A lot of UK buyers start in the same place. They want a base in Spain, a better climate, and a cleaner lifestyle shift than a full stop retirement in Britain. Then the practical questions arrive. Which visa fits best, can the property earn income, what happens to tax residency, and how much bureaucracy sits between the plan and the keys?

That's where most retire in spain visa advice falls short. It treats residency as a lifestyle formality and property as a separate decision. In practice, they're tightly linked. The visa you choose affects how you can use your property, how you evidence income, how you organise your entry into Spain, and how flexible your long-term portfolio becomes.

For a UK investor, the primary decision usually sits between the Non-Lucrative Visa, which suits applicants living from pensions, investments, rental income or savings, and the Golden Visa route, which may become relevant later if you want a more flexible structure with work rights. The right route depends less on aspiration and more on cash flow quality, timing, and how active you want your investment life in Spain to be.

Securing Your Future in the Spanish Sun

Spain still attracts buyers for obvious reasons. The lifestyle is easier to visualise than in most relocation markets. Coastal living, walkable towns, and access to the wider Schengen area make it more than a retirement fantasy. But if you're approaching this as an investor, the lifestyle story only matters if the structure underneath it holds up.

The first discipline is separating living costs, visa costs, and investment costs. Many buyers blend them into one rough budget and end up underestimating what needs to be liquid at each stage. Before you even compare locations, it helps to benchmark everyday expenditure against a broader Spain living cost guide for investors and expats, then ringfence funds for immigration and property separately.

Why visa planning changes the property plan

A retire in spain visa decision isn't just about permission to stay. It determines what income evidence you need, what administrative deadlines you face on arrival, and whether your property strategy should be passive from day one or structured for a later visa upgrade.

Three issues matter most:

- Income quality matters more than asset value. Spanish authorities want to see dependable, documented means.

- Timing matters. Visa approval, entry to Spain, TIE registration, viewings, legal checks, and completion can collide if you plan them in the wrong order.

- Use matters. Some buyers want a home first and yield second. Others need passive income from the asset to support renewals and long-term holding costs.

Investor lens: A good Spanish relocation plan doesn't start with the property type. It starts with the residency route, the cash flow evidence, and the tax consequences of becoming resident.

That's why the strongest retire in spain visa strategy is rarely the most glamorous one. It's the one that keeps your file clean, your deadlines realistic, and your property flexible enough to serve both lifestyle and portfolio goals.

