For global property investors evaluating European markets, Portugal's cost of living is not merely a lifestyle benefit; it is a core economic driver. The country's affordability compared to its Western European neighbours directly fuels rental demand, reduces vacancy risk, and ultimately supports stronger investment returns. This financial accessibility acts as a powerful magnet for a diverse and stable stream of tenants, from international remote workers and retirees to local professionals, underpinning the market's long-term fundamentals.

This guide provides a practical, data-driven analysis of the cost of living in Portugal, offering actionable insights for investors looking to build a resilient and profitable property portfolio.

Why Portugal's Cost of Living is a Strategic Advantage

A thorough understanding of a target market's cost of living extends beyond simple budgeting. In Portugal, this affordability is the cornerstone of the investment thesis. When day-to-day expenses such as groceries, transport, and utilities are low, tenants possess greater disposable income. This financial headroom translates directly into an enhanced ability to pay rent consistently and on time—a simple but critical factor that significantly de-risks a buy-to-let portfolio.

The UK Comparison: A Data-Led Perspective

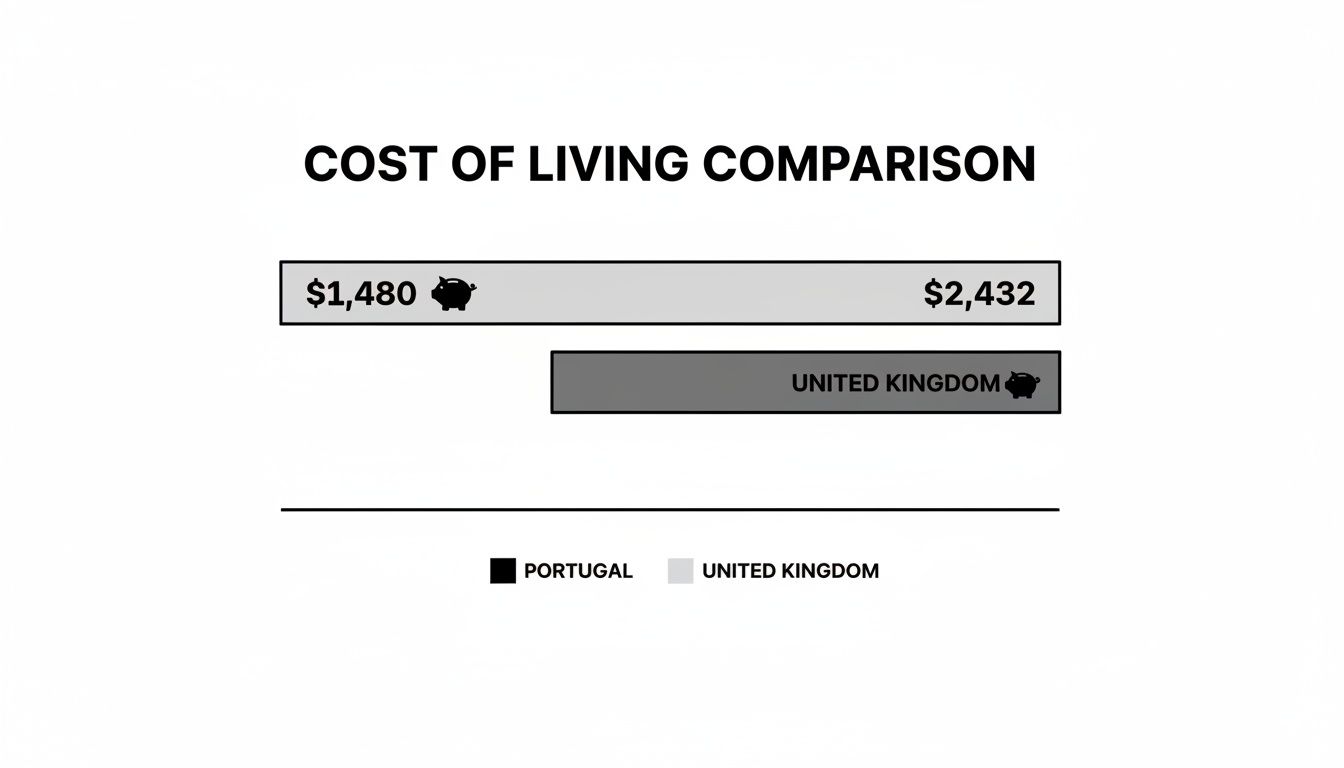

To contextualise this advantage, a direct comparison with the United Kingdom is highly instructive. Credible economic forecasts for 2026 indicate that the cost of living in Portugal is approximately 39% lower than in the UK.

