A lot of investors first meet dual citizenship at the wrong moment. They've already found the apartment in Lisbon, opened the file on a Dubai purchase, or started planning a family move while keeping a UK rental portfolio. Then the core questions arrive. Can I own in the same way as a local? Which passport do I travel on? Does a second nationality change my tax position, my inheritance planning, or my ability to finance property abroad?

That's why what dual citizenship is matters far beyond immigration law. For property investors, it sits at the intersection of mobility, market access, compliance, and family planning. It can make cross-border life easier, but it can also create obligations in two legal systems at once.

Most online guides stop at “you can hold two passports”. That's not enough. A serious investor needs to know what works in practice, where people get caught out, and which assumptions can become expensive.

Dual Citizenship and the Modern Property Investor

A typical scenario looks like this. A British investor wants a base in southern Europe, keeps buy-to-lets in England, and spends part of the year overseas. They start by asking about visas or residency. Very quickly, the discussion turns into something else entirely. Would a second citizenship help, or would it complicate tax and reporting?

For some investors, dual nationality is inherited and not planned at all. A parent was born elsewhere. A child is born abroad. Someone naturalises after years of residence and keeps their original nationality because both countries permit it. For others, it becomes part of a broader strategy around mobility, succession, and family options.

Global migration patterns help explain why this is now mainstream rather than niche. A comparative study noted that by the late 1990s 89 countries permitted multiple citizenship, and 16 of the top 20 immigrant-sending countries allowed some form of it, accounting for 83.9% of that flow from the top 20 senders (comparative study on dual citizenship and migration patterns). For investors, that matters because the people buying, relocating, inheriting and structuring across borders increasingly do so with more than one nationality in play.

The key point is practical. Dual citizenship isn't just about identity or convenience. It can affect:

- Market access: Some countries treat citizens and non-citizens differently when buying, inheriting, or financing property.

- Mobility planning: Travel flexibility can support portfolio management across several jurisdictions.

- Family structuring: Spouses and children may end up with different rights to live, work, study, or inherit in different countries.

- Risk management: Political change in one country is less disruptive when a family has lawful status elsewhere.

Practical rule: Investors usually overestimate the benefit of the second passport itself and underestimate the compliance that comes with it.

If you're exploring routes to a second nationality, this guide on how to get dual citizenship is a useful starting point. The important thing is to treat nationality as one layer of your international planning, not the whole plan.

