You agree a price on an overseas property, transfer the deposit, line up local financing, and focus on the legal work. Then sterling moves against you before completion. The property hasn't changed. Your investment thesis hasn't changed. But your sterling cost has.

That's why serious international investors need to understand how to hedge currency risk as part of the property process, not as an afterthought. If you're buying abroad, the foreign exchange exposure starts well before title transfer and often lasts until the day you sell and bring proceeds home.

If you want a broader primer on the mechanics before applying them to property, Alpha Scala's comprehensive guide to hedging is a useful foundation. For the property side of the transaction itself, the practical issues usually begin once you move from research into an actual deal, which is where a detailed guide to buying property overseas becomes relevant.

Why Currency Risk Matters for Property Investors

A UK buyer looking at Portugal, Spain, France, Dubai, or an emerging European market usually starts with the headline numbers. Purchase price. Gross yield. Mortgage terms. Local tax. Management fees. Those matter, but FX often cuts across all of them.

The exposure is obvious at purchase. If your property is priced in euros and your wealth is in sterling, you're effectively long the property and long the euro until you complete. If sterling weakens in the meantime, your acquisition cost rises in pound terms. That changes your real entry price, your equity requirement, and your expected return.

The exposure doesn't stop there. Rental income arrives in the local currency. Repairs, taxes, service charges, and insurance may also sit in the local currency. When you eventually refinance or sell, the final sterling outcome depends partly on the exchange rate on that date, not just on the asset's local market performance.

Why the decision looks different now

The economics of hedging have shifted because interest rates have shifted. Russell Investments notes that the Bank of England cut Bank Rate to 4.75% in November 2024 and then to 4.5% in February 2025, while the ECB also cut rates through 2024 to 2025, which means the GBP-EUR forward points and hedging cost can materially differ from the spot rate story (Russell Investments on currency exposures).

That matters because many investors still think about hedging as a simple insurance decision. It isn't. The forward rate reflects the spot rate plus or minus the interest-rate differential between the two currencies. So the key question isn't only, “Will sterling rise or fall?” It's also, “What am I paying, or receiving, through carry to lock in certainty?”

Practical rule: Treat FX management as part of deal underwriting. If the currency move can materially alter your sterling return, it belongs in your investment model from day one.

Established and emerging markets create different FX problems

In established eurozone markets such as Spain or France, the risk is usually transparent. You can model euro purchase costs, euro rent, euro expenses, and euro sale proceeds with relative clarity.

In markets linked to the US dollar, such as Dubai through the dirham's peg, the risk feels different but doesn't disappear. A sterling investor still carries a sterling versus dollar-linked exposure. In more thinly traded or operationally complex emerging markets, currency management becomes less about precision and more about damage control. The legal and banking process may be slower, local costs may be less predictable, and timing mismatches become more common.

