You've probably had this moment already. You find a deal in Manchester, Miami, Lisbon, or Dubai that looks workable on yield, tax, and long-term demand, then the financing question stops everything. Not the headline rate. Not even the deposit. The primary constraint is whether a lender thinks your existing obligations leave enough room for one more property.

That's where debt to income, usually shortened to DTI, becomes decisive.

If you want to know how to calculate debt to income properly, the maths is simple. The difficult part is knowing what belongs in the calculation, what lenders adjust, and how cross-border income changes the answer. An investor with strong assets can still present badly on paper if recurring debts are counted aggressively or variable income is assessed conservatively.

For international buyers, DTI is one of the few metrics that translates across markets. Lenders in different countries may use different underwriting systems, different affordability models, and different evidence standards, but they all want to answer the same question. Can this borrower carry the debt without strain?

Why Your Debt to Income Ratio is a Global Investor's Passport

A lender in one market might focus heavily on salary evidence. Another may lean more on rental coverage, tax returns, or stress testing. But they all need a quick way to compare your obligations with your income. That's why DTI matters so much. It gives lenders a standard lens through which to assess borrowers with very different profiles.

For investors, that makes DTI more than a mortgage metric. It's a portability metric. If you know your real ratio before you apply, you can assess whether a purchase is financeable, whether a refinance will hurt your next acquisition, and whether your current borrowing structure limits expansion into another jurisdiction.

The formula is universal, the interpretation is local

The core idea is straightforward. Lenders compare your regular monthly debt commitments with your gross monthly income. The principle is familiar whether you're buying in the UK or the US, but the treatment of income and debts is often local.

A UK lender may place your DTI inside a wider affordability model with mortgage stress testing. A US lender may discuss front-end and back-end ratios more explicitly. In some emerging markets, the analysis can be less standardised and more relationship-driven, but the same borrowing logic still sits underneath it.

A strong investor doesn't just ask, “Can I afford this property?” The better question is, “How will a lender classify my income and debt when they underwrite it?”

That distinction matters if you hold income in multiple countries, own property through different entities, or rely on self-employed earnings. On paper, your finances may look strong. In underwriting, they may be treated very differently.

Why investors should calculate DTI before shopping for finance

Most borrowers leave DTI until they speak to a broker or lender. That's late. By then, you're reacting to a credit decision instead of shaping one.

A better approach is to calculate your DTI before choosing the asset and before deciding the ownership structure. This is particularly important if your wider strategy includes relocation, residency, or a second-home purchase linked to mobility planning. Investors looking at those routes often need to think about finance and legal status together, not separately. This is especially relevant if you're exploring investor visa routes tied to property and capital planning.

What DTI tells you beyond loan approval

Used properly, DTI helps with three practical decisions:

- Portfolio pacing: It shows whether you should buy now or wait until an existing loan rolls off.

- Market selection: It helps you compare where your income profile will be understood best.

- Financing structure: It highlights when a lower-gearing purchase may create more future capacity than a maximised one.

Investors who master DTI speak the same language as lenders. That speeds up conversations, reduces surprises, and improves your negotiating position.

Front-End vs Back-End DTI The Two Ratios Lenders Scrutinise

Some borrowers talk about DTI as if there's only one number. In practice, lenders often look at two different ratios, and they don't tell you the same thing.

The first is the front-end ratio. The second is the back-end ratio. If you're financing an investment property, you need to understand both, but the back-end number usually carries more weight.

Front-end DTI looks only at housing costs

Front-end DTI isolates the property payment itself against your income. In mortgage discussions, that usually means the housing-related monthly commitment attached to the purchase being assessed.

This ratio can be useful because it answers a narrow question. Is the property payment, by itself, proportionate to income?

That sounds helpful, and it is, but only up to a point. A borrower can look perfectly sensible on a housing-only ratio and still fail overall affordability because other obligations are too high.

Back-end DTI captures the whole debt picture

Back-end DTI is broader. It includes housing costs plus your other recurring monthly debt obligations. That's why lenders usually rely on it more heavily for final approval. It gives a fuller picture of whether your monthly cash commitments are already stretched.

Think of it this way:

- Front-end DTI: Can you carry this property payment?

- Back-end DTI: Can you carry this property payment and everything else you already owe?

For investors, the second question is almost always the one that decides the outcome.

Practical rule: If your front-end ratio looks comfortable but your back-end ratio is tight, the lender will focus on the tighter number.