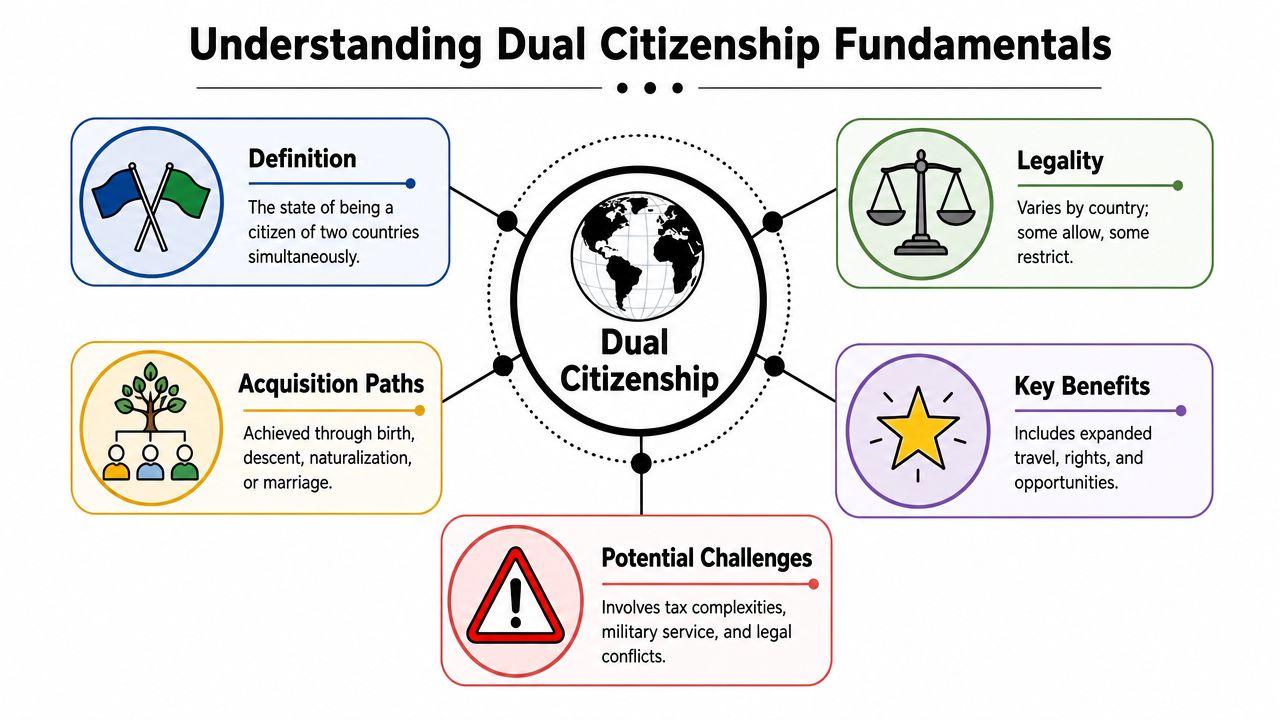

Understanding Dual Citizenship Fundamentals

Dual citizenship, also called dual nationality, means a person is legally recognised as a citizen of two countries at the same time. In UK practice, that status is possible because British citizenship can exist alongside another nationality if the other country's law also allows it.

That sounds simple. In practice, it happens because two legal systems reach the same person at once.

The main ways people become dual nationals

Most investors assume there is a formal application called “dual citizenship”. Usually, there isn't. Dual nationality often arises as the result of acquiring one citizenship while already holding another. UK-aligned guidance notes that it can happen when a child is born in one country to a parent from another, or when someone naturalises in a new country that permits retention of the original nationality. It also notes that the UK does not issue a separate dual-citizenship certificate (guidance on how dual nationality arises).

The three pathways investors most often need to understand are these:

Birth in a country

Some countries grant citizenship because you were born there. If another country also recognises you through a parent, you may hold both from day one.Descent through a parent

A child born outside the UK to a British parent may have a claim to British citizenship, while also being a citizen of the country of birth.Naturalisation after residence

An adult moves, settles, meets residence and legal requirements, then naturalises without losing the first nationality because both states allow it.

What dual citizenship is not

It isn't a visa.

It isn't permanent residence.

It isn't a tax status.

That distinction matters for property investors because many rights that affect real estate, such as the right to live indefinitely in a country or avoid foreign-buyer restrictions, may depend on citizenship or residence, but tax often turns on different tests.

A practical example helps. Someone may be a British citizen and later naturalise elsewhere. That doesn't create a hybrid legal identity. It creates two separate citizenships running side by side, each with its own rules.

Dual nationality is a legal overlap, not a legal merger.

For investors researching structured routes, including investor-led options in some jurisdictions, it helps to understand the broader scope of citizenship by investment. Just remember that the route is only one part of the analysis. The harder work is understanding what the status truly changes once you hold it.

Why the fundamentals matter for investors

The most common mistake is to jump straight to benefits. Start with legal character instead.

- Ownership rights may improve, especially where foreign ownership is restricted.

- Residence options may widen, which can affect how often you can use or manage a property.

- Family rights may differ, particularly for spouses and children.

- Compliance may become heavier, because two states may both expect documents, declarations, and legal obedience.

This is what dual citizenship means. It's not just access. It's access with obligations.

Practical Implications Travel Passports and Protection

For a globally mobile investor, dual citizenship becomes most visible at the border. You book flights, renew passports, pass through immigration, and assume the second passport is mainly a convenience tool. Sometimes it is. Sometimes it's also the start of a legal problem if you use the wrong document in the wrong place.

Passport use is not optional

The practical effect of dual nationality is that a person owes legal duties to both states simultaneously. Official guidance explains that dual nationals must follow the laws of each country, and one country may require use of its own passport for entry and exit. That can affect border processing, legal obligations and access to consular support (official guidance on dual nationality duties and passport use).

For a British dual national, the operational rule is straightforward in practice. If you're entering or leaving the UK, use the British passport. If the other country requires its own passport for arrival or departure, use that there.