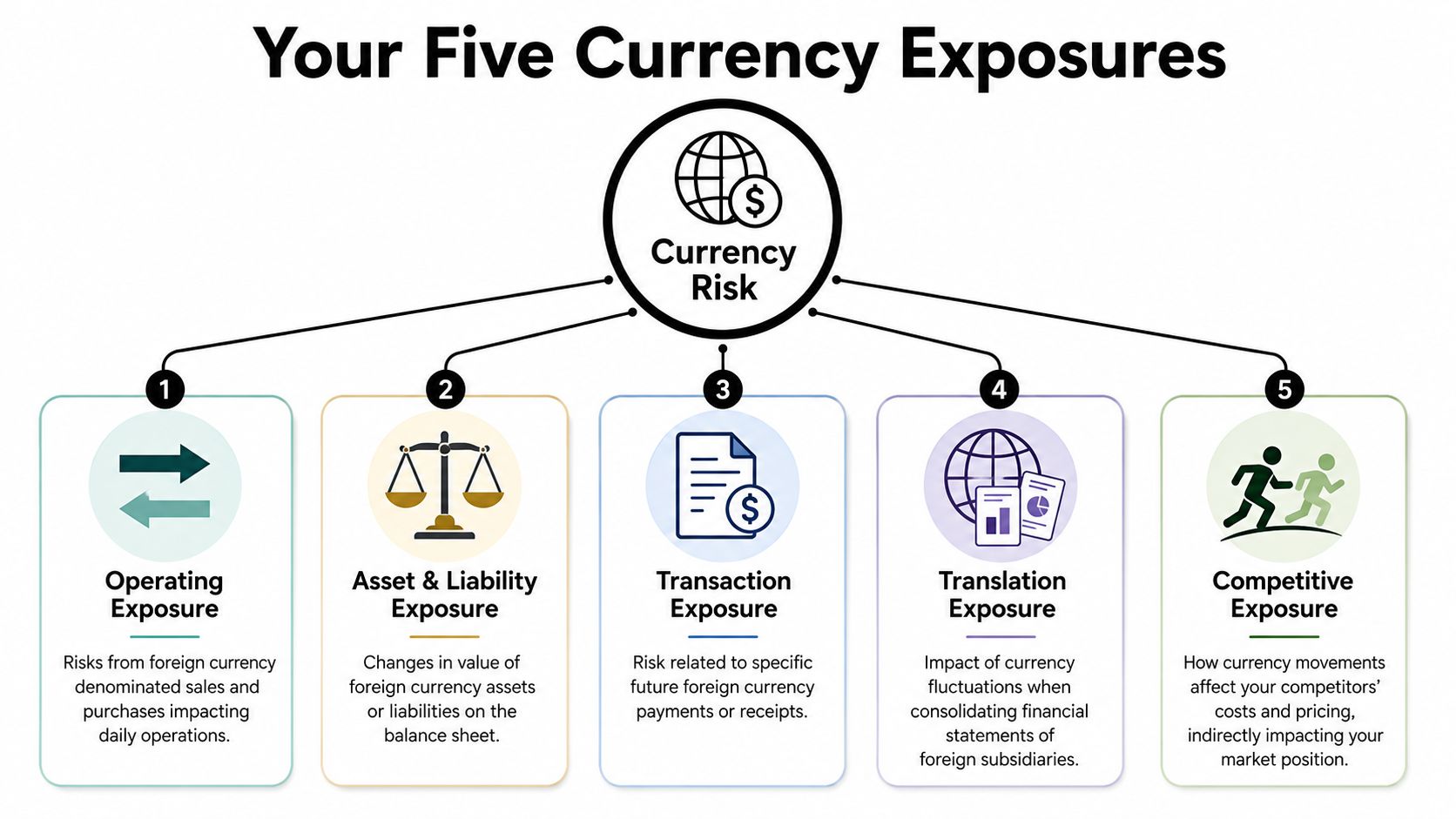

Identifying Your Five Key Currency Exposures

Most investors talk about “FX risk” as if it were one thing. In property, it's five separate exposures that appear at different moments in the investment lifecycle. If you don't separate them, you'll almost always hedge the wrong amount, for the wrong period, using the wrong tool.

Purchase price and deposit

This is the clearest exposure. You agree a foreign-currency price today, but completion happens later.

The danger sits in the gap between commitment and settlement. A reservation payment, deposit, staged construction payment, or final completion transfer all create transaction exposure. If your purchase is in euros and your capital base is in sterling, any adverse move in GBP/EUR before payment changes your effective cost.

Many UK buyers first look at specialist FX providers and mortgage structures. If you're financing part of the purchase locally, the shape of the exposure changes, which is why the debt side should be reviewed alongside buying an overseas property with a mortgage.

Foreign currency financing

A local mortgage can act as a partial hedge because the liability sits in the same currency as the asset. That's often called a natural hedge.

But it only helps if your income profile matches the debt. If you earn rent in euros and service a euro mortgage, that alignment can reduce the need to keep converting sterling each month. If your personal income remains in pounds and the rent is irregular or seasonal, you still carry repayment risk when the local cash flow falls short.

Rental income and remittance

Rent is where investors often overcomplicate things. You don't need to convert every receipt to sterling the day it lands.