That's particularly relevant for applicants with car finance, personal loans, revolving credit balances, student loan deductions, or multiple mortgages. The property might be affordable in isolation. Your balance sheet may still say no.

Why sophisticated investors still get caught out

Experienced buyers often underestimate DTI because they think in terms of assets, equity, and net worth. Lenders don't underwrite net worth in the same way they underwrite recurring obligations. Monthly servicing capacity matters more than broad balance-sheet strength in the first stage of approval.

This comes up often with second homes and mixed-use portfolios. An investor may own substantial property but still carry too many monthly commitments for a new mainstream mortgage. If you're planning a holiday home, pied-à-terre, or personal-use acquisition, the borrowing framework can change again, especially around occupancy assumptions and existing commitments. It helps to understand the common second home mortgage requirements lenders review.

The ratio that usually matters most

If you remember only one point from this section, keep this one. Back-end DTI is the operational number.

Front-end DTI helps frame the housing payment. Back-end DTI tells the lender whether your full monthly debt load remains manageable. For property investors, especially those buying across borders, that's the ratio that usually shapes borrowing power.

The Core Calculation A Step-by-Step Breakdown

A cross-border investor can have strong assets, healthy equity, and reliable rent coming in, then still hit a lending problem because the monthly income figure and the monthly debt figure were assembled the wrong way. The formula itself is simple. The judgement sits in what goes into each side.

Start with the lender version of your numbers, not your own management accounts or household budget. For a standard DTI calculation, you divide total monthly debt obligations by gross monthly income, then multiply by 100. The Consumer Financial Protection Bureau uses the same core method in its consumer debt-to-income guidance.

Build the debt side first

This is usually where experienced investors make the bigger error, especially if they hold property in more than one country.

DTI is based on committed monthly debt payments. It is not a measure of total living costs, portfolio quality, or net worth. Include obligations that a lender can see and verify. Leave out ordinary spending that is not a contractual debt payment.

Debt and Income Checklist for DTI Calculation

| Category | Include in Calculation | Notes for Investors |

|---|---|---|

| Existing mortgage payments | Yes | Include monthly mortgage commitments on properties you already own |

| Proposed new mortgage payment | Yes | Often missed in self-assessments. Many lenders underwrite with the new payment included |

| Minimum credit card payments | Yes | Use the required minimum payment |

| Personal loans | Yes | Count the contractual monthly repayment |

| Car finance | Yes | Include all active vehicle finance commitments |

| Student loan deductions | Yes | Include where the lender treats them as recurring obligations |

| Other committed financial obligations | Yes | Convert each recurring debt to a monthly figure |

| Groceries and utilities | No for core DTI | These affect affordability reviews, but they are not core DTI debt items |

| Gross salary or drawings before tax | Yes | Use pre-tax income, not take-home pay |

| Variable income | Sometimes, with caution | Lenders may average it or apply a haircut |

| Rental income | Sometimes, with adjustment | Usually assessed under lender-specific rules, not your full forecast |

One practical warning. International applicants often miss debts reported in one jurisdiction but not front of mind in another, such as US credit card minimums, UK buy-to-let mortgages, director loan repayments, or secured borrowing against a foreign property. If it creates a recurring payment, assume the lender will want it disclosed.

Use gross income. Then test whether the lender will recognise all of it.

Applicants often plug in net income because it feels closer to real cash flow. That is useful for your own budgeting. It does not usually match underwriting.

Lenders generally start from gross monthly income before tax and deductions. For employed applicants, that part is straightforward. For self-employed investors, company owners, and applicants with mixed income streams, it gets more technical. A lender may use salary plus dividends, retained profit, averaged earnings over multiple years, or a reduced figure if recent income is volatile.

That difference matters more in international cases. A US lender may focus on tax returns and add-backs. A UK lender may focus more heavily on salary, dividends, SA302s, accounts, and affordability stress testing. Two lenders can look at the same borrower and produce different usable income figures.

Handle self-employed and foreign income with discipline

For entrepreneurs and portfolio investors, the cleanest approach is to rebuild income into lender-ready categories.

- Employment salary: Usually accepted if evidenced through payslips or employment letters.

- Self-employed income: Often based on tax returns, filed accounts, or an average across years rather than recent receipts.

- Bonus, commission, or overtime: Commonly discounted unless there is a stable track record.

- Dividend or director income: Treatment varies by lender and by how the business is structured.

- Foreign currency income: Often accepted more cautiously, with extra documentation and possible currency risk adjustments.

