For a growing number of UK property investors, the decision to move to Portugal from the UK is not an emotional whim but a calculated financial strategy. It represents a move to secure assets, diversify into a Euro-denominated economy, and regain lifestyle and investment benefits within the EU. This guide provides a practical, data-driven analysis for global property investors considering this relocation.

Why Investors Are Moving to Portugal from the UK

The post-Brexit landscape has compelled many UK-based investors to reassess their long-term strategies. Portugal has emerged as a clear frontrunner, offering a powerful combination of financial opportunity and an exceptional quality of life. This is not simply a lifestyle trend; it is a strategic relocation driven by solid market fundamentals.

Portugal's stable political climate and resilient property market provide a robust hedge against economic uncertainty. For UK investors, it offers a direct route to diversifying assets while regaining a valuable foothold within the European Union.

The Market Validator: A Thriving UK Expat Community

A significant factor underpinning the investment case is the substantial British expatriate community. According to ONS and Portuguese government data, this demographic has been growing for decades, creating a large and stable market.

In 2006, an estimated 49,000 British nationals were already registered residents in Portugal, a figure that has swelled considerably since. This long-established community validates the market, creating reliable and sustained demand for high-quality rental properties and English-language services. This demographic acts as a powerful market driver, ensuring a dependable tenant pool for buy-to-let investors and fuelling consistent demand for specific amenities.

Investor Takeaway: The presence of a large, established British community de-risks the investment from a demand perspective. It signals a mature market with proven rental appetite, not a speculative bet on an unproven location.

Beyond the Algarve: A Look at Market Dynamics

While the Algarve has long been the traditional heartland for British buyers, savvy investors are now exploring opportunities across the country. Each region offers a different investment profile, from high rental yields to strong capital appreciation potential.

Established Markets: The Algarve

The Algarve remains a rental income powerhouse, driven by a relentless flow of tourism and a large community of retirees and remote workers. It offers some of the highest and most consistent rental yields in Portugal. Property values here are mature, offering stability and predictable income rather than speculative growth.

Growth Markets: Lisbon and Porto

As Portugal's economic engines, Lisbon and Porto attract a different demographic: young professionals, tech entrepreneurs, and digital nomads. Investment here is driven by capital growth potential and strong demand for long-term rentals. While entry prices are higher, the potential for significant asset appreciation is a key draw.

Emerging Markets: The Silver Coast and Comporta

For investors seeking the next frontier, areas like the Silver Coast (north of Lisbon) and Comporta (south of Lisbon) offer compelling value. These regions are experiencing a surge of interest due to their authenticity and lower price points compared to the Algarve, presenting a clear opportunity for early-stage capital growth. Exploring the nuances of these locations is key, as detailed in our guide to understanding daily life in Portugal.

Ultimately, the move to Portugal from the UK is being framed less as a retirement plan and more as a sophisticated investment in one's financial future—offering diversification, stability, and lifestyle benefits in a single, strategic package.