If the property generates local expenses in the same currency, keeping part of the rent onshore can reduce conversion frequency and lower friction. In practical terms, your FX exposure is the amount you intend to repatriate, not necessarily the gross rent itself.

Don't hedge gross cash flow when your true exposure is net cash flow after local costs.

Operating costs

Management fees, tax, maintenance, insurance, utilities, refurbishment, and legal bills can all sit in the local currency. Investors often ignore this side because the ticket sizes feel smaller than the purchase price.

That's a mistake. A portfolio with regular foreign expenses can produce a steady drain on sterling returns if every payment requires a reactive spot conversion. In an established market with reliable contractors and invoices, this is manageable. In an emerging market, timing uncertainty can make it much harder to fix exact amounts in advance.

Capital repatriation and exit

The biggest FX event may come at the end. You sell in the local currency, pay local taxes and fees, discharge any debt, and decide when to convert the net proceeds back to sterling.

That creates asset and liability exposure and, for some investors with structures or consolidated reporting requirements, a form of translation exposure as well. There can also be a competitive exposure angle. If sterling moves sharply, UK buyers may become more or less competitive relative to euro or dollar investors bidding in the same destination.

A villa in the south of France and an apartment in Istanbul can both be good assets locally, but the path from local sale proceeds to sterling wealth is very different. That final conversion can enhance or erode years of operating performance.

A Practical Comparison of Hedging Instruments

For most property investors, the right tool depends on one question. Are you hedging a known future payment, an ongoing income stream, or a long-term structural exposure?

Stanford's treasury guidance describes forward contracts as agreements to buy or sell currency at a set future rate and notes that they're used to reduce volatility in cash flows and budgets. It also notes that when future cash flows are uncertain, firms may hedge only a fraction of the exposure or spread maturities across periods (Stanford guidance on foreign-currency hedging). For UK property investors, that's the practical starting point.

Currency hedging instruments at a glance

| Instrument | Best For | Pros | Cons |

|---|---|---|---|

| Forward contract | Known completion dates, mortgage repayments, planned remittances | Locks in a future rate, creates budget certainty, works well for defined dates and amounts | Removes upside if FX later moves in your favour, needs accurate sizing and timing |

| Currency option | Situations where timing or execution is uncertain | Protects against adverse moves while preserving some upside if FX improves | More complex, can be expensive, often less attractive for smaller private investors |

| Multi-currency account | Holding rent locally and paying local expenses | Reduces unnecessary conversions, improves cash management, simple operational benefit | Doesn't itself lock in a rate, so market risk remains |

| Local-currency borrowing | Assets financed and operated in the same currency | Creates a natural hedge between asset, debt, and sometimes rent | Doesn't remove all exposure, especially for equity, exit proceeds, or cash shortfalls |

| Sterling-hedged fund or ETF | Securities portfolios linked to property allocation decisions | Operationally simple and rolled professionally | Not a direct hedge for a physical property purchase or local property cash flow |

What works best for property investors

Forward contracts are usually the most practical instrument when the exposure is specific. A Spain completion date. A French mortgage repayment. A planned dividend or rent remittance. They work because the notional amount, direction, and settlement date can be matched to the underlying need.

Multi-currency accounts help with operations, not risk transfer. They're useful for receiving rent and paying local bills without converting every movement back into sterling. That can reduce friction, but it doesn't fix your exchange rate.

Local financing is often underused as a hedge. If the asset, debt, and income all sit in euros, you're not forced to inject sterling into every operating cycle. This is one reason many investors reviewing overseas rental income should look at liability currency as carefully as gross yield.

Where investors go wrong

The common error is using a short-dated financial hedge for a vague long-dated risk. If you haven't decided whether you'll hold a Portuguese apartment for rent, personal use, or sale, a clean hedge is hard to structure.

Another mistake is hedging gross asset value when what really needs protecting is a specific cash event. Property isn't a listed equity position with daily liquidity. The hedge should follow cash flow certainty, not abstract anxiety about the market.