I advise clients to use the lower defendable figure first, then test upside only after that base case works. That prevents a common mistake. Borrowing plans built on the best recent quarter often fail once underwriting moves from headline income to documentable income.

If you are preparing your file, it helps to review the broader steps to qualify for a mortgage alongside the DTI calculation, because timing, documentation, and liability treatment often change the result.

Use the income a credit team can verify and sustain, not the income your portfolio produced in its strongest recent month.

Apply the formula

Once the inputs are clean, the calculation is straightforward:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) x 100

For example, if your total monthly debt payments are £1,000 and your gross monthly income is £3,000, your DTI is 33.3%.

The arithmetic is easy. The underwriting judgement is not. A self-employed investor with foreign income, two existing rentals, and a new purchase in another market may calculate 33.3% personally and still be assessed higher by a lender if part of that income is reduced or excluded.

Where investor calculations go wrong

The recurring error is treating DTI as a personal budgeting exercise instead of a credit underwriting exercise. Investors often use actual overpayments on credit cards instead of minimums, include projected short-term rental upside before a lender will recognise it, or leave out the proposed mortgage because the deal has not completed yet.

The better approach is to run two versions. First, calculate your raw DTI using the standard formula. Second, calculate a lender-style DTI using conservative income treatment and the full proposed housing payment. That second number is the one that tends to determine whether an application survives first review.

Serious buyers also compare financing capacity with property-level returns before committing capital. A purchase can look attractive on yield and still weaken borrowing headroom if the monthly debt load rises faster than recognised income. That is why financing analysis should sit beside rental yield calculations for property decisions.

How Lenders Treat Rental Income and Investment Properties

Investors often assume rental income will solve a tight DTI. Sometimes it does. Sometimes it barely helps. The difference comes down to how the lender treats that income, not how you model the property in your spreadsheet.

That gap matters in every market. Your investment case may rely on gross rent, seasonal upside, or portfolio diversification. A lender is usually asking a narrower question. How much of this income is stable enough to include in affordability?

Existing rent and projected rent are not treated the same way

For properties you already own, lenders often want evidence. That may include tenancy agreements, bank statements, tax returns, or accounts. For a property you haven't yet bought, they may look at projected rent more cautiously.

Experienced investors need to separate investment underwriting from mortgage underwriting. Your own model may use market rent assumptions, occupancy expectations, and operational improvements. A lender may apply a tighter view and only recognise part of that income, particularly if the asset is short-term let, newly converted, or overseas.

Established markets are usually more formulaic

In established markets such as the UK and US, underwriting tends to be structured and document-heavy. That doesn't always mean it's harsher, but it usually means it's less negotiable.

In some emerging markets, there can be more room for relationship-led decision making, stronger emphasis on asset value, or a more bespoke review of foreign buyers. That flexibility can help, but it can also create inconsistency. Investors should be careful not to confuse a looser initial conversation with a dependable credit standard.

A practical implication follows. If you're borrowing in a market with formal affordability tests, your own rental projections should be stress-tested before the lender does it for you.

Self-employed investors face a double layer of scrutiny

The issue becomes sharper when the borrower is also self-employed. UK lenders commonly average income over 1 to 3 years of accounts or tax returns, and they may assess bonus, commission, overtime, and variable income conservatively. The same guidance notes that this remains a confusing area for freelancers and contractors, especially given the UK's large and persistent self-employed workforce (self-employed DTI treatment).

That means a self-employed investor with rental income faces two separate judgement calls:

- How much of their earned income will be accepted?

- How much of their rental income will be counted?

Those decisions can vary between mainstream lenders, specialist lenders, and brokers packaging the case. Two investors with similar cash flow can end up with different borrowing capacity because one presents income in a format lenders can use more easily.

If your income is irregular, lender-ready presentation matters almost as much as the income itself.

Short-term rental investors need extra caution

Holiday-let and short-stay investors often rely on market seasonality, dynamic pricing, and occupancy management. That can produce strong gross revenue, but lenders may still prefer a more conservative baseline when assessing affordability.

If you're modelling a short-term let, it helps to understand the commercial side separately from the mortgage side. A practical reference point is to look at market pricing patterns, such as these Florida vacation rental rates and pricing considerations, then ask whether your lender will recognise that income on the same basis. Often, they won't.

That's why loan selection matters. Investors comparing products for buy-to-let, second homes, and portfolio expansion should examine how different investment property loan structures work in practice, especially where rental income treatment differs by lender and asset type.