For a single individual, the average monthly expenditure in Portugal is estimated at around £1,170 ($1,480), a stark contrast to over £1,920 ($2,432) in the UK. This data, corroborated by sources like the ONS and local economic bodies, highlights a significant strategic gap.

For an investor, this disparity creates several clear benefits:

- Sustained Rental Demand: Portugal’s affordability ensures a consistent influx of individuals from more expensive nations, keeping demand for quality rental properties high.

- Lower Vacancy Risk: A financially secure tenant base leads to longer tenancies and fewer defaults, which is fundamental to maximising occupancy rates and protecting income streams.

- Attractive Yields: While property prices have risen, they remain accessible compared to major UK hubs. This lower cost of entry, combined with strong and reliable rental income, creates a compelling formula for attractive net rental yields.

To provide a clear, high-level view, the following table breaks down the monthly expenses for a single person.

Monthly Cost of Living Snapshot 2026: Portugal vs United Kingdom

| Expense Category | Portugal (Average Monthly Cost) | United Kingdom (Average Monthly Cost) | Key Investor Takeaway |

|---|---|---|---|

| Rent (1-bed city flat) | £650 – £850 | £900 – £1,200+ | Lower rent makes Portugal a magnet for tenants seeking better value, ensuring high demand. |

| Utilities (basic) | £90 | £180 | Significantly lower operational costs improve tenant affordability and rental payment security. |

| Groceries | £200 | £280 | Day-to-day living is cheaper, which frees up tenant income for consistent rent payments. |

| Transport (monthly pass) | £35 | £70 | Reduced commuting costs add to the overall affordability appeal, widening the pool of potential tenants. |

| Total (Approx.) | ~£1,170 | ~£1,920 | The ~39% cost differential underpins strong, consistent rental demand and a lower-risk investment environment. |

The data clearly shows that financial pressure on tenants is substantially lower in Portugal, making rental income more secure.

For property investors, a low cost of living is not just an attractive feature; it's a strategic advantage. It underpins tenant affordability, which in turn secures rental income and enhances the long-term stability and profitability of your assets.

This guide will now delve deeper into specific costs—from housing and utilities to taxes and daily expenses—to provide the data needed to accurately model returns. We will also touch upon how these economic fundamentals can be paired with residency options. For further information, our guide on the Portugal Golden Visa may be helpful.

Decoding Portugal's Housing and Rental Market

While Portugal's low cost of living is an initial draw, for serious property investors, the mechanics of the housing market are what truly matter. This involves looking beyond lifestyle headlines to analyse the numbers that drive profit: purchase prices, rental income, and the resulting yields.

Portugal is not a monolithic market; it is a collection of distinct micro-markets. A significant difference exists between prime Lisbon or Porto and emerging suburban areas. This creates opportunities for various investment strategies, from targeting high-end corporate lets to more affordable family homes. Even in premium locations, the overall cost base is often more favourable than in other major European hubs.

This difference in day-to-day expenses is what gives the rental market its resilience, attracting a steady flow of tenants from more expensive countries.

Rental Prices and Yield Expectations

The on-the-ground data presents a compelling case for international investors. Analysis of 2026 data reveals a clear market segmentation. A one-bedroom flat in a prime city centre may rent for approximately €930 per month, while a three-bedroom apartment can command around €1,675.

Outside the main urban centres, the financial landscape shifts. The same one-bedroom apartment might rent for closer to €711, with a three-bedroom property fetching around €1,192. This creates two distinct tiers for investment. Further detail on these costs can be found at imin-portugal.com.

Rent, however, is only one part of the equation. The true measure of an investment's performance is its gross rental yield—the total annual rent as a percentage of the property's purchase price. Here, Portugal’s lower property prices create a powerful formula for profitability.

In prime areas of Lisbon or Porto, investors can realistically expect gross rental yields of 3.5% to 5.5%. In emerging suburbs or smaller cities, however, yields can push towards 6% or even higher. These figures compare very favourably with many parts of the UK, where higher property prices often compress yields.

Mortgages and Financing Advantages

Portugal’s financing landscape offers welcome advantages for overseas buyers. While a non-resident will need to prepare thorough documentation to secure a mortgage, the terms are often attractive.

- Loan-to-Value (LTV) Ratios: Most non-resident buyers can expect to secure a mortgage covering 60-70% of the property’s value, allowing for effective capital leverage.

- Interest Rates: Historically, Portuguese mortgage rates have been competitive. While influenced by the European Central Bank, they often track UK rates and can sometimes be lower, particularly on variable-rate products.

- Affordability Calculations: When lenders assess repayment capacity, Portugal's lower cost of living works in an applicant's favour, suggesting greater disposable income to service the mortgage.