A hedge works best when the amount, direction, and date all match the real exposure. Once any of those three become fuzzy, the risk of over-hedging rises quickly.

Established versus emerging market use cases

In the eurozone, forwards are straightforward because legal completion timetables and banking rails are generally predictable. In dollar-linked markets, local financing can do more of the heavy lifting because asset values and liabilities may already align around the same currency bloc.

In emerging markets, options can have conceptual appeal because they preserve flexibility. In practice, many private investors still prefer simpler tools and a lighter hedge ratio because the underlying transaction path itself is less certain.

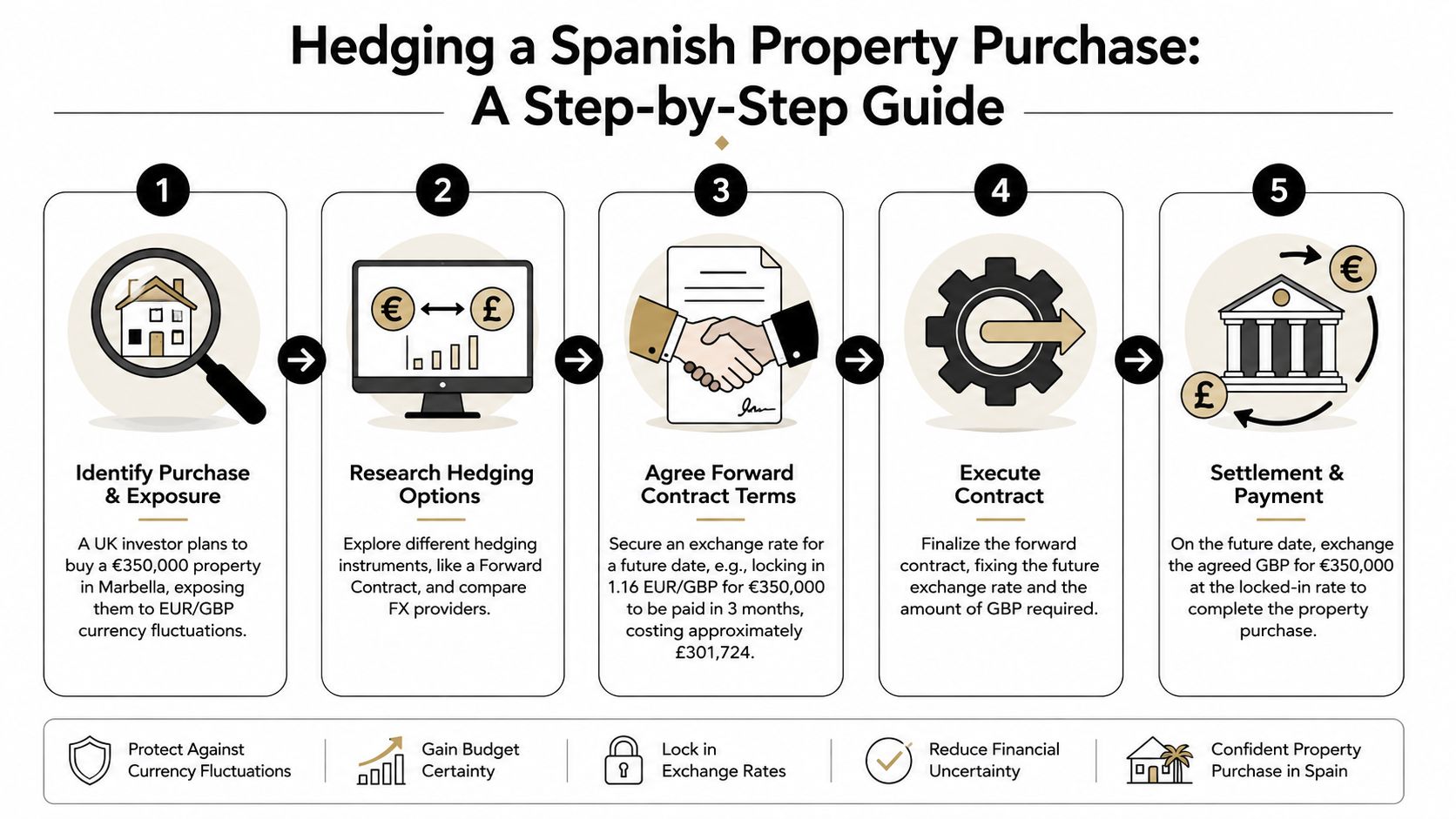

Worked Example Hedging a Property Purchase in Spain

A UK investor agrees to buy a €350,000 apartment in Marbella. Completion is expected in roughly three months. The investor's problem is simple. The purchase price is fixed in euros, but the capital available for completion is measured in sterling.

The infographic example uses a forward rate of 1.16 EUR/GBP for €350,000, costing approximately £301,724 in sterling terms. The exact market rate you receive will depend on timing, provider pricing, and prevailing forward points, but the logic is what matters.

How the hedge is structured

The investor books a forward contract with an FX provider. The contract specifies three things:

- Amount: €350,000

- Direction: Buy euros, sell sterling

- Date: Settlement aligned with the expected completion date

That converts an uncertain future sterling cost into a known one. The investor can then finalise legal, mortgage, and liquidity planning without guessing what GBP/EUR might do over the next few months.

For a buyer reviewing debt terms at the same time, local financing still matters. A hedge on the equity contribution should be assessed alongside the mortgage structure and current Spanish mortgage rate options.

What certainty is worth

