-year income.

Main tax points to review before purchase

Precise tax treatment should always be confirmed professionally, but your pre-offer checklist should include:

- Acquisition taxes: Understand whether the transaction falls into the relevant Slovenian acquisition tax framework and how that affects all-in entry cost.

- Rental income treatment: Clarify the tax basis, deductible costs and whether ownership through an entity changes your after-tax outcome.

- Exit taxation: Consider the future disposal route before purchase, not at sale.

- Cross-border reporting: Make sure the ownership structure is workable administratively, not just theoretically efficient.

A large number of foreign buyers focus on the asset first and structure second. That order often works in domestic markets. It’s the wrong order here.

For investors reviewing broader capital gains tax on foreign property, Slovenia should be treated as a market where tax design is part of deal selection. The right property in the wrong structure can turn a sound investment into a mediocre one.

The Slovenian Property Buying Process Step by Step

The Slovenian transaction process is orderly, but foreign buyers still need a disciplined sequence. Mistakes usually happen when purchasers treat reservation, due diligence and registration as informal steps. They aren’t.

Step one to three

Search and shortlist properly

Use a licensed local agent, but verify everything independently. Listing language, renovation quality and legal status don’t always align neatly.Submit a formal offer

In practice, serious buyers move from informal discussion to written terms quickly. Price is only one part of the negotiation. Completion timing, included furnishings and access for survey or inspection also matter.Sign a preliminary agreement if required

This stage often secures exclusivity while both parties prepare the main contract. Read every obligation carefully, especially around deposits, completion deadlines and what happens if title issues emerge.

Due diligence is where foreign buyers protect themselves

The most important work happens before completion, not on completion day.

Your adviser should check:

- Land register status: Confirm ownership, liens, easements and registration consistency.

- Planning and use: Make sure the current use matches what you intend to do with the property.

- Building condition: Older stock can carry hidden capital expenditure risk.

- Short-let suitability: Don’t assume a tourist area automatically means operational freedom.

Buy the legal reality, not the listing description.

Contract, notary and registration

Once due diligence is complete, the main sale contract is signed and notarised where required. Funds then move through the agreed mechanism, and the ownership change is entered in the land register.

For foreign buyers, process discipline matters most. Notaries and agents facilitate the transfer, but they do not replace independent legal review. If anything in the chain feels rushed, slow it down.

A broader how to buy property abroad guide is useful for framing the international process, but in Slovenia the practical details around title, municipal compliance and intended use deserve local review.

For a visual overview of the process, this walkthrough is useful:

Budget for the purchase, not just the price

A common foreign-buyer error is focusing on acquisition price and underestimating soft costs. Even where the legal process is straightforward, professional fees, translation, document handling, tax administration and post-completion setup all add friction.

Build your acquisition plan around three buckets:

| Cost bucket | What it covers | Why it matters |

|---|---|---|

| Transaction | Legal, notary, agent, registration | Affects total entry basis |

| Compliance | Tax setup, translation, filings | Often overlooked by overseas buyers |

| Operational | Insurance, furnishing, initial works | Determines how quickly the asset can perform |

The cleanest transactions tend to involve buyers who already know their intended use, ownership vehicle, banking route and management plan before they place the offer.

Financing a Property Purchase in Slovenia

Foreign investors should treat Slovenian financing as a constraint first and an opportunity second. That sounds blunt, but it’s the right starting point.

According to Properstar’s Slovenia buying guidance, Slovenian banks typically lend only 50–60% loan-to-value to non-residents. The same source notes that gross holiday-let yields of 6–8% can compress to net yields of 3–4% after financing costs, taxes and realistic occupancy, with occupancy and RevPAR in tourist zones becoming more volatile since 2024. That single adjustment changes the investment case completely.

Why leverage works differently here

Many UK buyers arrive with a buy-to-let mindset shaped by a deeper mortgage market. Slovenia doesn’t always support that approach cleanly for non-residents.

The practical consequences are immediate:

- More equity is required upfront

- Debt-service cover matters more

- Short-term rental volatility becomes harder to absorb

- Return on equity may disappoint if financing is poorly structured

In other words, the issue isn’t just whether you can get a loan. It’s whether the financing terms still leave the property attractive after stress testing.

Stress-test the income, not the brochure

A holiday let in Piran, Bled or the wider alpine belt may look compelling at the gross level. But gross yield is only the top line. Net return depends on vacancy periods, management, cleaning, maintenance, platform costs, local taxes and debt costs.

If your Slovenian deal only works on optimistic occupancy, it doesn’t work.

A simple underwriting framework is more useful than a promotional yield number:

| Underwriting layer | What to ask |

|---|---|

| Revenue | What happens if occupancy is weaker than expected? |

| Costs | Are cleaning, turnover and maintenance fully included? |

| Finance | Does the property still cash-flow comfortably at available non-resident terms? |

| Tax | Has the ownership structure been modelled properly? |

Better financing routes for some foreign buyers

For many non-residents, the strongest financing route may not be a Slovenian mortgage at all. It may be external liquidity, a remortgage in the home country, or a purchase with less debt that accepts a lower but steadier return profile.

That’s particularly true for buyers who prioritise long-term control over maximizing financial power. If you need to move funds internationally as part of a purchase structure or family office transfer, it’s worth reviewing a practical guide for South African business transfers from Zaro because the operational lessons on cross-border transfer costs and planning are relevant well beyond South Africa.

The strongest Slovenian investments for foreign buyers are often the least exciting on paper. They are the ones that still perform when financing is conservative, occupancy is uneven and exit timing isn’t perfect.

Example Deals and Final Investor Takeaways

Two model purchases show how Slovenia should be approached. Not as a market for aggressive assumptions, but as one where asset quality and structure drive the actual outcome.

Example one in Ljubljana

Consider a compact, well-located apartment aimed at a professional long-term tenant. The investment case here is not built on explosive income growth. It’s built on steadier occupancy, a deeper tenant pool and better eventual resale prospects than many regional alternatives.

This sort of property suits investors who want:

- Lower operational burden

- More predictable tenancy patterns

- A stronger chance of liquid resale in a slower market

The risk is simple. If you overpay at entry, the income won’t rescue you quickly. Ljubljana works best when bought for durability, not excitement.

Example two in the Soča Valley or an alpine tourism zone

Now consider a small tourism-led property in a scenic region. This can outperform a city flat on gross income in strong periods, but only if marketing, guest operations and occupancy management are handled professionally.

That makes it a different business entirely. You’re not just owning real estate. You’re running a hospitality product with seasonality and reputational exposure. For owners trying to improve listing presentation and conversion, a practical guide to AI for real estate professionals can be useful because better visuals and digital marketing can materially affect short-let performance.

What the best Slovenia investors do differently

The most successful buyers in Slovenia usually share the same habits:

- They buy in strong micro-locations: City district, walkability, view and access matter.

- They underwrite net, not gross: Financing and tax are built into the first model.

- They hold for the long term: Slovenia is better suited to patient capital than quick flips.

- They assemble local expertise: Lawyer, tax adviser, manager and agent all matter.

Slovenia is a good market for investors who like controlled risk, not theatrical upside.

For foreign buyers, especially from the UK, the central question isn’t whether there is property for sale in Slovenia worth buying. There is. The key question is whether you can structure, finance and operate the asset in a way that preserves the advantages the market offers. When you do that well, Slovenia looks less like a speculative play and more like a carefully chosen European long-term holding.

If you’re comparing Slovenia with other international markets, World Property Investor publishes detailed country guides, rental yield analysis, tax breakdowns and buying advice to help you assess where a property fits within a wider portfolio.