The upside for investors

The obvious benefit is mobility. If you inspect assets, open bank accounts, meet brokers, or rotate between countries for part of the year, multiple passports can reduce friction. They can also help when one passport gives easier access to a market where you hold or plan to hold property.

A second practical advantage is continuity. If one country changes entry rules or experiences disruption, another nationality can preserve lawful access elsewhere. For investors with tenants, contractors, or family in different places, that flexibility matters.

Short-term examples include:

- Portfolio visits: You can travel to review refurbishments, complete notarisation, or deal with management issues with fewer immigration hurdles.

- Banking and administration: Some institutions are more comfortable onboarding citizens than foreign clients.

- Family logistics: Schooling, healthcare access, and spousal rights often become easier when status is clear.

For readers looking at mobility-focused passports in the Caribbean space, this overview of the Saint Lucia passport is one example of how investors assess practical travel value alongside broader planning.

Where people get caught out

The second passport doesn't erase obligations. It multiplies them.

One state may expect military service. Another may impose tax filing. Another may treat you solely as its own citizen while you are inside its territory, which can limit outside help if something goes wrong.

If you're in a country of which you are also a national, your other citizenship may offer limited practical protection there.

That point matters more than many investors realise. Some people assume a second embassy can step in during a dispute, detention, family law matter, or property conflict. Often, the country where you hold nationality will treat you first and foremost as its citizen.

A simple operating habit

Keep a travel protocol. Experienced investors do this for entities and bank accounts. They should do it for citizenship too.

Use a one-page checklist covering:

- Which passport to use for each leg of travel

- Which name format matches each passport and title document

- Which residence permits remain valid

- Which country requires declarations on entry, exit, or tax residence

That reduces the small administrative mistakes that later become expensive legal ones.

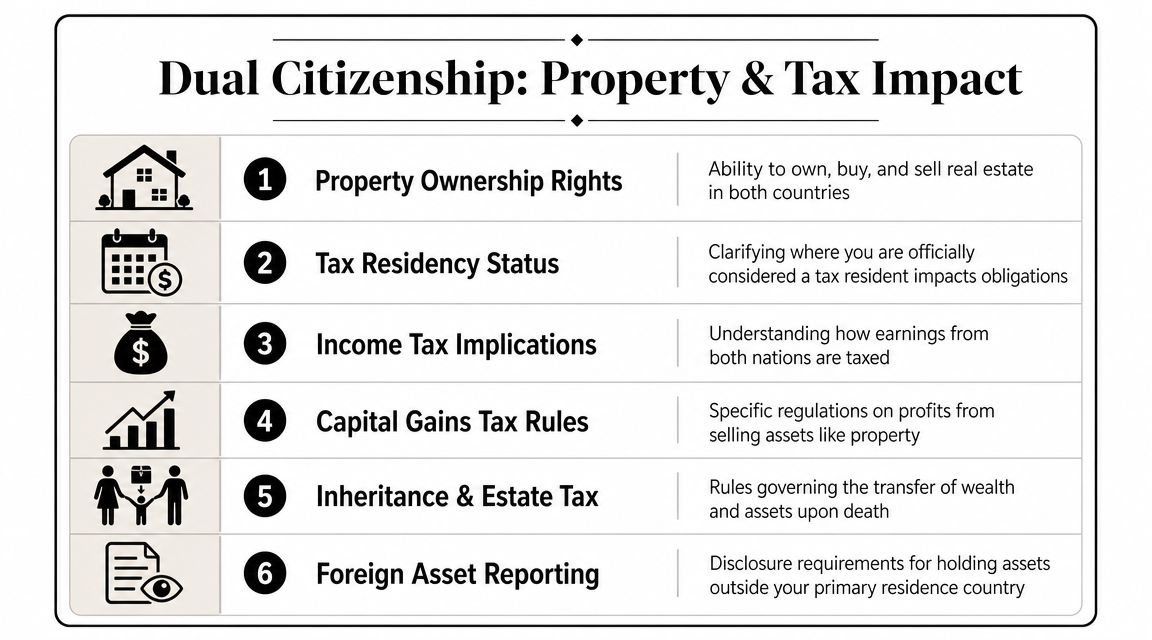

How Dual Citizenship Affects Property Investment and Tax

A common point of confusion is that investors hear “citizenship” and think “tax advantage”. Often, that's the wrong frame.