If sterling weakens before completion, the forward will usually look smart in hindsight because it protected the budget. If sterling strengthens, the investor may feel they “lost” by not waiting for a better spot rate.

That's the wrong way to judge the decision. The point of the hedge wasn't to beat the market. It was to guarantee affordability and protect the underwriting assumptions made when the deal was approved.

The right benchmark for a property hedge isn't the best possible rate. It's whether the investment still works on the day cash is due.

When a partial hedge makes more sense

A full hedge isn't always the default. JPMorgan's investment guidance states that its strategic asset allocation is neutral at about 30% hedged for the relevant foreign equity allocation, leaving 70% unhedged (JPMorgan on currency hedging).

Property investors can borrow that logic without copying it mechanically. If your Spanish purchase is heavily debt-financed and your sterling liquidity is tight, a higher hedge ratio may be sensible because FX slippage could derail completion. If you have surplus liquidity and are comfortable with some market movement, a partial hedge can protect against a severe adverse move while leaving some upside if sterling improves.

A practical approach might look like this:

- Fully hedge the committed amount needed for completion.

- Leave a smaller discretionary portion unhedged if you can absorb the movement.

- Review staged payments separately rather than treating the whole transaction as one block.

- Avoid hedging vague future plans such as a possible renovation budget that hasn't been committed.

What changes outside Spain

In France or Portugal, the mechanics are similar because the euro exposure behaves much the same from a UK investor's perspective.

In a dollar-linked market such as Dubai, the hedge may be built around sterling versus a dollar-linked currency dynamic rather than sterling versus euro. In more volatile emerging markets, the purchase hedge often needs more caution because legal completion dates can drift, and mismatched timing can create a new problem even when the original hedge idea was sound.