Post-Brexit Visa and Residency Options for Investors

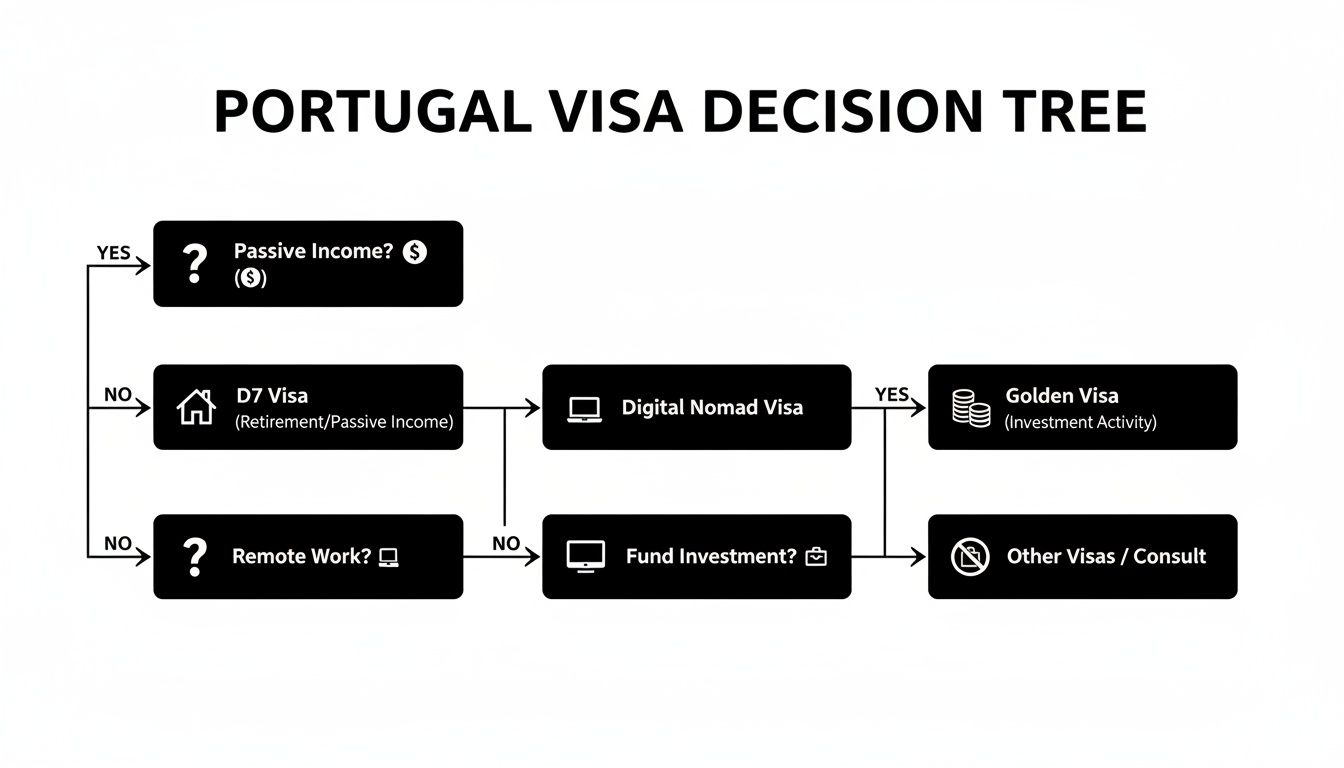

Since Brexit, UK citizens are classified as third-country nationals, meaning a visa is a prerequisite for residency. Portugal offers several well-defined pathways tailored to investors, remote workers, and individuals with passive income. Selecting the correct route is critical and depends entirely on your financial structure and long-term objectives.

The D7 Visa: For Passive Income and Retirees

The D7 Visa, or Passive Income Visa, is a popular route for UK investors and retirees. It requires proof of a stable, recurring income from outside Portugal. The financial threshold is notably reasonable.

To qualify, a single applicant must demonstrate a passive income equivalent to at least the Portuguese minimum wage, which for 2026 is approximately €11,040 per annum. This figure increases for a spouse or dependents. This income can be derived from various sources, including rental income from a UK property portfolio, share dividends, royalties, or pension payments.

Investor Takeaway: For a property investor, the D7 Visa is highly practical. The rental yield from a UK buy-to-let portfolio can directly satisfy the income requirement for the residency application.

The D8 Digital Nomad Visa: For Remote Professionals

The D8 Digital Nomad Visa is designed for UK professionals who are employed by non-Portuguese companies or operate their own business with international clients. This has become a favoured option for younger professionals and consultants.

The financial requirement is higher than the D7, demanding a monthly income of at least four times the Portuguese minimum wage, which equates to approximately €3,680 per month in 2026. This visa allows you to transfer your UK or international career to a Portuguese base.

Investor Takeaway: The D8's flexibility is a key advantage. It permits you to reside in Portugal while managing international investments—including a UK property portfolio—without being tied to local employment.