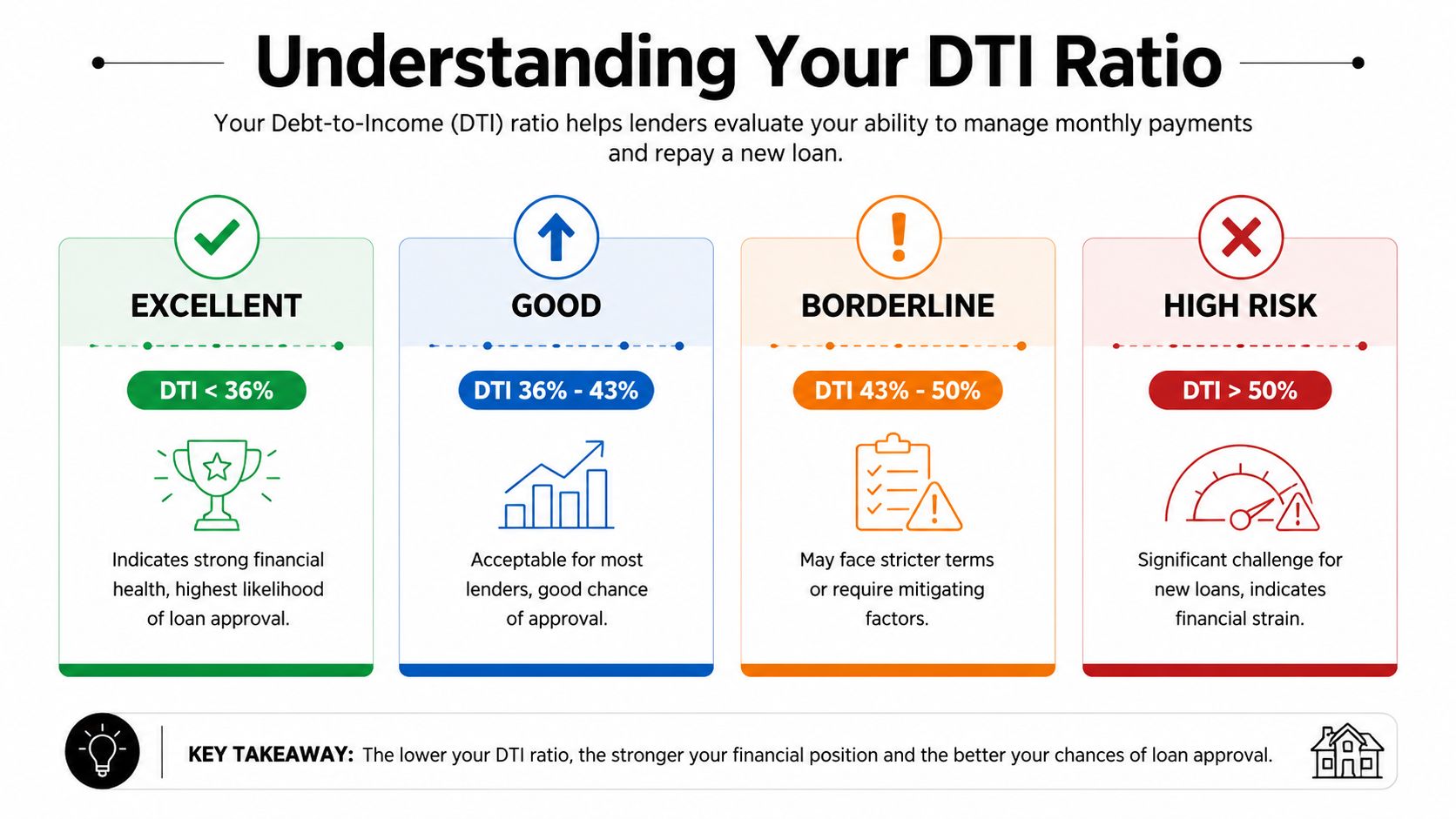

Interpreting Your DTI What Is a Good Ratio?

Once you've calculated the ratio, the next question is simple. Is it good enough?

The answer depends on market, lender, and loan type, but there are still useful benchmarks. In the UK mortgage context, lenders commonly look for debt burdens around the mid-30% range, and widely used lending guidance treats a DTI of about 36% or less as comfortably manageable, while around 50% or more is generally considered high risk (UK DTI benchmark guidance).

What those bands mean in practice

The same benchmark gives a clear working example. A borrower earning £4,000 gross per month would typically want total monthly debt payments below about £1,440 to stay near the 36% threshold, and below about £2,000 at the 50% level.