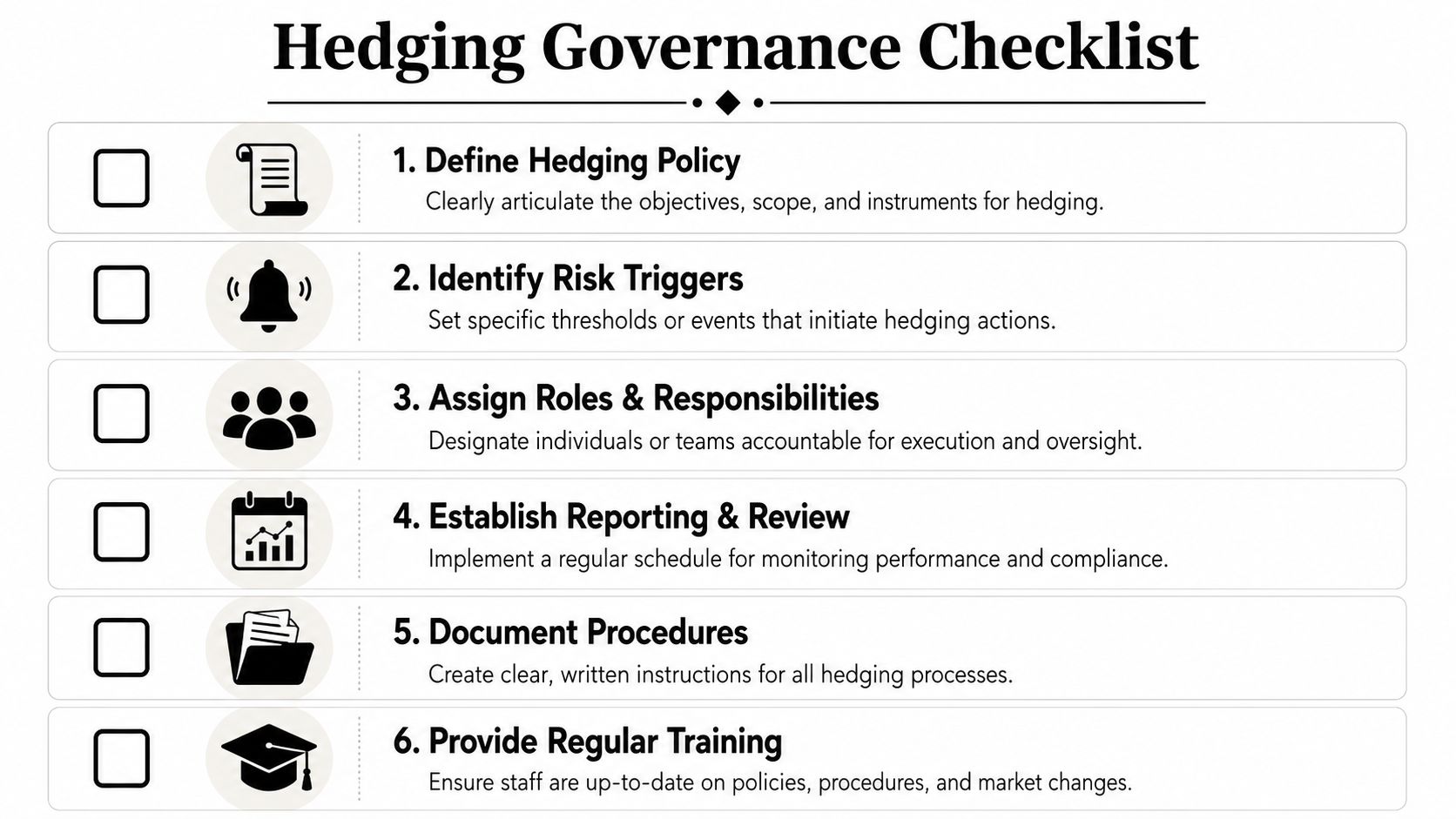

Establishing Your Hedging Governance and Timing

Investors usually lose discipline in one of two ways. They either hedge nothing and hope for the best, or they react emotionally after a sharp move and lock in a policy they haven't thought through.

Professional investors tend to do something more boring and more effective. They choose a rule, document it, and stick to it unless the underlying facts change. State Street notes that many institutions settle on static hedge ratios of 0%, 50%, or 100% because continuous optimisation is operationally difficult. The same analysis also points to selective hedging behaviour, including funds hedging only 17% of dollar investments and 27% of euro investments, while bond funds hedge almost all of their dollar exposure but only 45% of euro exposure (State Street research on hedge ratios).

A simple governance checklist

Use a written policy, even if you own only one overseas property.

- Define the objective: Decide whether you want budget certainty, income stability, capital protection, or a mix of all three.

- Separate transaction risk from portfolio risk: A completion payment is different from long-term exposure on a hold strategy.