Comparing Portugal's Key Visa Routes for UK Investors

The table below provides a clear comparison of the primary visa routes, enabling you to align your financial profile with the most suitable option.

| Visa Type | Primary Requirement | Minimum Investment/Income | Best For | Key Investor Benefit |

|---|---|---|---|---|

| D7 Passive Income Visa | Stable passive income from outside Portugal. | €11,040 per year (single applicant) | Retirees, landlords, investors with dividend/royalty income. | Low financial threshold; uses existing income streams for residency. |

| D8 Digital Nomad Visa | Remote work or self-employment income from foreign sources. | €3,680 per month (single applicant) | Remote professionals, freelancers, business owners. | Live in Portugal while managing a UK or global career/business. |

| Golden Visa | Qualifying investment into the Portuguese economy. | €500,000 into an approved investment fund. | High-net-worth investors seeking flexibility and EU access. | Minimal physical presence required (7 days/year); clear path to EU citizenship. |

The Golden Visa via Investment Funds

While the direct property purchase route for the Golden Visa was terminated, the programme remains highly attractive for high-net-worth individuals through its investment fund option. This pathway requires a minimum investment of €500,000 into a qualifying, Portuguese-regulated investment fund.

This route offers two distinct advantages for sophisticated investors:

- Strategic Diversification: It allows capital to be deployed away from a single property asset and into professionally managed funds spanning sectors like technology, renewable energy, or private equity.

- Unmatched Flexibility: The Golden Visa imposes the most relaxed stay requirement, demanding an average of just seven days per year in Portugal. This is ideal for investors who require EU residency and visa-free travel without committing to a full-time move.

For those prioritising EU access and a long-term path to citizenship without the burden of full-time residency, the Golden Visa remains a strategic powerhouse. For a deeper analysis, you can learn more about the Portugal Golden Visa fund route in our detailed guide.

A UK Investor's Guide to Buying Portuguese Property

The Portuguese property acquisition process differs significantly from the UK system. A UK-centric mindset can lead to costly errors. Methodical due diligence and assembling a professional team are fundamental to a secure investment.

Your most critical partner is a specialist property lawyer (advogado). Their role extends beyond simple conveyancing; they conduct forensic checks on property deeds, land registry records, and municipal permissions to ensure the asset is free of undisclosed debts or legal encumbrances.

The Essential First Steps

Before any transaction, a foreign buyer must obtain a Portuguese fiscal number, the Número de Identificação Fiscal (NIF). This is a non-negotiable requirement for opening a bank account, signing contracts, and the final property purchase. An advogado can typically procure a NIF on your behalf within a few days.

Following this, a Portuguese bank account should be opened to manage the flow of funds for the deposit, taxes, and final payment. With these two elements in place, you are legally prepared to make an offer.

Understanding the Financial Commitments

The acquisition costs associated with a Portuguese property purchase can be significant and must be budgeted for accurately. The first major financial milestone is the signing of the Promissory Contract of Purchase and Sale (CPCV). This is a legally binding agreement locking in the sale terms, at which point a deposit of 10% to 20% of the purchase price is paid.

Investor Takeaway: The CPCV provides strong protection for both parties. If the seller defaults, they are obligated to repay double the deposit. If the buyer withdraws, the deposit is forfeited. It ensures commitment to the transaction.

After the CPCV is signed but before the final deed, property transfer taxes must be paid. These are the primary ancillary costs to factor into your budget:

- IMT (Imposto Municipal sobre as Transmissões Onerosas de Imóveis): The main property transfer tax, calculated on a sliding scale based on the property’s value and use (main home or second home).

- IS (Imposto do Selo): Stamp Duty, levied at a flat rate of 0.8% of the property value declared in the final deed.