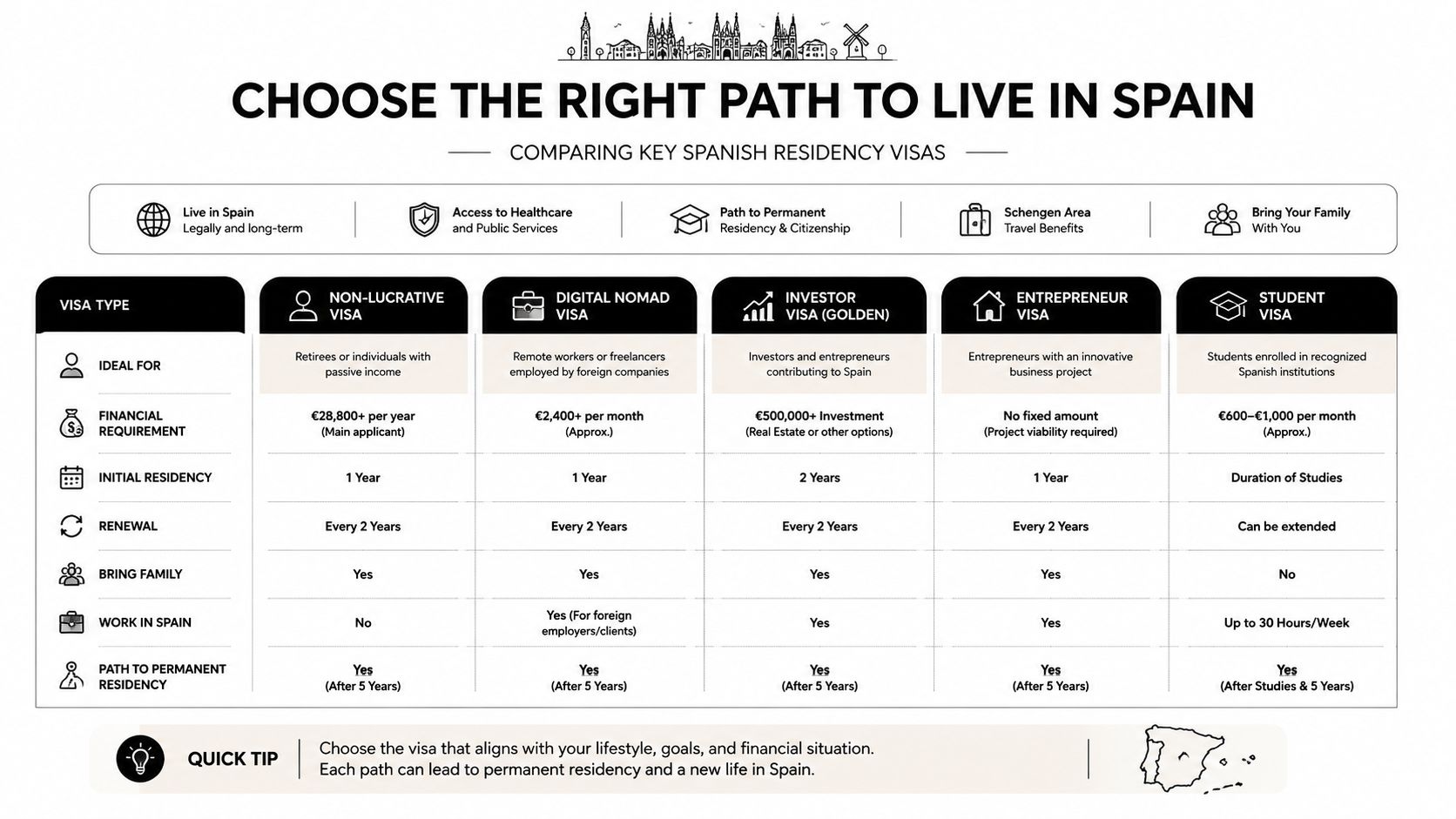

Choosing Your Spanish Residency Visa

A UK buyer who plans to spend long periods in Spain usually reaches the same fork in the road early. Keep capital liquid and prove passive income, or commit more money to Spain and build residency around the investment itself. That choice affects far more than paperwork. It shapes how quickly you can buy, whether you need the property to produce income, and how exposed you become to Spanish tax residency.

The Non-Lucrative Visa for passive-income applicants

For many UK applicants, the Non-Lucrative Visa is still the cleanest entry route. It lets you establish residence without buying first, which matters if you want time on the ground to compare regions, test rental demand, and avoid forcing a purchase around a consular deadline.

The main hurdle is documented financial capacity. The 2026 requirement is €28,800 annually for the main applicant, approximately £25,000 for a UK applicant, with an additional €7,200 per dependent, taking a couple to €36,000 per year, according to Anchorless on Spain's 2026 non-lucrative visa rules.

That usually suits applicants with pensions, dividends, rental income outside Spain, or sizeable savings held clearly in their own name. It suits investors too, but only if the income trail is easy to evidence. A healthy balance sheet helps. A messy file with irregular withdrawals, opaque company structures, or undocumented transfers does not.

From an investment standpoint, the NLV gives you room to buy selectively. You can rent first, learn the local market, and decide whether your Spanish property should be a primary residence, a seasonal asset, or part of a longer-term income strategy.