Dual citizenship can change your legal access to a market. It does not, by itself, determine where you pay tax. Tax residence, source of income, domestic law, and treaty rules usually do the heavier lifting.

A British framework allows its citizens to hold other nationalities, a position modernised by the British Nationality Act 1981. But the legal statuses run in parallel, not as one combined status. A British dual national is expected to use a British passport when entering or leaving the UK, while the other country may impose its own passport rules. That parallel structure is a useful reminder for tax and compliance analysis too (guidance on British dual nationality and parallel legal duties).

Early in any cross-border property review, I separate four questions. Investors who mix them together usually make poor decisions.

Question one: can you buy like a local

In some markets, citizenship or long-term status improves your position. You may face fewer restrictions on title, land categories, financing, or inheritance. In others, citizens and foreigners can both buy, but the process, lender appetite, or permitted use differs.

That's why dual citizenship can be strategically valuable for property investors. It may widen the range of assets you can legally buy or simplify ownership structures. But the answer is country-specific. It isn't automatic.

Question two: where are you tax resident

This is the issue investors most often miss. Nationality and tax residence are not the same thing.

A dual national might still be tax resident only in one country. Another investor might trigger residence in more than one jurisdiction because of days spent there, family ties, or the location of their main home. Rental income, gains on sale, and reporting obligations often depend more on residence and source rules than on the passport in your pocket.

Key takeaway: A second passport may open the door to a market. It doesn't tell you how the tax office will view your rental income or property sale.

For UK-facing investors, that gap is especially important because nationality status is separate from the UK's tax rules on residence and property taxation. In practice, readers often need a much clearer answer on whether dual citizenship changes issues such as SDLT, rental income tax, or inheritance exposure. That's a frequent blind spot in basic explainers (discussion of the gap between nationality and property tax questions).

A practical comparison can help. An investor with British and another nationality buying in London may still need to assess UK residence, overseas residence, and treaty position. Their citizenship alone won't settle those questions.

If you're reviewing disposal planning, this guide to capital gains tax on foreign property is a useful companion because gains analysis usually depends on jurisdiction, residence, and reliefs rather than nationality alone.

Question three: how is the income reported

Rental income is often taxable where the property sits. It may also need to be declared where you are tax resident. That doesn't always mean double tax in economic terms, because domestic reliefs or treaties may matter, but it often does mean double reporting.

Consequently, dual nationals often under-budget. They focus on acquisition and ignore annual compliance. A modest overseas rental can create a disproportionate paperwork burden if ownership, residence, and banking are spread across jurisdictions.

For investors considering flexible living arrangements rather than nationality itself, it's also worth comparing European digital nomad visas. In some cases, a residence route suits the investor's lifestyle better than chasing citizenship too early.

Here's a short explainer on cross-border property tax mechanics:

Question four: what happens on death or transfer

Inheritance planning is where dual citizenship can become highly relevant but still not determinative. Nationality may affect family rights in some legal systems. Residence, domicile concepts, local succession rules, forced heirship, and asset location may all matter as well.

For property investors, the practical answer is not to ask “does my second citizenship solve this?” Ask instead:

- Which country taxes the estate or transfer

- Which law governs succession to the property

- Whether local probate is required

- Whether the ownership structure still works for heirs

That's the investor's version of what dual citizenship means in real life. It's a planning factor. It is not a substitute for tax analysis.

Navigating Global Rules on Dual Nationality

Property investors often assume there is a global standard on dual nationality. There isn't. Countries vary sharply. Some are permissive. Some are selective. Some tolerate dual nationality in practice but make naturalisation harder, slower, or more conditional.

For investment planning, the right question isn't “which country is best?” It's “which legal system fits the way I want to live, own, and pass on assets?”

Established and emerging market approaches

The UK is relatively straightforward in principle. It allows British citizens to hold another nationality. That makes it comparatively workable for internationally mobile families who don't want to surrender an existing citizenship.

Portugal is widely seen as more open in approach. Investors often view it as part of a broader European mobility and residency strategy, especially where lifestyle use and eventual naturalisation are both on the table.