That tells you two things immediately. First, small changes in monthly debt matter more than many investors expect. Second, DTI can tighten quickly when you already hold multiple loans, even if your properties are performing well.

A practical way to read your own result

Use your DTI as a lending signal, not as a moral judgement about debt.

- Below the lower benchmark range: You're usually in a stronger position for mainstream underwriting.

- Around the middle band: The case may still work, but lender choice and evidence quality become more important.

- Near the high-risk end: Expect friction. The deal may still be possible, but terms, product options, and approval odds usually get worse.

This is why established and emerging markets can feel so different. In more standardised lending systems, DTI thresholds often act as early filters. In less standardised systems, you may get further into the process before affordability concerns surface.

A “good” DTI isn't just the ratio that gets approved. It's the ratio that still leaves you room for the next opportunity.

Why investors should think in capacity, not just eligibility

A lender might approve a borrower near the upper end of acceptable debt levels. That doesn't make it wise for a portfolio investor. A ratio that technically passes can still reduce resilience if rates move, vacancy rises, or another acquisition appears sooner than expected.

That's why I usually treat DTI in two ways. One number tells you whether you're likely to qualify. The second question is whether the post-closing ratio leaves enough flexibility to keep investing. Those are not always the same answer.

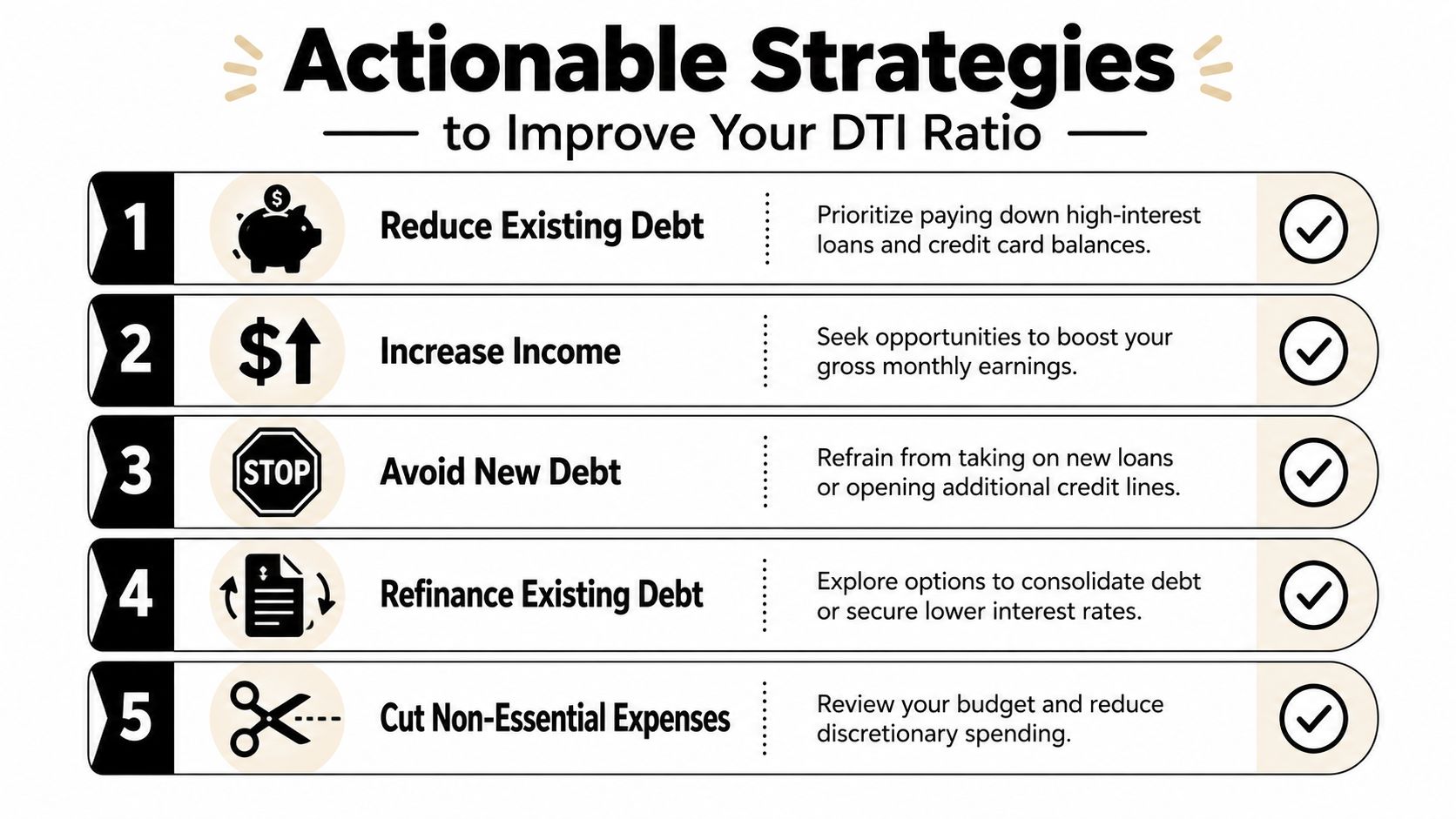

Actionable Strategies to Improve Your DTI Ratio

A borrower can look strong on paper, own profitable rentals in two countries, and still fail affordability because the wrong monthly commitments sit in the file. I see this often with international investors. The issue is not total wealth. It is which debts the lender counts, which income they discount, and how the case is documented.

If your ratio is too high, improve the inputs lenders use. Start with monthly obligations, then move to income presentation, then review deal structure. That order usually produces the fastest underwriting improvement.

Cut the monthly payments that hurt affordability most

DTI responds to monthly outgoings, not headline balances. A modest loan with a heavy monthly payment can damage affordability more than a larger loan amortised over a longer term.

Prioritise the debts that release the most monthly capacity:

- Reduce revolving credit first: Minimum card payments often consume more affordability than investors expect, especially in US applications where underwriters are strict on reported obligations. Practical guidance from Morgan Lawyers on credit card debt can help if card balances are part of the problem.

- Clear short-term instalment debt where possible: Car finance, personal loans, and buy-now-pay-later commitments can materially weaken a mortgage case.

- Do not add fresh liabilities before application: A new vehicle lease, unsecured loan, or financed purchase can change the underwriting result, even if your income is otherwise strong.