The investor route for buyers who want more flexibility

The investor route appeals to applicants who want residency tied more directly to capital deployed in Spain. In practice, it tends to suit buyers who are already comfortable committing substantial funds to a Spanish asset and who want more flexibility around how they structure life and work after arrival.

The trade-off is straightforward. You preserve less liquidity, but you may gain more freedom in how the residency position fits into a broader portfolio plan. For some UK clients, that works well where Spain is not just a retirement destination but a base for a second home, family use, and long-term capital allocation.

The route has also faced policy pressure in recent years, so applicants should assess current rules at the point of filing rather than relying on older headlines or forum advice.

Side-by-side decision framework

| Feature | Non-Lucrative Visa (NLV) | Investor-led residency route |

|---|---|---|

| Main basis | Proof of passive means | Qualifying investment |

| Financial threshold | €28,800 for main applicant in 2026, plus €7,200 per dependent | Higher capital commitment tied to the relevant investment rules |

| Work position | No paid professional activity under the standard NLV framework | Greater flexibility may be available, depending on the route in force |

| Best fit | Applicants with strong pension or investment income | Buyers treating Spain as part of a larger wealth and residency strategy |

| Property timing | Buy later, once the area and asset type are clear | Buy earlier as part of the residency plan |

| Portfolio effect | Preserves liquidity for staged entry into the market | Concentrates capital in Spain sooner |

For a UK investor, the fundamental question is not which visa sounds better. It is which route fits the evidence you can present and the way you want the Spanish property to perform over the next five to ten years.

How to choose with an investor mindset

Use the NLV if your passive income is reliable, your paperwork is clean, and you want time to assess locations before purchasing. That route often works well for buyers deciding between a lifestyle-led home in Valencia or Málaga and a more yield-focused asset in a different market.

Use an investor-led route if Spain is already a confirmed allocation decision and you are comfortable tying residency to a substantial purchase. That can make sense for a buyer planning a premium asset with limited borrowing, lower vacancy risk, and long holding periods.

What usually fails is a half-formed strategy. Applicants try to use property wealth to compensate for weak income evidence, or they buy too early in the wrong area because they assume residency and acquisition should happen at the same pace. They should not.

A final practical point. Consulates and visa centres often reject files over small technical errors, including photo specifications, so many applicants create Spain visa photos online before the appointment rather than risk a rebooking.

For a wider comparison of routes used by internationally mobile buyers, review this guide to Spanish investor visa and residency options for property buyers.

The Visa Application Process Step by Step

The Spanish process is manageable if you treat it like a transaction. It becomes messy when applicants treat it like a holiday admin task. For UK applicants, the sequence matters as much as the paperwork.

Build the file before booking confidence gets expensive

The most common mistake is booking appointments too early, then scrambling to legalise or translate documents. For UK applicants, consular resolution typically takes 1 to 3 months, all supporting documents must be officially legalised and translated into Spanish, and a typical UK couple can expect total visa-related costs of £4,300 to £6,000 before relocation, according to this UK-focused Spain visa process breakdown.

That means the retire in spain visa process should be run in stages:

- Income evidence first. Gather pension letters, investment statements, recent bank statements, and tax material that clearly support your means.

- Personal documents next. Criminal records, marriage certificates where relevant, and medical certification need to be current, properly issued, and capable of legalisation.

- Translation and legalisation after that. Many first-time applicants lose time during this specific stage.

- Then the appointment. Not before.

The documents that usually cause delays

Some documents are straightforward. Others are time-sensitive and get rejected because they're outdated, incomplete, or not properly stamped.

A practical checklist looks like this:

- Financial proof: Recent bank statements and income evidence should tell one story without gaps or contradictions.

- Identity papers: Passport copies and civil status documents need to align across names, dates, and spellings.

- Criminal record documents: These must be legalised and translated correctly.

- Medical certificate: It needs to meet the Spanish consular wording and timing requirements.

- Application forms: Small omissions create disproportionate delays.