Spain is more nuanced and can be more restrictive depending on the nationality involved. That matters for investors who assume a residence route and a citizenship route are effectively the same. They're not.

UAE sits in a different category for many investors. It is a major property hub, especially for internationally mobile buyers, but citizenship analysis there is not the same as residency analysis. Many investors in Dubai focus on residency, ownership rules, and operating flexibility rather than assuming citizenship is the likely end point.

Dual Citizenship and Property Investment Rules A Snapshot

| Country | Allows Dual Citizenship? | Residency/Citizenship by Investment Path? | Key Investor Consideration |

|---|---|---|---|

| UK | Yes | Residency routes may lead to settlement and then naturalisation, subject to legal requirements | Citizenship is separate from UK tax residence and property tax treatment |

| Portugal | Generally open in approach | Residency-led routes are often more relevant than immediate citizenship | Investors should distinguish lifestyle planning from tax residence planning |

| Spain | Can be more restrictive depending on nationality | Residency options may exist, but citizenship outcomes need careful legal review | Don't assume naturalisation will allow retention of original nationality |

| UAE | Investor interest is often residency-led rather than citizenship-led | Residency pathways are usually the practical focus for property buyers | Ownership rights, visa status, and operational use often matter more than nationality |

What works and what doesn't

What works is choosing the jurisdiction that matches your actual objective.

- If you want mobility and lifestyle flexibility, a residence route may be enough.

- If you want long-term family rights, citizenship may matter more.

- If you want portfolio access, ownership rules and finance terms may matter more than either.

What doesn't work is treating citizenship as a trophy asset. Investors sometimes pursue it because it sounds strategic, then discover they really needed residence certainty, treaty analysis, or cleaner succession planning.

The best nationality strategy is the one that supports the portfolio you already intend to build, not the one that looks impressive on paper.

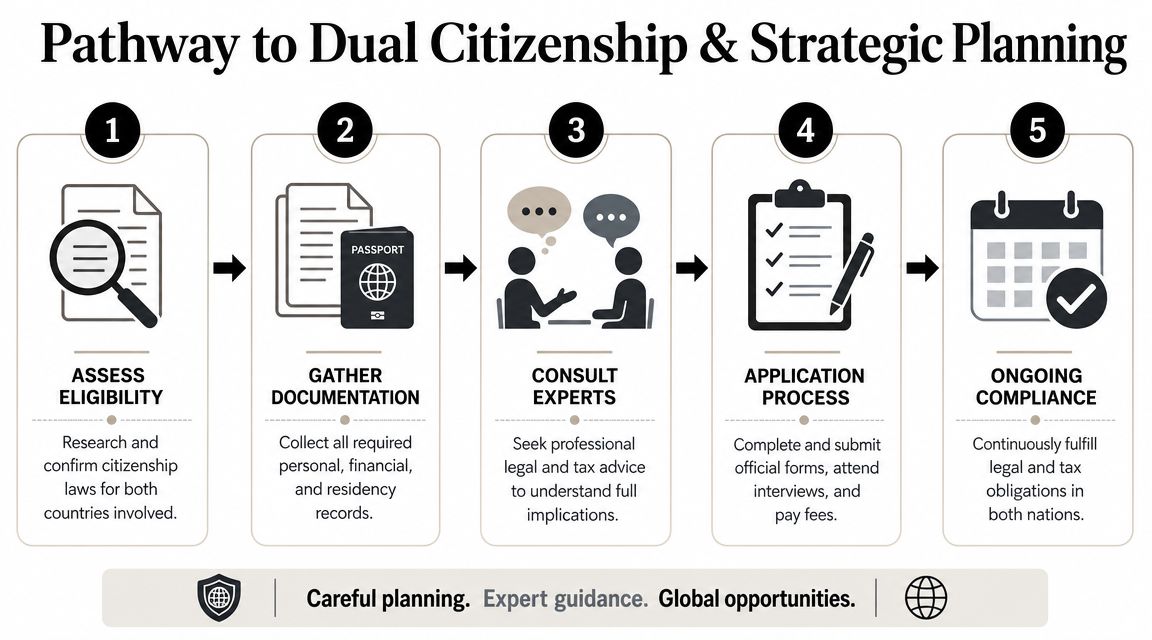

Confirming Your Eligibility and Strategic Planning

A frequent error is to begin incorrectly. Individuals often ask whether they should get dual citizenship before checking for an existing plausible claim through birth or descent.