This accessible financing, combined with robust rental demand, makes it possible to structure an investment where rental income comfortably covers the mortgage and operational costs, potentially leading to a cash-flow-positive asset from day one.

For investors focused on the capital, our guide on buying a house in Lisbon provides a deeper analysis of the acquisition process.

Analysing Daily Expenses and Tenant Affordability

A successful buy-to-let investment hinges on more than the purchase price and rental income. The stability of your investment is directly linked to your tenant’s financial health, which is shaped by the cost of living in Portugal. Understanding the full spectrum of daily expenses—from groceries and utilities to transport and childcare—provides strategic intelligence for any discerning investor.

When tenants have more budgetary flexibility after covering basic needs, your rental income becomes far more secure. Portugal's affordability in these everyday categories is a fundamental advantage that de-risks your asset.

Utilities and Groceries

One of the most immediate financial benefits for residents in Portugal is the cost of basic utilities. For a standard 85m² apartment, the combined monthly bill for electricity, heating, water, and refuse collection typically falls between €110-€130. This is markedly lower than in the UK, where similar costs often exceed £200, instantly improving a tenant’s ability to manage their monthly budget.

Groceries follow a similar, reassuring trend. A weekly shop for a couple, including fresh produce from the local mercado, meat, and wine, can average around €100-€120. This represents a significant saving compared to major UK cities, freeing up household income that can be comfortably allocated to rent.

Transport and Childcare Costs

A granular analysis of daily expenses reveals even starker contrasts with the UK, offering direct insights for investment strategy. For instance, data for 2026 shows that transportation costs in the UK are 56.6% higher than in Portugal. This affordability widens the viable commuter belt, making properties in emerging suburbs with good transport links more attractive to tenants.

The difference in childcare expenses is even more dramatic. In the UK, childcare costs can be up to 2.4 times higher, a prohibitive expense that often shapes where families can live. Portugal’s more affordable childcare makes it a highly attractive destination for young professional families, signalling strong, stable demand for two and three-bedroom rental properties.

As an investor, these data points are not just trivia; they are demand signals. Lower transport costs validate investment in well-connected suburbs, while affordable childcare points directly to a robust market for family homes.

To help put these numbers in context, the following table provides a snapshot of a typical monthly budget for a couple living in Portugal, before rent. This offers a baseline for understanding what potential tenants can comfortably afford.

Typical Monthly Household Budget in Portugal 2026 (Excluding Rent)

| Expense Category | Estimated Monthly Cost (Couple) | Notes for Property Investors |

|---|---|---|

| Utilities | €110 – €130 | Significantly lower than UK averages, increasing disposable income for rent. |

| Groceries | €450 – €500 | Affordable fresh food supports a high quality of life on a reasonable budget. |

| Transport | €100 – €150 | A monthly pass is affordable; lower running costs make suburban properties viable. |

| Healthcare | €80 – €150 | Private insurance is common and affordable, a key part of an expat’s budget. |

| Leisure/Dining Out | €200 – €300 | A vibrant café and restaurant culture is accessible, a major lifestyle draw. |

| Total (Excluding Rent): | €940 – €1,230 | This baseline shows strong tenant affordability for mid-market rental prices. |

This breakdown reveals a crucial advantage: after covering all essential living costs, a professional couple still has significant capacity to afford quality rental accommodation without financial stress.

Healthcare and Other Essentials

While Portugal offers a high-quality public healthcare system (the SNS), many expatriates and affluent locals opt for private health insurance for faster access to specialists. Monthly premiums are very competitive, often a fraction of equivalent cover in the US, making it an affordable part of an expat’s budget. You can find detailed information on options like Health Insurance for Expatriates in Portugal.

The combination of these savings underpins tenant affordability. A lower overall cost of living in Portugal creates a resilient tenant base with the financial capacity to meet rental obligations, reducing the risk of defaults and vacancies—two of the biggest threats to rental yield. Our complete guide to the lifestyle and practicalities of life in Portugal offers further insights into what makes the country so appealing to a global audience.

A Regional Look at Portugal's Investment Hotspots

Portugal should not be viewed as a single market. An investor focused on Lisbon’s prime postcodes will have a completely different experience—and see different returns—than one buying in the Algarve or an emerging inland city. The relationship between the cost of living in Portugal and property prices varies dramatically by region, creating a spectrum of investment opportunities. The choice lies between pursuing long-term capital growth in established hubs or targeting higher immediate rental yields in lifestyle and emerging markets.