- Set a hedge ratio by exposure type: You might hedge purchase obligations more heavily than long-dated equity exposure.

- Choose review points: Reviews can be event-driven, such as exchange of contracts, financing approval, or a decision to remit rent.

- Assign responsibility: One person should own the decision. If it's a family office or partnership, ambiguity usually causes delay.

- Keep records: Document notional amount, tenor, provider, rationale, and what would justify a change.

Timing matters more than prediction

The most effective timing discipline comes from the cash-flow calendar, not from a market view. Hedge when the liability becomes real enough to threaten the investment if FX moves against you.

For a property purchase, that might be the point at which you exchange contracts or commit a non-refundable deposit. For rental income, it might be when enough local cash has accumulated to justify a scheduled remittance. For debt service, it may be tied to the repayment calendar.

Investors who try to optimise every hedge usually end up speculating. Investors who tie hedges to real obligations usually get the outcome they actually wanted, which is control.

Match the hedge to the risk

A low-volatility income stream often deserves more protection than a high-volatility growth asset. That's consistent with the institutional pattern in the State Street research. If the currency swing can overwhelm the expected return from the asset itself, hedge more aggressively.

That principle is especially important in lower-yielding developed markets and in debt-funded deals. In those cases, an FX move can erase a large part of the expected annual return. In higher-growth or operationally messier markets, investors often accept more currency risk because the asset thesis itself already carries wider variability.

Understanding the Costs Fees and Tax Implications

Hedging only works if you understand what you're paying for. The visible cost is usually the provider's spread or explicit fee. The less visible cost sits in the forward rate itself, because the price reflects the interest-rate differential between the two currencies.

The three cost buckets to check

- Provider spread: Banks and specialist brokers quote differently. Compare the all-in exchange rate, not just the headline sales pitch.

- Transaction charges: Some providers use explicit dealing fees, transfer charges, or minimum ticket costs.

- Carry and roll cost: If you extend or roll a hedge, the pricing impact can matter as much as the initial booking.

If you're trying to reduce friction around routine conversions, this practical guide to currency fee avoidance for global trade is helpful because many of the same payment and spread issues apply to property cash flows as well.

Cost control starts with precision

McKinsey's guidance is practical here. The most effective hedging matches the instrument to the underlying exposure in amount, direction, and timing, and it warns against over-hedging long-term exposure with short-term instruments because that can remove upside and add unnecessary cost and complexity (McKinsey on managing currency risk).

That point matters in property because dates slip. Completions move. Renovation budgets change. Sale decisions get delayed. Every mismatch increases the odds that you pay to amend, roll, or unwind something that was supposed to reduce risk.

Tax needs specialist review

For UK investors, the tax treatment of FX gains and losses linked to an overseas property transaction can interact with the property's broader tax position. The practical issue isn't to assume the hedge sits in a separate box. It often needs to be considered alongside acquisition cost, disposal proceeds, financing, and reporting.

Use a qualified adviser and ask specific questions tied to your structure, residency, and ownership vehicle. Before that conversation, it helps to understand the broader framework around capital gains tax on foreign property so you can ask better questions and keep proper records from the start.

Your Key Takeaways on Currency Hedging

Currency hedging in property is about certainty, not cleverness. The best investors don't try to win a forecasting contest against the FX market. They identify where currency can damage returns and decide which exposures are worth neutralising.

Start with the five pressure points. Purchase funds, financing, rent, operating costs, and exit proceeds. Then choose the tool that matches the exposure. For a defined future payment, a forward contract is usually the cleanest answer. For ongoing operations, local currency matching and cash management often do more work than a complex hedge.

Keep the policy simple. Set a hedge ratio, tie decisions to real cash-flow events, and review when facts change. That's how to hedge currency risk in a way that supports an overseas property strategy instead of distracting from it.

If you're comparing markets, tax regimes, rental prospects, and buying rules across countries, World Property Investor offers practical guides that help you evaluate overseas property opportunities with a clearer view of risk, returns, and on-the-ground fundamentals.