A Worked Example: Acquisition Costs

This example illustrates the total acquisition cost for a €500,000 second home, a common budget for UK investors.

| Cost Item | Description | Estimated Cost |

|---|---|---|

| Property Price | The agreed sale price. | €500,000 |

| IMT (Transfer Tax) | Calculated at the applicable rate for a second home. | ~€28,855 |

| IS (Stamp Duty) | 0.8% of the purchase price. | €4,000 |

| Legal Fees | Typically 1-1.5% of the purchase price + VAT. | ~€7,380 |

| Notary & Registration | Fixed fees for recording the deed. | ~€1,000 |

| Total Cost | Total capital required for the acquisition. | ~€541,235 |

Prudent financial planning requires budgeting for an additional 8-10% on top of the purchase price to cover all taxes and fees. If you're looking specifically at urban hotspots, our guide on how to buy a house in Lisbon offers more detailed local insights.

Managing Your Tax Obligations in the UK and Portugal

Effective tax management is a non-negotiable component of a successful international move. When you move to Portugal from the UK, understanding your tax position from day one is essential for asset protection and legal compliance.

The process begins with obtaining a Portuguese tax number (Número de Identificação Fiscal – NIF) and opening a local bank account. These are foundational steps for any financial activity in Portugal.

Defining Your Tax Residency Status

You will generally become a tax resident in Portugal if you spend more than 183 days in the country within any 12-month period. Alternatively, maintaining a primary home in Portugal that suggests an intention of habitual residence can also trigger tax residency.

Once you are a Portuguese tax resident, you are potentially liable for tax in Portugal on your worldwide income. The Portugal-UK Double Taxation Agreement (DTA) is a critical treaty designed to prevent income from being taxed in both countries. It clarifies which nation has the primary right to tax different income streams, such as UK rental income, pensions, or capital gains.

Investor Takeaway: The DTA is highly significant for property investors. It stipulates that income from a UK property portfolio remains taxable in the UK first. This income is then declared in Portugal, where a credit is given for the UK tax already paid, thereby avoiding double taxation.

Proactive planning is paramount. Seeking integrated tax advice from professionals who understand both UK and Portuguese systems before you move is a critical step. This allows for the optimal structuring of assets for maximum tax efficiency under the DTA.

The Non-Habitual Resident (NHR) Scheme in 2026

The original Non-Habitual Resident (NHR) scheme, a major draw for UK expatriates for many years, has now ended for new applicants. By 2026, this regime has been fully replaced by a new, more targeted incentive.

The original NHR offered broad benefits, including a flat 20% tax on certain professional incomes and exemptions on most foreign income. Individuals who secured NHR status under the old rules will continue to benefit for their ten-year term, but new arrivals in 2026 must adhere to the new framework.

The successor scheme, often referred to as 'NHR 2.0' or the Tax Incentive for Scientific Research and Innovation (IFRICI), is far more specific. It retains a 20% flat tax rate on Portuguese-source employment or self-employment income, but is restricted to individuals in designated high-value professions. These roles are narrowly defined and typically include higher education teachers, scientific researchers, and qualified positions within certified technology and innovation companies.

For most UK investors, particularly those reliant on passive income like rent or pensions, this new scheme offers limited advantages. Foreign-source pension income, for instance, is now generally taxed at Portugal's standard progressive rates. Understanding the tax implications is therefore vital; learn more by exploring our analysis of capital gains tax on foreign property.

The Practicalities of Relocation and Settling In

Once legal and financial frameworks are in place, the focus shifts to the logistical execution of your move to Portugal from the UK. These practical details—healthcare, education, and transport of possessions—are critical for a seamless transition.

Navigating Healthcare and Education

As a resident in Portugal, you are entitled to register with the public healthcare system, the Serviço Nacional de Saúde (SNS). While comprehensive, many investors supplement this with private health insurance for faster access to specialists, a wider choice of facilities with English-speaking staff, and enhanced comfort.

For families with children, schooling is a primary consideration. Portugal offers two main pathways:

- Local State Schools: This provides full cultural and linguistic immersion and is free of charge, though costs for books and materials apply.