Established Markets: Lisbon and Porto

Lisbon and Porto are the country’s economic and cultural engines, attracting a constant stream of tenants, from international tech talent to digital nomads. This creates relentless rental demand and has historically supported strong capital growth. However, this popularity comes at a price.

Lisbon (Established): Property here is at a premium. A one-bedroom flat in a sought-after central neighbourhood can exceed €350,000. While rental income is solid, the high purchase price means gross yields often land in the 3.5% to 5.5% range. The strategy is typically focused on long-term capital appreciation.

Porto (Established): Though a major city, Porto offers a more accessible entry point, with prices often 15-25% lower than in Lisbon. This allows investors to achieve better yields, sometimes approaching 6% in the right locations.

The Algarve: A Lifestyle-Driven Market

The Algarve operates on a different set of rules, driven almost entirely by tourism and lifestyle demand. It attracts a mix of seasonal holidaymakers, foreign retirees, and remote workers. This creates a dual market for short-term holiday lets and traditional long-term rentals.

In the Algarve, investment success hinges on understanding seasonality. A property might generate the majority of its annual income during peak summer months, requiring a different cash flow management approach compared to a city apartment with a 12-month lease.

While the general cost of living here is lower than in Lisbon, property prices in prime coastal spots like Vilamoura or Lagos can be high. The primary opportunity often lies in the lucrative holiday rental market, which can generate high weekly rates but also involves higher management costs and vacancy risks in the off-season. You can explore more granular data in our full report on Portugal housing prices.

Emerging Markets: Inland and Silver Coast

For investors prioritising stronger cash flow and a lower cost of entry, the inland regions and the Silver Coast present a compelling alternative. University cities like Coimbra, northern hubs like Braga, and towns along the Silver Coast offer a much lower barrier to entry, with properties available for 30-50% less than in Lisbon.

This affordability translates directly into higher potential yields, which can exceed 7% for a well-managed property. The tenant base shifts towards students, local professionals, and families drawn by the significantly lower cost of living. This strategy trades the explosive capital growth potential of major cities for stronger, more immediate cash flow.

Understanding Taxes and Your Investment Returns

Gross rental yield and capital growth figures are only part of the investment analysis. A sophisticated investor knows that the true return on investment (ROI) is the net figure after taxes. Understanding Portugal’s tax landscape is not an afterthought but a critical component of financial modelling. A clear grasp of these fundamentals is essential for working confidently with local advisors and ensuring your projections are accurate.Core Taxes for Property Investors

For a non-resident investor in Portugal, three main taxes will directly impact your net returns. These should be treated as fixed operational costs, similar to insurance or management fees.

Rental Income Tax (IRS): Income generated from renting a Portuguese property is taxed at a flat rate of 25% for non-resident individuals. This is a significant deduction, making accurate rental forecasts crucial for understanding real-world cash flow.

Annual Property Tax (IMI): This is the Portuguese equivalent of UK council tax. Known as Imposto Municipal sobre Imóveis, IMI is a municipal tax based on the property’s rateable value, with rates typically falling between 0.3% and 0.45% per year.

Capital Gains Tax (CGT): Upon selling the property, any profit is subject to capital gains tax. For non-residents, this is charged at a flat rate of 28%. Understanding the rules around CGT is vital for planning a profitable exit strategy. Our detailed article provides more context on how capital gains tax on foreign property works for UK investors.

The Non-Habitual Resident (NHR) Scheme

It is important to note that the well-known Non-Habitual Resident (NHR) scheme, which once offered significant tax advantages, was substantially changed for new applicants from 2024. While existing NHR beneficiaries are protected under legacy rules, new arrivals fall under a much narrower regime aimed at specific scientific and innovation roles. For most new property investors, the standard tax rates should be used for all financial planning.

The key takeaway for investors is to model your returns based on the standard tax rates. A robust financial plan accounts for a 25% tax on rental income and a 28% tax on eventual capital gains, ensuring your yield calculations are realistic and conservative.

When dealing with international investments, ensuring your financial documents are correctly certified for Portuguese authorities is paramount. A detailed guide to financial services translation can help ensure all paperwork meets local legal standards, preventing costly delays and complications.

Your Strategic Takeaways for Investing in Portugal

For the globally-minded investor, Portugal's appeal is rooted in a simple but powerful concept: the country's low cost of living is not just a lifestyle perk but a fundamental market driver that creates a uniquely stable and profitable environment for buy-to-let investment. It is the core of the rental market's resilience.

At its heart, Portugal's affordability acts as a powerful economic engine. It guarantees consistent demand from a diverse tenant base—from international remote workers to local families—all drawn by the high quality of life achievable on a reasonable budget. This sustained demand is the bedrock of a secure rental market.