A strong file reads like an audit trail. Each document should support the next one.

Health insurance is a compliance test, not a shopping exercise

Applicants often underestimate private health insurance because they compare it with ordinary travel or expat cover. That's the wrong benchmark. The required policy must provide 100% coverage of medical, hospital, and out-of-hospital expenses with zero deductibles, zero co-payments, no waiting periods, and no coverage limits for the full 12-month period, as explained by My Spain Visa's guidance for retirement applicants.

If the policy doesn't meet that standard, the rest of the file can still be weakened. For investors, that matters because delays ripple into travel dates, rental planning, and acquisition schedules.

Budget realistically, not optimistically

A typical UK budget should account for more than the consular fee. Real spend usually includes:

- Preparation costs: Document gathering, legalisation, translation, and certificates.

- Appointment costs: Consular charges and related admin.

- Insurance spend: Mandatory private cover paid on terms acceptable to the visa rules.

- Contingency: Replacement documents, new certificates, and extra translation work if timing slips.

Another overlooked point is document freshness. Some supporting records need to be recent, and if a file drifts, you may end up paying twice to refresh documents that were correct but no longer current by submission day.

Property Investment and Your Spanish Visa

A common UK investor scenario looks like this. You want a base in Spain, some rental income to offset holding costs, and residency that does not create an avoidable tax problem or force a rushed purchase. Your visa choice affects all three.

The non-lucrative visa can sit alongside property ownership and passive income. The practical boundary is activity. Holding a Spanish property, collecting rent through the right structure, and using local agents for management is one thing. Running an active short-let operation yourself while resident under an NLV is where clients start creating unnecessary risk.

What the visa means for an investment plan

For a UK buyer, the property decision should be tested against the residency route from day one. If the plan is an NLV, the asset needs to work as a personal base first and an investment second. That usually points to locations with stable resale demand, solid long-let fundamentals, and lower dependence on peak-season tourism.

A property can still serve several purposes at once:

- Residence base: A home you can use while establishing yourself in Spain.

- Income asset: Passive rental income that helps cover service charges, IBI, insurance, and maintenance.

- Portfolio foothold: A lower-risk entry point before deciding whether to commit more capital to Spain later.

That last point matters. Buying too early, or buying the wrong asset class, is expensive to fix.

Where investors misread the risk

The problem is rarely ownership. It is strategy.

Some buyers assume any attractive coastal unit will produce reliable holiday-let income. That assumption has weakened in parts of Spain because local licensing rules, community restrictions, and municipal pressure on short-term lets can change faster than an overseas owner can respond. An asset that only works as a tourist rental is a fragile asset.

I generally advise clients to underwrite the purchase on conservative terms. Ask whether the property still works if it is used as a long-let, a part-year residence, or is left without peak-season occupancy for a period. If the numbers only make sense under an aggressive Airbnb model, the risk sits in the property, not the visa.

The best NLV-friendly purchase is a property that remains financially sensible even if short-term rental income disappoints.

Timing matters more than many buyers expect

Residency deadlines affect acquisition timing. As outlined by Wise's guide to retiring in Spain, visa holders have a limited window to enter Spain after approval and then a short period after arrival to complete the TIE process. That compresses your schedule.

For investors, the implication is straightforward. Do the research before approval, but avoid forcing completion into the same narrow window as travel, local registration, and residency appointments.

| Stage | Better approach for investors |

|---|---|

| Before approval | Research markets, appoint an independent lawyer, compare ownership costs, and shortlist target areas. |

| Immediately after approval | Prioritise travel dates, arrival planning, and the first mandatory residency appointments. |

| Early post-arrival | View properties selectively, but keep paperwork and local admin ahead of deal momentum. |

| After local admin is under control | Move on price negotiation, legal checks, mortgage approval, and completion. |

Finance also needs to be planned in parallel. If part of your capital must remain visible for visa compliance, borrowing may preserve flexibility, but only if the loan terms still support the investment case. A realistic review of mortgage rates in Spain for foreign buyers helps you judge whether financing improves the deal or merely adds cost and complexity.