For investors, good planning starts with legal eligibility and ends with a coordinated tax, residency, and family strategy.

Start with the routes that may already exist

Review your family line first. Parentage and place of birth can matter more than current residence. Then review any country where you already hold long-term residence and may later naturalise.

A sensible order is:

Check birth and ancestry

Look at parents, and where relevant, earlier generations. Match family facts against current nationality law, not assumptions or family stories.Review residence history

If you've already spent years in one country, naturalisation may be more realistic than you think.Assess investor routes carefully

Some programmes are marketed aggressively. The legal and tax consequences deserve more attention than the brochure.

For investors exploring mobility options linked to business and capital movement, this guide on a visa for investors helps frame the earlier-stage alternatives to citizenship.

Build a proper diligence file

Treat this like an acquisition file, not a casual enquiry.

Gather:

- Civil records: Birth, marriage, divorce, and name-change documents

- Immigration history: Residence cards, visas, entry records where needed

- Tax facts: Current residence position, filing footprint, entity ownership

- Property map: Which assets are held personally, jointly, or through companies

Then ask a harder question. If citizenship is approved, what changes for your portfolio?

That answer may touch lending access, family relocation, estate planning, and healthcare planning. For families relocating to Europe, medical coverage often becomes part of the compliance file as well. Anyone evaluating a move should also review practical issues like expat medical insurance for France where healthcare evidence can affect settlement planning.

Use specialist advice at the right stage

Nationality law, tax law, and property law don't sit neatly together. One adviser rarely covers all three in depth.

Use a joined-up team where needed:

- Nationality lawyer for entitlement and process

- Cross-border tax adviser for residence, reporting, and ownership structure

- Property lawyer in the asset jurisdiction for title, succession, and local constraints

Don't file first and analyse later. By the time citizenship is granted, you may already have triggered planning issues that should have been resolved in advance.

Think one generation ahead

The strongest plans usually aren't about the current buyer alone. They consider children, succession, future residence choices, and whether the next generation can hold or inherit property efficiently.

That's where dual citizenship can be powerful. Not because it sounds prestigious, but because it can create lawful continuity across countries if it fits the family and the assets.

Frequently Asked Questions for Investors and Expats

Does dual citizenship let me avoid foreign-buyer rules

Sometimes, but not automatically. If a country reserves certain ownership rights to its citizens, holding that citizenship may improve your position. But many restrictions depend on residency status, property type, land classification, or local approvals. Check the property law, not just the passport rule.

Does a second passport change my UK property taxes

Not by itself. The key issue is usually tax residence and the nature of the asset and income. Investors often assume nationality changes SDLT, rental tax, gains, or inheritance treatment across the board. It usually doesn't. The legal analysis sits elsewhere.

Can I choose whichever passport is more convenient every time I travel

Not always. Some countries expect their own citizens to use that country's passport for entry and exit. Keep a written travel protocol if you move frequently between portfolio jurisdictions.

Is dual citizenship better than a residence visa for investors

It depends on the goal. If you want flexible living rights and operational ease, a residence route may be enough. If your plan involves long-term family settlement, political rights, or passing status to children, citizenship may be more valuable.

What's the most overlooked issue for expat investors

Ongoing administration. Renewals, filings, local registrations, tax disclosures, succession planning, and document consistency across countries all matter. Investors spend time on the acquisition and neglect the operating burden.

For people living between jurisdictions, the basics of connectivity and compliance also matter more than they used to. This practical guide to expat use cases is a useful reminder that cross-border life runs on small operational details as much as big legal ones.

Can my children benefit from my second citizenship

Often yes, but never assume it. Eligibility may depend on when you acquired the nationality, where the child is born, and whether registration is required. If family planning is part of the property strategy, confirm the intergenerational rules early.

If you're comparing countries, tax exposure, ownership rules, and investor visas, World Property Investor offers practical guides to help you research markets, understand cross-border property fundamentals, and make better long-term decisions before you buy.