Cost of Living as a Strategic Advantage

The key insight is that the affordable cost of living in Portugal directly benefits your bottom line. It provides tenants with financial headroom, which dramatically lowers the risk of rental arrears and vacancies. When daily essentials are manageable, tenants can comfortably meet their rent obligations.

This affordability also has a direct impact on operational costs. Property management, maintenance, and repair services are generally more cost-effective than in markets like the UK or North America. These savings on overheads contribute directly to a healthier net yield.

For a global property investor, Portugal's market dynamics offer a compelling formula. The combination of accessible property prices, strong rental demand fuelled by affordability, and lower operational costs creates a clear pathway to achieving healthy, sustainable returns.

Yields and Regional Opportunities

A smart investment strategy must be tailored to Portugal's distinct regional markets, each offering a different balance of risk and reward.

Established Markets (Lisbon & Porto): These markets are defined by long-term capital appreciation, driven by a high-earning professional and international tenant base. Higher entry prices mean gross rental yields are typically more moderate, often sitting between 3.5% and 5.5%.

Lifestyle Hubs (The Algarve): Here, the focus shifts to a dual market of long-term lets and lucrative short-term holiday rentals. While property can be expensive in prime coastal spots, the potential for high seasonal income is significant.

Emerging Markets (Inland & Silver Coast): For investors who prioritise immediate cash flow, these regions offer the most attractive proposition. Lower property prices can push gross rental yields towards 7% or higher, trading the capital growth potential of major cities for stronger, more immediate income.

When these elements are combined, it becomes clear how Portugal’s economic fundamentals create a resilient and profitable landscape for property investment. It is this balance of lifestyle appeal and solid financial metrics that places Portugal firmly on the map for savvy global investors.

Frequently Asked Questions for Investors

Once the high-level market trends are understood, practical questions arise regarding the real-world implications of Portugal's cost of living. How does it affect your tenants, and how do the country's lower costs impact your bottom line as a landlord? Here are concise answers to common investor queries.

What is a realistic monthly budget for a retired couple in Portugal in 2026?

A monthly budget between €1,500 and €2,500 (excluding rent) is a realistic target for a retired couple seeking a comfortable lifestyle. This covers everything from regular dining out and leisure activities to running a car. In a popular area like the Algarve, this budget supports a high quality of life. In smaller inland towns or on the Silver Coast, it stretches even further.

For an investor, this data points to a stable and financially secure tenant base. Retirees with reliable pensions can easily cover rent within this budget, signalling a low-risk, long-term tenancy and a predictable income stream.

How does the cost of living in Lisbon compare to other major European capitals?

Lisbon maintains a significant affordability advantage over most Western European capitals. As of 2026, consumer prices, including rent, are roughly 40% lower in Lisbon than in London. It is also around 20% more affordable than Berlin and offers substantial savings compared to hubs like Paris or Amsterdam.

This "capital city value" is a powerful magnet for a high-calibre tenant pool of international professionals and tech entrepreneurs, who are drawn by the opportunity to live in a vibrant European capital without the associated financial pressure.

For an investor, this imbalance is the core opportunity. It allows you to acquire an asset in a prime European capital with strong, consistent rental demand, but at a more accessible price point, catering directly to a high-earning tenant base.

Are utility costs significantly lower in Portugal than in the UK?

Yes, the difference is substantial and directly impacts tenant affordability. In Portugal, basic utility bills for a standard 85m² apartment (electricity, heating, water) typically average between €110 to €130 per month. This is significantly less than in the UK, where similar costs can easily exceed £200 (€235). A monthly saving of over €100 is a tangible boost to a tenant’s disposable income.

This provides two clear advantages for landlords. First, it makes your property fundamentally more attractive on the rental market. Second, if you offer a rental arrangement that includes utilities, the lower operational expense directly improves your net yield.

As an investor, does the low cost of living reduce my property management expenses?

Absolutely. The lower cost of living in Portugal directly translates into more affordable labour and professional services, which positively impacts your overheads as a landlord.

Key property management expenses are more affordable:

- Management Fees: The percentage charged by management firms is often competitive, and their underlying labour costs are lower.

- Maintenance and Repairs: Sourcing skilled tradespeople—plumbers, electricians, decorators—is generally less expensive than in countries like the UK, Germany, or the US.

- Cleaning and Upkeep: The cost of regular cleaning for common areas or preparing a property between tenancies is also more cost-effective.

These are not minor savings; they accumulate to provide a direct boost to your net rental income and enhance your overall return on investment.

At World Property Investor, we provide the data and analysis you need to make informed decisions in global real estate. Explore our full range of guides and market insights at https://www.worldpropertyinvestor.com.