For portfolio investors, the trade-off matters. Using cash to clear debt may improve DTI faster than holding that cash for a deposit. But it can also reduce liquidity, which some lenders and experienced investors both value. The right move depends on whether the immediate constraint is affordability, deposit size, or reserve requirements.

Make income easier for a lender to accept

High earners are declined every year because the income is real but difficult to evidence. This is common with self-employed applicants, company directors paid through salary and dividends, contractors, and investors earning across jurisdictions.

Lenders in the UK often want a stable pattern in tax returns, company accounts, or SA302s. US lenders may average variable income over a set period and apply their own adjustments to rental or business income. Cross-border income adds another layer. Foreign currency earnings may be discounted, and overseas rental income may only count if it is clearly documented and already visible in tax filings or audited accounts.

Three practical steps help:

- Apply after the stronger period is documented. If profits have improved recently, waiting for filed accounts or completed tax returns can produce a better result than applying too early.

- Separate personal and business cash flow cleanly. Mixed accounts create avoidable questions and often lead underwriters to use the most conservative reading.

- Present rental income on a lender basis, not an investor basis. Some lenders use gross rent, some use a percentage, and some want costs, vacancies, and mortgage payments evidenced before they give credit.

That last point is where international investors often lose ground. The property may perform well, but the lender may still haircut the income or ignore part of it if the documents do not fit local underwriting standards. This guide to buying property abroad with a mortgage gives a useful overview of how lenders assess borrowers whose income, assets, and liabilities sit in different countries.

Before the final push, it's worth hearing a concise walk-through of how borrowers can improve affordability in practice:

Adjust the case structure if the numbers are close

Sometimes the fastest improvement comes from changing the application setup rather than rushing to repay more debt.

For example, a self-employed applicant may get a better outcome after filing the latest year of accounts. A landlord with overseas rent may need to apply with a lender that has a clear policy for foreign income. In joint applications, changing which borrower is included can improve affordability if one applicant carries high personal debt or unstable income.

I regularly advise clients to compare three versions of the same deal before submitting anything: the application now, the application after one debt is cleared, and the application after the next reporting period. That exercise often shows whether speed or preparation will produce the better lending result.

Keep enough borrowing capacity to absorb rate moves, vacancy, and the next acquisition without forcing weak decisions.

If you're comparing markets, financing routes, and rental fundamentals across borders, World Property Investor is a strong place to continue your research. The site brings together country guides, market comparisons, and practical buying advice for investors who want to make better property decisions with clearer data.