- Private International Schools: Concentrated in the Algarve, Lisbon, and Porto, these schools typically follow a British or International Baccalaureate (IB) curriculum. Fees are significant, ranging from €8,000 to over €20,000 annually, but they ensure educational continuity.

Investor Takeaway: The school decision represents a trade-off between cultural immersion and educational continuity. The optimal choice depends on the children's ages, adaptability, and your family's long-term residency plans.

Managing the Logistics of Your Move

The physical move now involves additional post-Brexit bureaucracy. Obtaining multiple quotes from international removal companies with recent UK-to-Portugal experience is essential to navigate customs declarations. A full household move can cost between £3,000 and £8,000, depending on volume and service level.

Importing a UK-registered vehicle has become complex and costly due to customs duties (VAT) and a significant vehicle import tax (ISV). For many, it is more financially prudent to sell their UK vehicle and purchase a left-hand-drive car upon arrival in Portugal.

Finally, you are required to exchange your UK driving licence for a Portuguese one after becoming a resident. This process is administered by the IMT (Institute of Mobility and Transport) and should be initiated promptly to ensure you remain legally compliant. To ensure your budget is realistic, it is wise to review the typical cost of living in Portugal to understand day-to-day expenses.

Investor Questions Answered

This section addresses common practical questions from UK investors preparing to relocate to Portugal.

Can I Still Use the NHS After Moving to Portugal?

Once you become an official resident of Portugal, your routine access to the NHS in the UK ceases. Your healthcare will be managed by the Portuguese national system, the Serviço Nacional de Saúde (SNS), upon registration. For emergency medical needs during short trips back to the UK, a Global Health Insurance Card (GHIC) provides cover, but it does not apply to planned medical treatment. For this reason, many British expatriates opt for comprehensive private health insurance in Portugal.

How Difficult Is Obtaining a Portuguese Mortgage as a UK Citizen?

Obtaining a mortgage in Portugal as a non-resident is feasible, but lenders require a higher level of financial commitment. Expect to provide a larger deposit, typically in the 30-40% range, compared to the 10-20% standard for residents. A comprehensive file of your UK financial history is required, including tax returns (P60s or Self-Assessments), proof of income, and bank statements.

Investor Takeaway: The entire mortgage application process is conducted in Portuguese. Engaging a specialist mortgage broker with experience assisting British buyers is essential to navigate the bureaucracy and avoid potential misunderstandings.

How Does Brexit Affect My UK Pension in Portugal?

Your UK pensions, including the State Pension and private schemes, can be paid directly into a Portuguese bank account. The UK Government continues to apply annual increases (uprating) to the UK State Pension for residents in Portugal. Under the UK-Portugal Double Taxation Agreement, this income is taxed in Portugal as per your residency status. Given the recent reforms to the NHR scheme, professional financial advice is critical to ensure your pension is structured for optimal tax efficiency.

What Are the Rules for Bringing Pets from the UK to Portugal?

Since Brexit, pet transport from the UK to the EU requires specific documentation. EU pet passports issued in Great Britain are no longer valid. Your pet must have a microchip, a valid rabies vaccination (administered at least 21 days before travel), and an Animal Health Certificate (AHC). The AHC must be issued by an official veterinarian in the UK no more than 10 days before your travel date.

Are Property Prices Still Rising in Portugal?

Yes, the Portuguese property market continues to show growth, albeit at a more sustainable pace than in previous years. Official data from the National Statistics Institute (INE) confirms consistent year-on-year growth. Lisbon and Porto remain robust markets, while emerging areas like the Silver Coast and parts of the Alentejo offer lower entry points and strong potential for future appreciation. The sustained demand from the large UK resident population provides a solid foundation for the market, indicating resilience and maturity rather than a speculative bubble.

Planning a strategic move or investment requires expert guidance. World Property Investor provides in-depth analyses, market data, and practical guides to help you navigate international real estate with confidence. Explore our resources at https://www.worldpropertyinvestor.com.