The stronger approach is disciplined. Use the first phase of residency to confirm area quality, building condition, service-charge exposure, rental demand, and your likely tax position before committing more capital than necessary.

Post-Arrival Essentials for Investors in Spain

The move isn't complete when you land. For investors, the first weeks in Spain are administrative, and they affect both your legal status and your ability to run property ownership cleanly.

Handle residency admin before lifestyle admin

A lot of buyers make the same mistake after arrival. They prioritise furniture, bank meetings, and area exploration ahead of formal residency tasks. That order feels natural but it's risky. Your TIE and related local administration should come before the softer parts of settling in.

The right mindset is simple. Treat arrival week like the opening week after completion on an investment asset. Deadlines matter. Documents matter. Local appointments matter.

Tax residency is where many plans become expensive

For UK investors, the most serious post-arrival issue is often tax, not immigration. The verified warning is important. Many UK expats must file Spain's Form 720 to declare UK assets, including property, over €50,000, and failure to do so can result in fines starting at €10,000, according to Lumon's article on Spain retirement visa planning.

That matters if you still own UK rentals, hold overseas investment accounts, or keep substantial assets outside Spain. A lot of retirees assume that if an asset stays in Britain, it stays outside Spanish reporting concerns. That assumption causes trouble.

A practical post-arrival checklist

Use the first phase in Spain to get these priorities in order:

- TIE appointment: Don't treat this as flexible admin. It's central to your legal footing.

- Tax advice: Get Spain-specific advice early if you hold UK property, pension assets, or offshore accounts.

- Asset reporting review: Check whether Form 720 applies to your situation before the filing issue becomes urgent.

- Property paperwork: Make sure ownership, insurance, utilities, and local contact details are properly aligned.

- Healthcare continuity: Plan beyond the first policy year so there isn't a coverage gap later.

If you own property in more than one country, tax residency usually becomes more complex faster than buyers expect.

For broader relocation context, this guide on living in Spain as an expat and investor is a useful companion once the visa is in place and the move becomes operational.

Common Pitfalls and Expert Tips for UK Applicants

The most expensive mistakes usually come from false confidence. Buyers assume that because Spain is a familiar market, the move will be intuitive. It isn't. The visa route, tax exposure, and property timing all need to line up.

The mistakes that cost the most

Some problems repeat constantly:

- Under-budgeting the process: Buyers plan for property costs and ignore visa administration, insurance, and document work until late.

- Misreading the no-work rule: Passive income is one thing. Active local economic activity is another.

- Rushing the purchase: A property bought too early can create pressure before residency logistics are stable.

- Ignoring pension and tax structure: UK pension income may support the visa, but the tax treatment after relocation needs proper review.

- Choosing only headline markets: Established areas feel safer, but they can also be more crowded, more regulated, and harder to operate efficiently.

What stronger applicants do differently

The investors who handle the retire in spain visa process well usually do three things. They keep documents orderly, they choose a property strategy that still works under stricter conditions, and they take tax advice before they become resident rather than after.

I'd also challenge one common assumption. Bigger names aren't always better markets for a retiree-investor. Barcelona, Valencia and parts of Andalusia attract obvious attention, but established markets often come with more competition and less room for error. Emerging inland and secondary markets can offer a calmer operating environment, better local fundamentals for long-term letting, and fewer expectations built on peak tourism.

If you're still comparing whether the move is right at all, it helps to step back and review the wider process of leaving the UK for a new life abroad. Spain works best when it fits the whole financial picture, not just the climate preference.

World Property Investor helps international buyers compare markets, understand yields, assess visa-linked property strategies, and make better cross-border decisions. If you're weighing Spain against other residency or buy-to-let destinations, explore World Property Investor for practical market guides, investor research, and country-by-country property analysis.